Netflix Stock Forecast: Will Netflix Survive The Streaming War?

Highlights

- People are leaving bundle TV and going to streaming because it offers a much better service at a lower price. Netflix's biggest competitor is the bundle tv, and other streaming platforms seem to be complementary.

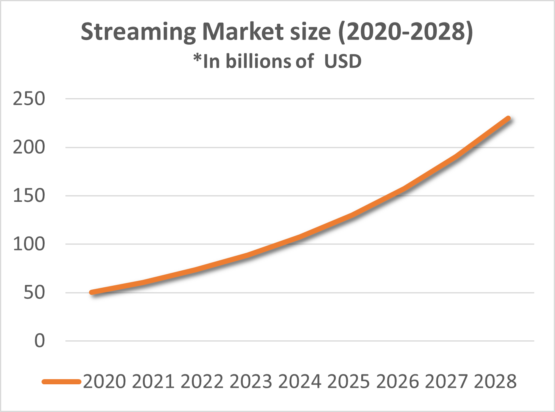

- The streaming market is expected to expand at a CAGR of 21% from 2021 to 2028.

- Netflix is losing market share to its competitors as the streaming war escalates.

- Forecasts for Netflix remain positive on revenue and subscribers.

- NFLX stock is already considered overvalued, even though few analysts remain bullish.

Transition bundle TV – to streaming TV

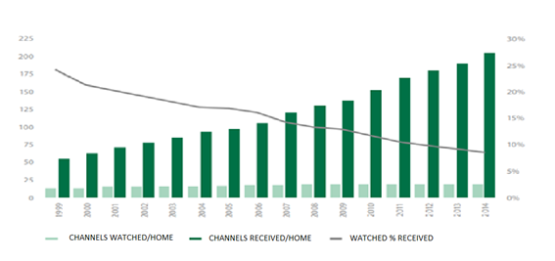

Bundle TV, every year is losing more and more market share for streaming platforms for many reasons. One of the most important reasons is that is way cheaper, and you can watch what you want, whenever you want without sponsors. American citizens, pay 70% less on Netflix per watched hour and offers for most people a better service. An average user of Netflix fails to watch 200 hours of advertising a year, almost 8 full days. For this reason, people are leaving bundle TV, and most of them are young people. Due to this fact, Netflix’s forecasts towards new subscribers are good for a long time.

Another reason that shows how Netflix’s business model is better than the classic bundle TV, is that in the normal bundle, an average user pays for more than 200 channels, and only watches 18. With the internet, every entry barrier became easier to break and compete with, so Netflix with the internet disrupted the bundle TV market that was a well-consolidated market.

Overview of the streaming market

Besides the bundled TV, which has more than 800 million subscribers all around the world, Netflix has some big competitors that are also growing at high rates, such as Amazon (amazon prime), Disney (Disney +). The streaming market was growing at huge rates, and during the pandemic grew even more. Some studies are forecasting a future CAGR for the streaming market of more than 21% YoY from 2021 until 2028 reaching close to 230 billion USD.

Contrary to what many people think, we will have complimentary streaming platforms and not a winner takes all. This is because, when they leave the current TV packages, there will be a budget left over to have more than one streaming, since the bundled TV is much more expensive. Also, Disney+ should have a larger membership of children, and streaming is just one part of a larger ecosystem. Amazon prime is used to attract and retain customers for e-commerce, and each of them has different shows that attract different types of clients.

Netflix business model

Netflix’s only focus is streaming video, and for this reason, they are ahead in many aspects, such as technology. With the Netflix technology, users can receive content that is personalized due to the machine learning process. Moreover, the focus on only one main business can provide Netflix more flexibility towards its decisions compared to the biggest streaming competitors. Amazon and Disney are the biggest competitors in the streaming market, and they need to decide the future of their streaming together with their main business (e-commerce/ parks). However, these two big companies have much more money to invest in the streaming market than Netflix, since Amazon is one of the biggest companies in the world and Disney is already a huge producer, with brands known all over the world.

Netflix has almost a decade of leadership, and this provides lots of benefits for the company and for staying ahead of the competition. One consequence is that customers who have been using a service for a long time tend not to leave the company as easily as a new customer. With this, Netflix manages to have a much lower churn rate than its competitors and a much higher LTV, and by that invest more money in looking for new clients and less for trying to “prove to the client” that is worth staying subscribed, and for this reason, Netflix always had good stock forecast about the future.

Netflix has a decade more of data, and this way can make better recommendations for the clients, which makes the client experience way better and this also helps to reduce the churn rate. Lastly, the advantage of being alone in this market for so long ensured that Netflix became a global producer, and by that, people all around the world have content about their country. This global producer feature makes the streaming entry barrier a little stronger, but not enough to keep other players out of the market.

The streaming market becoming more competitive

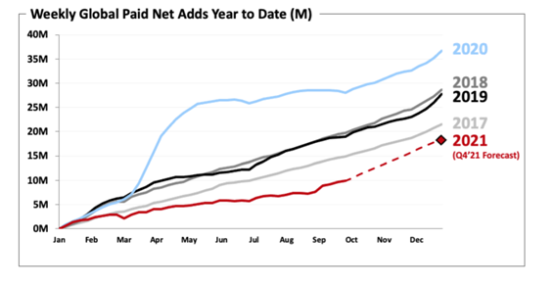

Although Netflix has all this advantage over the competition, last year it didn’t show us this scenario. Netflix’s market share dropped 31% from 2019 to 2020, thus going from 29% market share in 2019 to 20% market share in 2020. Amazon’s prime market share is really close to Netflix, and by that, the advantage that Netflix had of scale is turning almost equal to Amazon, showing us that the streaming war is not going to be easy for either side and causing the worst forecast towards Netflix stock.

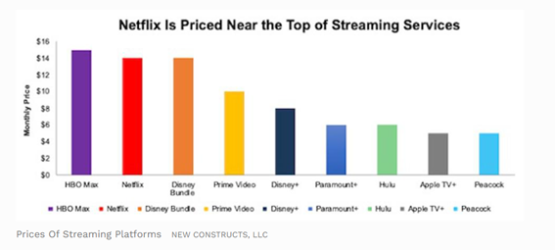

The market trend is for Netflix to lose even more share, once there are many competitors entering the market as the barrier to entry is low and there are other competitors getting stronger and ready for “war”. Disney offers a bundle at the same price as Netflix but offers Disney+, Hulu, and Espn+. Amazon prime offers a cheaper plan and includes the Amazon Prime shipping service. Netflix is cheap when compared to the bundled TV, but when compared with other streaming platforms is expensive.

The rising of new competitors creates another problem, which is the increasing cost of its streaming. The cost of production is increasing due to the additional licensing for third-party content in addition to the marketing for this content. This happens because of the simple economic rule of supply and demand, once there are more competitors wanting to license the same shows and have the same actors, for example. When Netflix was alone in this market, they had low costs of licensing most of the shows. Nowadays, great actors have numerous options of choosing which producer they want to participate in a movie, so the cost of Netflix hiring actors like Chris Hemsworth or Dwayne Johnson significantly increased.

What Are Netflix’s results and the forecast for next quarter?

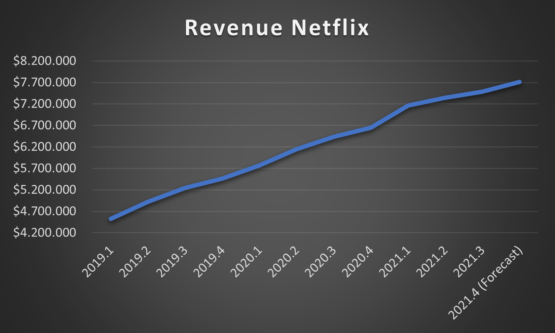

In recent quarters the company has always managed to exceed the expectations of analysts and the projections shown in the shareholder letter. In the last quarter, (third quarter of 2021) Netflix released a balance slightly higher than expected by the market, and for this reason, the stock has already gained 7% since the release on October 19th. The revenue grew almost 2% in the third quarter and is expected to grow 3.05% in the next 3 months based on the forecast shown in the Q3 2021 Shareholder letter.

The ROE of the last 12 months is 11.82%. Since the forecast of net income from the financial statements for the next quarter (4th quarter) is expected to decrease significantly, the last quarter ROE will probably also decrease. The ROE for 2021, considering the Netflix projections, is expected to be 11.40%.

In terms of customers, Netflix continues with growth projections of more than 8 million new subscribers for the next quarter and reaching 222 million subscribers worldwide. In the last 4 quarters, Netflix subscribers grew at a compound growth of 2.28% per quarter. For the next quarter, the forecast is that Netflix will grow 4% in the number of subscribers.

Netflix Valuation

Regarding Netflix’s valuation, the stock price is reflecting a very promising future, although many think that Netflix will not meet this expectation. There are few analysts that can see space for the stock continue to rise. Douglas Mitchelson at Credit Suisse boosted his price target from $643 to $740, a move that suggests a 17% of upside from the current level. Hamilton Faber at Atlantic Equities increases his price target on the stock from $690 to $780. Those analysts that still think that Netflix could still rise, see around 20% gain.

Other than that, when you look at which investment funds invest in Netflix, there are 5 big investors who have a significant position. All these investment funds have unattractive ratings. This is very asymmetric, once if everything goes really great Netflix could rise as high as 20%, but if not, Netflix could stay trading in this price range for a long time or even reduce the stock price.

Netflix is being traded in a P/E close to 60x. Even though Netflix P/E is lower than the last few years, it doesn’t prove that now is a great opportunity for investment, since the conditions changed a lot in the last years, when before Netflix was the only one in the streaming market and growing in high rates.

Since streaming is not the main business of Netflix competitors, is it not recommended to look only for the P/E. Amazon Apple Disney and AT&T shares are traded based on the company’s main business and with that, if we analyze only the P/E of the companies, we will reach conclusions that Netflix is expensive, as the other businesses are traded at multiples smaller than video streaming.

Conclusion

Netflix is a great company, is going to grow a lot in the next years, and has a CEO that has proven that he is capable of maximizing long-term shareholder value. Yet, Netflix stock already is reflecting all this growth that is expected and maybe more than it can grow in the streaming market. Netflix is entering the video games market, and maybe with this new business segment Netflix stock can possibly grow more than 20%. For this reason, I am neutral towards Netflix because I don’t see much space to grow, and I don’t think it’s worth the risk of short-selling the stock, given the conditions and the impressive ability of CEO Reed Hastings to reinvent and adapt the company’s business model.

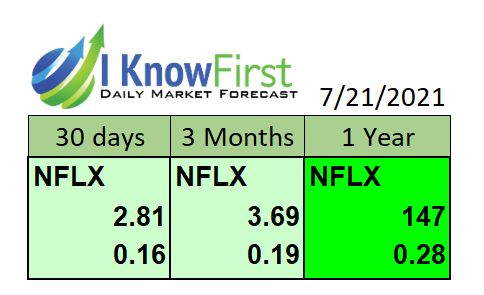

My conclusion is in line with the I Know First’s predictive algorithm forecast. The bullish one-year stock forecast for Netflix provides a very strong signal at almost 200, however, the predictability of the asset is not so favorable. Therefore, NFLX stock is currently a risky choice for your portfolio for the next year, even though for a diversified portfolio, it could be an attractive option.

Past Success With Netflix Stock Forecast

I Know First has been bullish on the Netflix stock price in the past. The I Know First algorithm issued a Netflix stock forecast on July 22th, 2021, recommending NFLX’s stock for the coming year. Despite that the prediction for the one-year horizon is not over yet, the algorithm successfully forecasted the movement of Netflix’s shares on the 3 months time horizon. NFLX’s shares rose by 22.99% in line with the I Know First algorithm’s forecast.

Please note-for trading decisions use the most recent forecast.

Here at I Know First, our AI-based stock forecast algorithm has modeled and predicted assets price movement worldwide for ...

more

Thnks for an educational, interesting, and useful article!

Of course, Netflix would not exist as we know it without the streaming technology, and so while it was first, it was more a pioneer of the streaming era. Prior to that the closest was "Pay-per-view", whatever technology that used.