The commitment of central banks around the world to battle inflation and the associated increases in interest rates to achieve this goal are instigating global growth concerns. In this environment, safe-haven assets tend to perform better than riskier equity investments. Today, markets consolidated in anticipation of tomorrow's US CPI, which might have a significant impact on future monetary policy decisions and assets’ trajectory.

Earlier in the week, the IMF and World Bank downgraded their economic forecasts for 2022 and 2023, underscoring that much of the global economy is headed for recession next year. Today, OPEC followed suit and revised down its oil demand forecasts citing high inflation levels, continued China COVID-related shutdowns, and slowing economies. This announcement marked the fourth cut in demand forecasts since April.

In such an uncertain and dismal environment, the demand for safe-haven assets tends to increase, while the performance of equity investments tends to deteriorate. Today, stocks closed in negative territory as investors awaited the publication of tomorrow's CPI data while digesting a slightly higher-than-anticipated September PPI reading.

At the close, the Dow, the S&P 500, and Nasdaq 100 all posted losses of 0.10%, 0.33%, and 0.53% respectively. Only three of the eleven S&P sectors advanced with Consumer Staples among the leaders. PepsiCo reported strong quarterly results and raised its 2022 sales and earnings guidance.

On another front, Fed officials have maintained a hawkish stance. Minneapolis Fed President Kashkari reaffirmed the FOMC's commitment to fighting inflation while stressing that the bar for monetary policy turning is set very high. In addition, the FOMC Minutes from the September meeting also suggested that interest rate hikes will continue until a sufficiently restrictive level is reached to then sustain them and assess the impact on the economy and the financial system.

TECHNICAL OUTLOOK

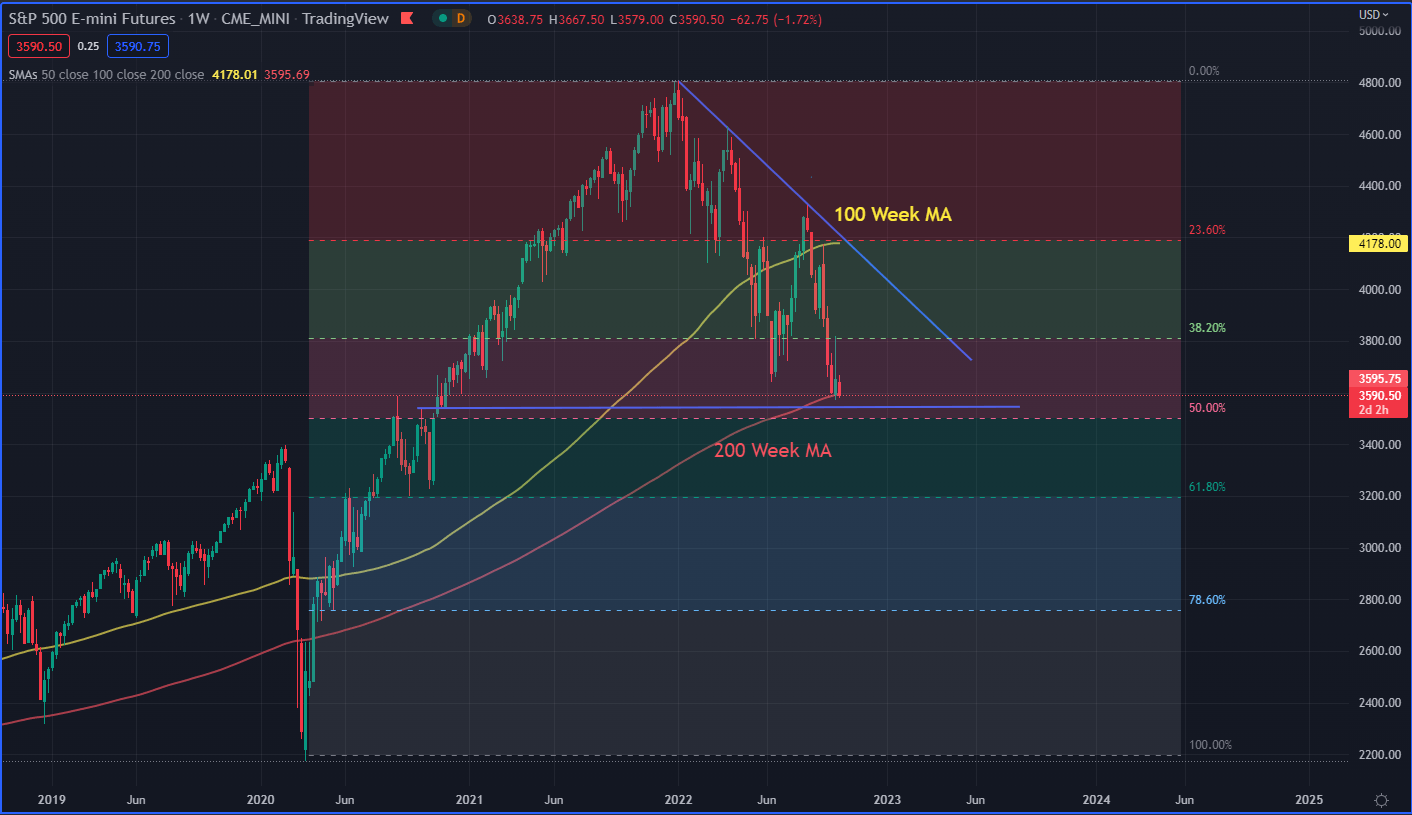

From a technical standpoint, the S&P 500 wavered between gains and losses during today’s session before snapping finishing in negative territory for the sixth consecutive day. Uncertainty and indecision ahead of the CPI is visible. The figure could be crucial for next monetary policy decision but also for the trajectory of equities. We continue to monitor the key support level of 3600, which is near the 50% Fibonacci retracement level and also converges with the 200-week moving average. If we see a weekly close below 3600, the next floor is seen around 3540-3500

S&P 500 (ES1) Mini Futures Weekly Chart

(Click on image to enlarge)

S&P 500 Mini Futures Chart. Prepared UsingTradingView

Looking ahead, the September CPI number is expected tomorrow at 8:30 EDT. Markets are expecting an increase of 8.1% y/y, down from 8.3% in August.

More By This Author:

S&P 500 Seesaws After Hawkish Fed Minutes, Stock Market Fate Tied To Inflation Data

EUR/USD Struggles As Markets Look To EU Energy Meet

New Zealand Dollar Bucks USD Strength but APAC Sentiment Fragile on China Lockdowns

Comments

Log in or sign up to join the conversation.