Netflix (NFLX) has officially clinched the blockbuster bidding war for Warner Bros Discovery’s (WBD) premium assets – the Warner Bros. film and TV studios and HBO Max streaming service – in an $82.7 billion cash-and-stock megadeal announced this morning, valued at $27.75 per share.

This caps weeks of intense rivalry with Paramount Skydance (PSKY) and Comcast (CMCSA), where PSKY chased the full company including the cable assets, and Comcast zeroed in on studios to dodge antitrust pitfalls. Netflix's winning bid – blending $23.25 cash and $4.50 in NFLX stock per share – seals the fate for a debt-burdened WBD, paving the way for its planned cable spinoff into Discovery Global.

For NFLX investors facing this seismic shift, the burning question is, does victory mean it's time to sell?

A Strategic Fit

Netflix has been clear that it wanted no part of WBD's cable TV channels like CNN or TNT, focusing solely on the studio and streaming crown jewels. This aligns with Netflix's streaming-first focus, avoiding the declining linear TV business that's plagued traditional media giants.

What may have pushed NFLX bid to the top was The $82.7 billion price tag (roughly $31 per share for the acquired assets) lets WBD wipe out most of its $40 billion debt mountain and hand shareholders a clean, focused linear-TV company.

For Netflix, the prize is enormous: instant ownership of some of the world’s most bankable IP, plus HBO Max’s 100 million subscribers (many of whom overlap, but many more who don’t). Combined with Netflix’s 300+ million global accounts, the merger creates an unassailable content moat just as ad-tier and password-sharing crackdowns are supercharging monetization.

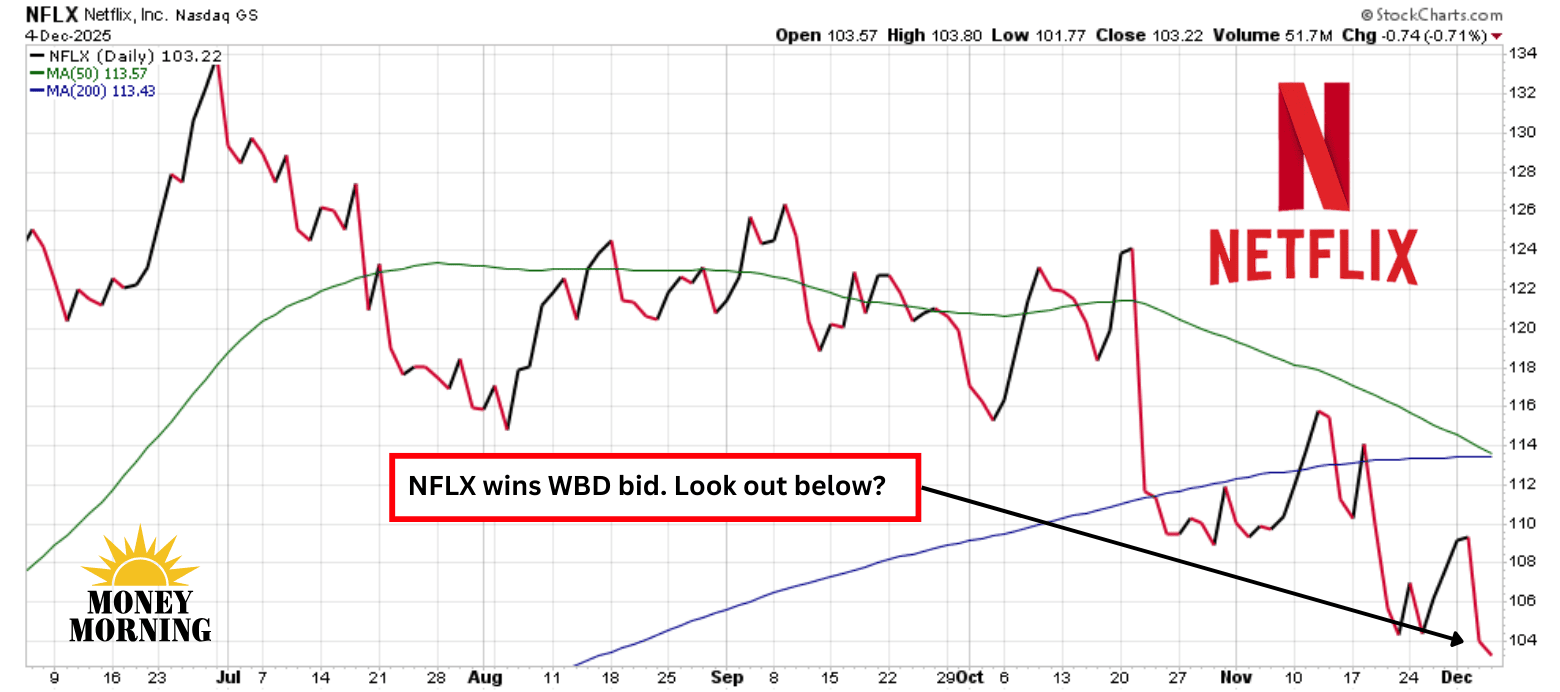

(Click on image to enlarge)

The Massive Risks Investors Can’t Ignore

The upside is dazzling, but the price is brutal. $82.7 billion in cash and stock will blow through Netflix’s $17 billion cash hoard and force the company to raise tens of billions in new debt or equity at a time when interest rates remain elevated. Leverage that was once negligible will suddenly be substantial.

Of equal concern is the integration minefield. There are bound to be culture clashes merging Netflix's Silicon Valley agility with WBD's Hollywood bureaucracy. History paints a grim picture: Successful M&A hovers at just 10% to 50%, with 70% to 90% failing to deliver promised synergies due to integration woes, overpayment, and clashing cultures.

Bain & Company notes substantial value destruction in mega-deals. Where smaller bolt-on acquisitions shine, transformative ones falter. For NFLX, the lure of Harry Potter and GoT may not be enough to surmount the debt drag and merger indigestion that follows.

Bottom Line

The market doesn't like it. NFLX stock tumbled 5% on Wednesday, closed slightly lower yesterday, and is dropping 4% in premarket trading today after the news broke. Investors fret over dilution, regulatory hurdles, and Paramount's claims of a "tainted" process. Netflix faces large execution risks on a stock already trading at 43x earnings.

Should NFLX investors sell? I wouldn't make a knee-jerk decision, because Netflix may be able to pull it off, but more conservative investors may want to move to the sidelines as mega-mergers typically don't turn out well. A successful deal could redefine streaming – but there's high likelihood Netflix instead turns into another AOL-Time Warner sequel.

More By This Author:

From "Uptober" Hype To Winter Woes: Can Bitcoin End 2025 On A High Note?Is Copper The New Gold? Here’s Why Freeport-McMoRan Is The Best Stock To Buy

Why Hedge Fund Bets Make UNH Healthcare's Hottest Turnaround Play

Comments

Log in or sign up to join the conversation.