Phase 2b Data Continues To Impress From HedgePath Pharma

TM editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

Interim Update Further Validates Why I'm Bullish On HPPI

In August 2016, I introduced investors to HedgePath Pharmaceuticals (HPPI) and the company's improved formulation of itraconazole for the treatment of Basal Cell Carcinoma Nevus Syndrome (BCCNS) / Gorlin Syndrome called SUBA-Cap. Investors can view that article >> HERE

HedgePath is currently conducting a Phase 2b trial with SUBA-Cap. Shares are up 134% since August 2016, driven in part by two positive interim results released over the past three months from the ongoing Phase 2b trial. The most recent update, which came this morning, demonstrates continued impressive results for SUBA-Cap. Below I provide a review of the positive Phase 2b data and compare it to Erivedge®, a leading product approved for metastatic and locally advanced basal cell carcinoma, but not for BCCNS, sold by Genentech/Roche.

A Little Background

HedgePath is currently enrolling patients in a Phase 2b open-label trial (NCT02354261) of SUBA-Itraconazole (SUBA-Cap) in subjects with basal cell carcinoma nevus syndrome (BCCNS). BCCNS is an autosomal dominant disorder characterized by the early appearance of basal cell carcinomas. Target enrollment for the Phase 2b trial is 40 patients with BCCNS. Entry criteria stipulate that each subject exhibit significant BCC target tumors at baseline consisting of a minimum of 10 surgically eligible lesions. Additionally, the subject must have a history of surgical removal of at least 10 BCC tumors. For each subject, 10 to 15 of the largest lesions are selected by the investigator at baseline to represent a valid sample of overall lesions (target tumors).The longest diameters of these target tumors are then added together to create a "target tumor burden” number.

HedgePath is collaborating with the BCCNS Life Support Network, a philanthropic organization dedicated to supporting the patients and families of patients with BCCNS / Gorlin Syndrome for this trial. The Phase 2b study is a single arm, multicenter, open-label study with a primary endpoint of the Response Rate of BCC target lesions. Enrollment began in September 2015. Interim results released on October 20, 2016, include an analysis of 18 subjects who have completed 16 or more weeks of SUBA-Cap dosing (oral 150 mg BID).

A previously completed Phase 2a clinical study with a generic formulation of itraconazole in patients with BCC is published in the Journal of Clinical Oncology (March 2014) (1), with data presented at AACR in April 2011. Eight subjects with multiple BCC tumors were treated with itraconazole. A total of 57 tumors were biopsied. Results show itraconazole reduced cell proliferation by 45% (P = 0.04), Hh pathway activity by 65% (P = 0.03), and reduced tumor area by 24% (95% CI, 18.2-30.0%). A waterfall plot published by Kim DJ, et al., can be found >> HERE.

Interim Phase 2b Data

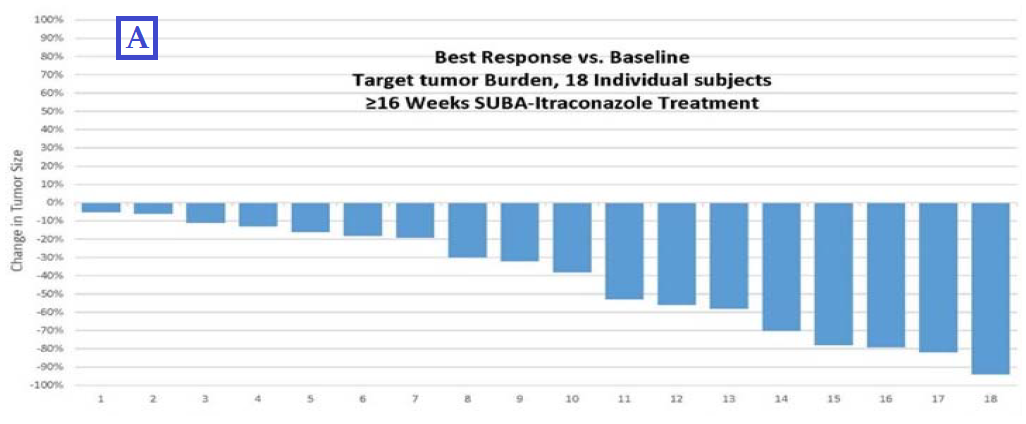

The interim data reported by HedgePath today was derived from results of the first 18 subjects who have completed at least 16 weeks of SUBA-Cap dosing. SUBA-Cap is a patented unique (non-substitutable) formulation of itraconazole which offers substantially improved bioavailability. Management conducted two separate interim analyses: (A) the change in target tumor burden for each subject (which is based on the change in the sum of the longest diameters of each subject’s target lesions) to measure the change in target tumor burden from baseline; and (B) the change in the longest diameter of all individual target lesions from baseline across all subjects in the study, which the company believes documents clinical impact.

On target tumor burden (A), among the 18 subjects who have dosed for ≥ 16 weeks, 100% of the patients had a target tumor burden reduction. Importantly, target tumor burden did not increase in any subject and was reduced by greater than 30% in 11 of the 18 subjects (61%) with an average reduction of 61%. This is important because the FDA guides that a tumor response rate, defined as a greater than 30% reduction in tumor burden, must occur 30% of subjects in order to be considered for approval. The results of the best response vs. baseline for each patient are graphed below:

(Click on image to enlarge)

An independent biostatistical analysis revealed the mean percent reduction in target tumor burden was 36% across all subjects when 7 subjects with stable disease and 11 subjects with partial response were included in the analysis (P-value <0.0001). HedgePath also analyzed the “best response” and “duration of response” (DoR) data for all 231 target lesions across the 18 subjects. The DoR was an encouraging 27.2 weeks for the significant number of tumors responding to SUBA-Cap treatment with 16 or more weeks of dosing.

On changes in the longest diameter of individual target lesions (B), the company conducted an interim analysis of 231 individual target lesions across all 18 subjects. All of these tumors were primary tumors, meaning none were metastatic lesions. The interim analyses showed that 31% of cancerous lesions have disappeared (complete response), an additional 30% have exhibited greater than a 30% reduction but less than 100% (partial response), and 38% have remained stable (< 20% increase and < 30% reduction).

- Response rate: CR (31%) + PR (30%) = 61% (141 of 231) (95% CI: 57.0-69.4%)

- Stable disease: 38% (88 of 231)

- Disease progression: 1% (2 of 231)

Presented below are the results of the 229 tumors that demonstrated stable disease, partial response and complete response:

(Click on image to enlarge)

The growth of a primary tumor increases the likelihood that an individual tumor will require surgical treatment. Although only 1% of target lesions (2 of 231) analyzed in the interim data have increased by more than 20% in longest diameter, one patient did require surgical intervention on one of these tumors. Management reported that SUBA-Cap continues to be well tolerated with Grade 1 or no toxicity reported in 89% of subjects assessed to date (16 of 18) in the trial. Two subjects had their dose of SUBA-Cap reduced due to elevated liver enzymes and one subject was forced to discontinue for peripheral edema.

Putting The Numbers In Perspective

Roche's Erivedge® (vismodegib) is an oral small molecule inhibitor of the Hedgehog pathway (Hh) signaling. Erivedge was approved in January 2012 for the treatment of adults with metastatic basal cell carcinoma (mBCC) or with locally advanced basal cell carcinoma (laBCC) that has recurred following surgery or who are not candidates for surgery or radiation. The U.S. FDA approval of Erivedge was based on results from a pivotal single-arm, multicenter, two-cohort, open-label, Phase 2 study that enrolled 104 patients with advanced BCC, including laBCC (n=71) and mBCC (n=33). Gorlin syndrome (BCCNS) was diagnosed in 22 of the 104 patients (21%).

Efficacy results published in the New England Journal of Medicine show an ORR of 30.3% for mBCC and 42.9% for laBCC (2). Complete response (CR) rates for mBCC and laBCC were 0% and 20.6%, respectively. Partial response (PR) rates were 30.3% and 22.2%, respectively. Median response duration was 7.6 months for both mBCC and laBCC. Only 7.7% (7/104) had disease progression.

Adverse events in the trial were significant and included muscle spasms (65%), alopecia (61%), dysgeusia (49%), weight loss (44%), fatigue (34%), nausea (28%), loss of appetite (22%), and diarrhea (21%). Several grade 3/4 events, including muscle spasms, weight loss, and fatigue were reported.

Novartis' Odomzo® (sonidegib) is an oral hedgehog pathway inhibitor indicated for the treatment of adult patients with locally advanced BCC that has recurred following surgery or radiation therapy, or those who are not candidates for surgery or radiation therapy. The U.S. FDA approved Odomzo in July 2015 based on a Phase 2, randomized, double-blind, multicenter clinical trial that enrolled 94 patients with locally advanced or metastatic BCC (3).

Efficacy results published in the Journal of the American Academy of Dermatology show an ORR of 57.6% for the 200 mg dose and 43.8% for the 800 mg dose in patients with locally advanced BCC. Patient with metastatic BCC has only a 7.7% and 17.4% ORR to the two doses, respectively. Among all patients, 19% progressed or died during the 12-month trial. Grade 3/4 adverse events and those leading to discontinuation were less frequent with sonidegib 200 versus 800 mg, but still were measured at 38.0% vs. 59.3% and 27.8% vs. 37.3%, for the locally advanced and metastatic patient populations, respectively (4).

The following table compares the Phase 2 data (full for BCC Erivedge and Odomzo vs. interim BCCNS for SUBA-Cap) based on ORR (CR + PR) and disease progression. Although more of an Apples-to-Oranges comparison, investors can see the ORR and rate of progression when comparing tumors treated with SUBA-Cap compares favorably with Erivedge and Odomzo.

(Click on image to enlarge)

Erivedge® Data In BCCNS

Roche conducted a separate Phase 2 with Erivedge (vismodegib) in patients with BCC Nevus Syndrome (also known as Gorlin Syndrome). The trial enrolled a total of 41 patients, 26 which received vismodegib and 15 on placebo. Data were published in the NEJM and although the reduction in the number of new tumor appearing in vismodegib treated subjects was impressive (primary endpoint of that study), the discontinuation rate in BCCNS patients was a staggering 54% due to adverse events (5). This contrasts starkly with the low toxicity profile observed thus far in subjects with BCCNS / Gorlin in the current Phase 2b SUBA-Cap trial. Recall, the discontinuation rate due to tolerability / side-effects in the ongoing Phase 2b trial is currently only 6% (1 of 18).

What's Next For HedgePath?

Data for SUBA-Cap demonstrate impressive interim Phase 2b results for HedgePath Pharma. Target enrollment is 40 patients and as per the company's press release, 18 have completed 16 or more weeks. The longest patients has been in the trial for 48 weeks. I do not know the current number of patients that have been enrolled, but I suspect that enrollment will complete before year end.

Per the protocol, 33 subjects must complete 16 weeks of active dosing, with 30% showing a response rate. This equates to only 11 patients. As noted above, management has already reported that 11 patients have responded with only 18 subjects completing 16 weeks. Obviously, the trial needs to continue, but I find it extremely encouraging that HedgePath has already achieved the target number of responders with less than half the patients completing the study.

Perhaps the most important takeaway from the interim Phase 2b results is that SUBA-Cap compares very favorably with Erivedge and Odomzo on efficacy and safety. These are two drugs that each cost over $10,000 per month. Roche posted global sales of Erivedge of CHF167 million ($162 million) in 2015, up 31% from 2014 levels. Approximately 70% of these sales were derived from the U.S. market. And importantly, approval of both Erivedge and Odomzo came after Phase 2b data in only around 100 patients.

HedgePath management intends to continue collecting data and will interact with the U.S. FDA regarding ongoing results demonstrating efficacy and tolerability for SUBA-Cap treatment for BCCNS. Erivedge and Odomzo are not approved for BCCNS, which presents HedgePath the opportunity to petition the FDA for approval if the final results of this 40-patient trial are as encouraging as the interim data above. As noted above, the company may have already achieved the primary endpoint with still half the patients left to fully treat for 16 weeks. Nevertheless, there can be no assurance that this trial will enable an NDA filing. As a reminder, in June 2016, the U.S. FDA granted HedgePath's SUBA-Cap Orphan Drug designation for the treatment of BCCNS.

A Look At Valuation

HedgePath currently trades with a market capitalization of $160 million. Shares trade on the OTC, but with the market value on the rise given the strong interim Phase 2b data, I see a logical path to a Nasdaq listing in the future. I believe if the final analyses from the Phase 2b study are positive, HedgePath will not remain valued at only $160 million for long. Therein lies the opportunity, today.

Recall, because SUBA-Itraconazole targets an orphan disease, management may be able to count the current Phase 2b study as the pivotal registration study. This would not be unprecedented, as both Roche and Novartis were able to gain approval for their respective skin cancer drugs, Erivedge (vismodegib) and Odomzo (sonidegib), respectively, based on only Phase 2 data. Both vismodegib and sonidegib target the hedgehog pathway, similar to itraconazole.

However, if we assume that HedgePath's current trial is a registration-quality study, then positive data would likely send the shares above the Feuerstein-Ratain "Mendoza" line of $300 million. I believe the shares are below $300 million today because investors view the Phase 2b study as "Phase 2" instead of potentially pivotal. Again, there is clear risk that the final results will not match up with the impressive interim data, but using the Feuerstein-Ratain rule as a way to project valuation upon success provides a good starting point to talk about what HedgePath is worth if the NDA goes under review.

I have developed a detailed financial model to value HedgePath Pharma. Investors can view that model >> HERE. I peg the fair value of the stock today at $0.80 per share, with obvious upside over $1.00 based on filing the application during the first half of 2017. Approval of SUBA-Cap puts the stock fairly valued at roughly $2.00 per share.

Conclusion

HedgePath remains an interesting story for small-cap biotech investors. The company is likely to report full enrollment over the next few months, with top-line Phase 2b results expected during the first half of 2017. If the full data look as strong as the interim data presented today, I expect the company to seek approval for SUBA-Cap via the 505(b)(2) pathway before the end of 2017. I see the peak opportunity for SUBA-Cap at $750 million, which includes the upside from use in metastatic or locally advanced BCC, or other solid tumors where itraconazole has demonstrated utility such as lung cancer or prostate cancer.

BioNap Consulting provides both sponsored and independent equity research, due diligence, valuation analysis, market research, strategic advice on M&A or product in/out-licensing opportunities, ...

more

{kind=link}

{kind=link}