Image Source: Pixabay

Earnings season is nearing its end, with the vast majority of S&P 500 members already delivering quarterly results. The Q2 cycle has overall been resilient, underpinned by a strong showing from Tech, with the same expected for the current period (Q3).

Still, we’ve got the most important release of the Q2 cycle on deck for next week, which is coming from none other than AI favorite Nvidia (NVDA - Free Report) .

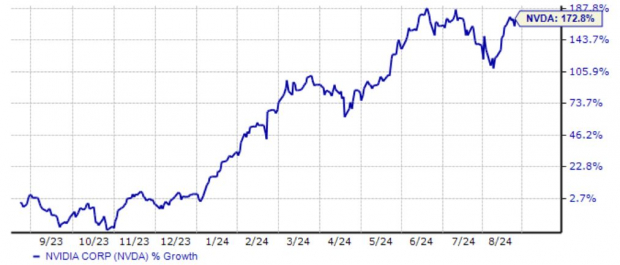

We’ve all become accustomed to the company’s remarkable story, with shares gaining an incredible +170% over the last year on the back of record-setting Data Center results.

Image Source: Zacks Investment Research

Let’s take a deeper dive into the most highly-awaited release of the Q2 cycle and see if the stock is still worth a buy.

EPS & Sales Expectations Stay Muted

Headline expectations for Nvidia haven’t seen much action over recent months, with analysts keeping their estimates stable. This is a different development relative to other recent periods, as the stock previously enjoyed positive revisions leading up to other recent releases.

Still, another period of robust growth is expected, with consensus expectations alluding to a 130% pop in earnings on 110% higher sales.

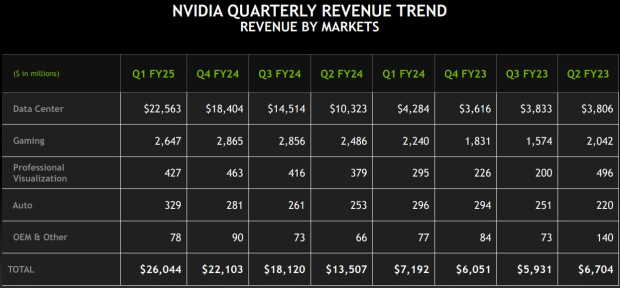

The $28.2 billion expected would pencil in the fifth consecutive period of triple-digit percentage Y/Y sales growth rates. Below is a visual breakdown of the company’s sales, showing that the data center has quickly become its most lucrative segment.

Image Source: NVIDIA

Data Center Expectations Remain High

The company’s breakneck sales growth has been led by unbelievable Data Center results, which have consistently shattered records for the company in recent releases. For a quick refresher, the company’s Data Center results include the sales of its AI chips.

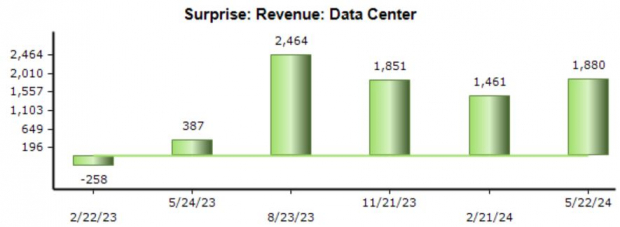

Below is a visual illustrating the company’s Data Center results relative to our consensus expectations in recent periods. As you can see, the beats have been overwhelmingly strong over recent periods, with the most recent beat totaling a sizable $1.9 billion.

Image Source: Zacks Investment Research

For the quarter to be released, the Zacks Consensus Estimate for Data Center results stands at $24.6 billion, 140% higher than the year-ago mark of $10.3 billion. Still, it’s critical to note that there have been reports of delays for its chips based on Blackwell architecture, which could negatively affect coming periods if the delays remain longer than expected.

The Blackwell architecture reflects a serious upgrade, delivering up to 4X faster training and 30X faster inference than the H100. Amazon, Google, Meta, Microsoft, OpenAI, Oracle, Tesla and xAI are among the many organizations expected to adopt Blackwell.

Demand for Hopper and Blackwell GPUs remains rock-solid and well ahead of supply, with the supply/demand mismatch trend expected to continue well into 2025. We’ll likely hear further color concerning the supply constraints in the release, particularly concerning reported delays for Blackwell.

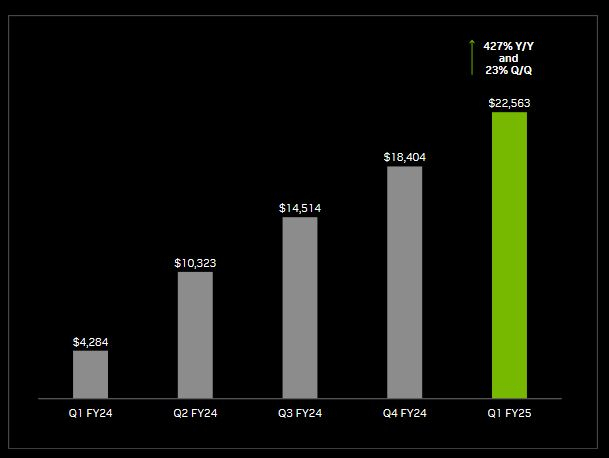

Below is a chart illustrating the company's Data Center results on a quarterly basis.

Image Source: NVIDIA

Are Shares Expensive?

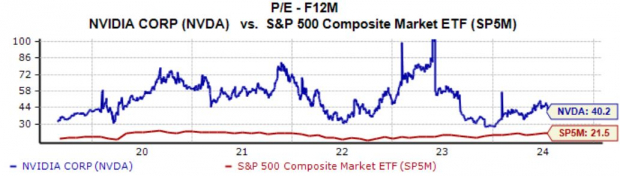

Given the stock’s massive run, many have become wary of the valuation picture. Shares presently trade at a 40.2X forward 12-month earnings multiple compared to a five-year high of 106.3X and a five-year median of 50.7X.

Relative to the general market, current valuation levels reflect a considerable premium, with the S&P 500 currently trading at a 21.5X forward 12-month earnings multiple.

Image Source: Zacks Investment Research

Further, the current PEG ratio works out to 1.1X, reflecting a bargain relative to a 2.6X five-year median and five-year highs of 5.5X. So, while the stock isn’t cheap when compared to the general market, it’s currently trading at a discount relative to its historical levels.

Image Source: Zacks Investment Research

5 Key Points

Investor and AI-favorite Nvidia undoubtedly reflects the most highly-awaited release of the Q2 cycle, with the company’s growth story expected to continue in a big way. Here are five key points to keep in mind -

- Estimates have largely remained stable for the release, the opposite of what the stock has experienced in prior periods.

- Data Center expectations remain strong, with the company again expected to deliver triple-digit percentage year-over-year sales growth.

- We’ll likely hear further color concerning Blackwell delays and demand, though the company has already previously recognized a supply/demand mismatch (for both Hopper and Blackwell GPUs) that’s expected to continue well into 2025.

- Shares aren’t expensive relative to historical levels but do reflect a big premium when compared to the S&P 500. Remarkable growth has helped keep valuation multiples down, with the current PEG ratio also reflective of a fair price for the forecasted growth.

- Shares are up 175% over the last year, with the stock moving into a Zacks Rank #3 (Hold) in late July. A beat-and-raise quarter would usher in positive revisions, likely helping it find its way back into a favorable Zacks Rank.

More By This Author:

3 Artificial Intelligence Stocks To Buy For Dividends: Taiwan Semiconductor, Micron, BroadcomInsider Trading: 3 Stocks CEOs Are Buying

3 Companies Unlocking Higher Profits: KMB, DECK, WMT

Comments

Log in or sign up to join the conversation.