You already know about my concerns around higher-yielding stocks. When a company offers a yield of over 5-6% (especially in today’s market with low-interest rates), you must take a minute to understand why. There is no free lunch in finance. Should you aim at higher yield? Yes, but not to a point where you increase the risk to your portfolio. We have designed the DSR dividend safety score to help prevent most dividend cuts in your portfolio. Many companies rated “2” cut their dividend in the past 2 years. One sector including many of them are Energy MLP’s. I know they are praised by income-seeking investors and this is why I want to highlight this industry. First, let’s do a recap of what they are.

What are MLP’s?

MLPs were formed in the U.S. in the early 1980’s. They are publicly traded partnerships. Back then, there were much higher top marginal tax rates than there are currently so investors were particularly interested in tax-advantaged businesses. The MLP structure allowed businesses to spin off portions of their assets in a very tax-advantaged situation and allowed individual investors to benefit as well. But the structure was so attractive in terms of taxation, that practically every business would want to be an MLP, and so in 1987, the government restricted which kinds of businesses can exist as MLPs.

The structure of MLPs can vary to some extent, but the basic structure is this: There exists a General Partner (GP), that consists of the management team, and Limited Partners (LPs), that contribute capital. Often the entity that holds the GP also holds some LP units.

Limited Partners contribute capital by buying units of the MLP. (They are called units rather than shares). These LP units can then be traded on a stock exchange. In return, the LPs receive distributions from the operations, which are similar to dividends.

The GP often has Incentive Distribution Rights (IDRs) that are set forth in the founding of the partnership. The IDRs give the GP a ton of incentive to raise the distribution overtime for the units that the LPs hold. These partnerships, therefore, are specifically designed for distribution growth.

This is what we have seen on the market in the past few years: a bunch of MLPs raising their distribution month after month while seeing their stock value disappearing faster than Nutella in a house filled with teenagers. All those MLPs offer incredible yields (many of them over 10%). Income seeking investors went after them thinking they found their golden egg hen. Unfortunately, the hen is about to kill itself leaving you with no more shiny eggs.

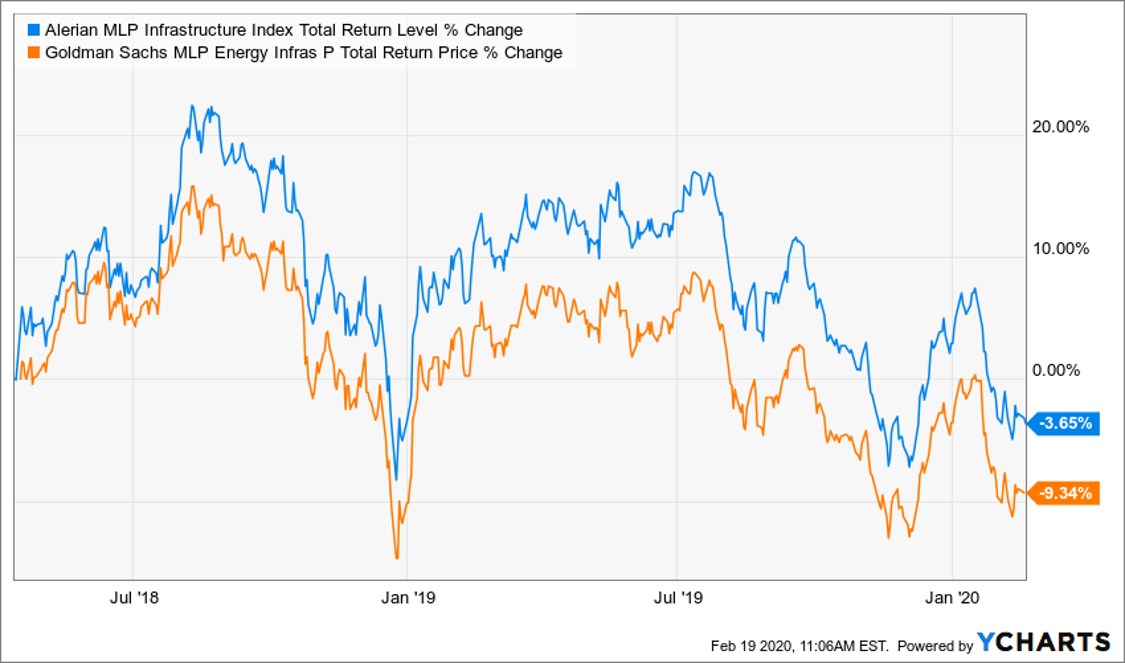

MLPs are Currently Burning Your Cash

If you have built an MLP portfolio in the past 5 years, chances are you feel like you are using dollar bills to fuel your furnace. If you look at the Goldman Sachs MLP Energy Infrastructure fund (GMNPX) and the Alerian MLP Infrastructure Index Total Return (ALMLPITR) you will see how you never made a single penny after 5 years, no matter how big your distributions were.

Source: Ycharts

Considering the past 5 years have been incredible on the stock market, investing in MLP’s for the sake of their high yield seems like a monumental error. However, this doesn’t mean there are no good MLP’s out there. Funny enough, many companies in this industry reported great financial results over the past 2 years.

One thing you must follow when you look at MLP’s is their distributable cash flow (DCF) and DCF per unit. Since the single purpose of this business model is to raise their distributions, you want to make sure the dividend is covered. The “coverage ratio” will be discussed in each quarterly earnings report. A coverage ratio of 1.0x means that a company generated exactly enough cash in the period to cover its distribution. In an ideal world, you would like to see a coverage ratio over 1.0x all the time.

Why Such Sell-off?

If an MLP is reporting good earnings and a solid coverage ratio, why in the world would its unit price keep going down? There are several reasons explaining the bear among all the bulls. Some of them are justified, some others not too much.

#1 MLPs are complicated. Due to their unique structure, many investors don’t quite understand how they work. A good example of that is when the Federal Energy Regulatory Commission (FERC) modified tax rules for MLPs back in March 2018. On Bloomberg, you could read the following headline:

Pipeline Stocks Plunge After FERC Kills Key Income-Tax Allowance

This was more than enough to kill about 10% of the market value for any MLPs. Interesting enough, the new ruling only applied to MLPs using the specific “cost of service” rate-setting method. Most of them don’t use that method and yet, investors didn’t listen. They probably fear the FERC will eventually come with more new rulings.

#2 The oil & gas business isn’t exactly booming right now. Considering the major trend in finding cleaner energy sources, the oil & gas industry is facing many headwinds. We can see money (including institutional investors’) moving away from this industry and going after the renewable energy sector. If you look at companies like Brookfield Renewable Partners LP (BEP, BEP.UN.TO) over the past 3 years, you’ll know what I’m talking about. The good old “offer vs demand” rule applies, and shares/units prices go down as nobody wants to buy them anymore.

#3 Incentive Distribution Rights (IDRs) are weighing on future projects. With such high yields, MLPs are limited in the number of new units they can issue as their distribution rates are killing their cash flow. It used to be easy to issue new units or secure more debt to finance large projects and increase their distribution. The “party” seems to have come to an end and many investors don’t believe MLPs will be able to grow at the same pace anymore.

#4 This all leads to one thing: the fear of distribution cuts. It already started to happen in the industry as previously mentioned. Some MLPs just can’t keep up with their current structure and must slash their distribution. In such event, you lose both your income source and a part of your capital.

Oh, and don’t forget about the fun you’ll have to complete your taxes. MLP distributions come with a K-1 for each MLP you own. The Schedule K-1 is a laborious, complex form. You might not want to attend to this “paperwork party” each year at tax time.

One MLP I like

Magellan Midstream Partners LP (MMP) is probably one of the safest MLP at the moment. The company offers a decent yield (6.50% to 7%) without destroying completely your capital (-4.55% total return over the past 5 years).

MMP provides network access to nearly half of the U.S. refining capacity. The company is well-positioned to enjoy Permian basin cost advantage. It also owns the longest refined petroleum products pipeline system. Management has proven to make great capital allocation decisions so far. Unfortunately, we are a little concerned their golden years are behind them. The rise of many competitors and the fear of a potential economic slowdown reduce MMP’s growth perspectives. At least, its juicy dividend yield is combined with an excellent history of distribution growth. Along with some core dividend picks, MMP could not only boost your portfolio’s yield but also provide healthy growth.

Since the whole purpose of an MLP is to provide income, you can use the dividend discount model to calculate Magellan Midstream Partners' intrinsic value. Using the Dividend Discount Model with a dividend growth rate of 5% for the first 10 years and a terminal growth rate of 4% (you can use the Dividend Discount Model spreadsheet here), we can see that MMP trades under its fair value right now.

| Input Descriptions for 15-Cell Matrix | INPUTS | ||

| Enter Recent Annual Dividend Payment: | $4.11 | ||

| Enter Expected Dividend Growth Rate Years 1-10: | 5.00% | ||

| Enter Expected Terminal Dividend Growth Rate: | 4.00% | ||

| Enter Discount Rate: | 10.00% | ||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $110.97 | $92.22 | $78.83 |

| 10% Premium | $101.72 | $84.53 | $72.26 |

| Intrinsic Value | $92.48 | $76.85 | $65.69 |

| 10% Discount | $83.23 | $69.16 | $59.12 |

| 20% Discount | $73.98 | $61.48 | $52.55 |

Please read about the dividend discount model limitations before drawing any conclusions.

As you can see, there is a possible ~20% discount on the current stock price. You can then enjoy a steady income stream and hope for some capital appreciation along the way.

Comments

Log in or sign up to join the conversation.