TM Editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

Image Source: Unsplash

MAIA Biotechnology (MAIA), a biotechnology company developing innovative cancer treatments, has seen its stock drift downwards for the past months as it has fallen victim to the worst biotech bear market ever. Despite releasing blowout data for their lead oncology treatment asset, the stock has sold off. This presents investors with the opportunity to invest in a stand-out, groundbreaking cancer treatment entering the mid-stages of development (phase 2 clinical trials) at venture valuations. If MAIA can continue to show their cancer treatment has eye-popping efficacy as well as a good safety profile, the potential upside is enormous for investors buying at these levels.

MAIA’s Audacious Goals in Cancer Therapy

MAIA is going after large targets in the oncology space, starting with NSCLC (non-small cell lung cancer). Now, going after this indication is an audacious goal as this requires proving superiority over current standard of care treatments, which include therapies with immune checkpoint inhibitors (ICI) alone and in combination with chemo, depending on how advanced the disease is. Overall, the current market leading immune checkpoint inhibitor (ICI) for treating NSCLC is Merck’s (NYSE: MRK) Keytruda, which is used standalone and also with chemo for a variety of NSCLC applications or stages (i.e. perioperative, early, late stage). The way MAIA intends to succeed in becoming standard of care over current market leaders in first and second line NSCLC (Merck’s Keytruda and Eli Lilly’s (NYSE: LLY) Cyramza + chemo, respectively) is by teaming up in combination with Regeneron’s (REGN) Libtayo (aka cemiplimab-rwlc). The oncology playing field is crowded and it's difficult to compete with big pharma and their development resources as well as their well-oiled commercial sales and distribution machines. If a small company like MAIA wants to succeed in immunotherapies for cancer, its best bet is to work with big pharma, not against them.

Merck’s Keytruda, which is the current market-leading immune checkpoint inhibitor (ICI) for treating NSCLC, and Libtayo has the same mechanism of action as Keytruda. These drugs, called PD-1 inhibitors, are also considered the backbone of ICI combination therapies. They work by blocking the PD-1 receptors from receiving signals. Immune cells such as T cells express PD-1 proteins on the cell surface which signals to the T cells to basically turn off: “Engagement of PD-1 by its ligands PD-L1 or PD-L2 transduces a signal that inhibits T-cell proliferation, cytokine production, and cytolytic function.” Cancers often learn to produce PD-1 ligands (keys) as a defense mechanism in response to the immune system attack. So these drugs allow the T cells, potent cancer killers, to keep on killing without being turned off. By combining PD-1 inhibitors with other therapies like chemo or other immune system-augmenting or direct cancer-killing drugs, overall therapy efficacy can be improved further. And if MAIA knocks it out of the park in NSCLC with Regeneron’s Libtayo, the chances are high that Regeneron will in-license MAIA’s cancer drug, THIO-101, and use it along with Libtayo to steal the NSCLC crown from Keytruda and subsequently make billions. ICI therapies dominate the market in NSCLC, and Keytruda is heading the pack.

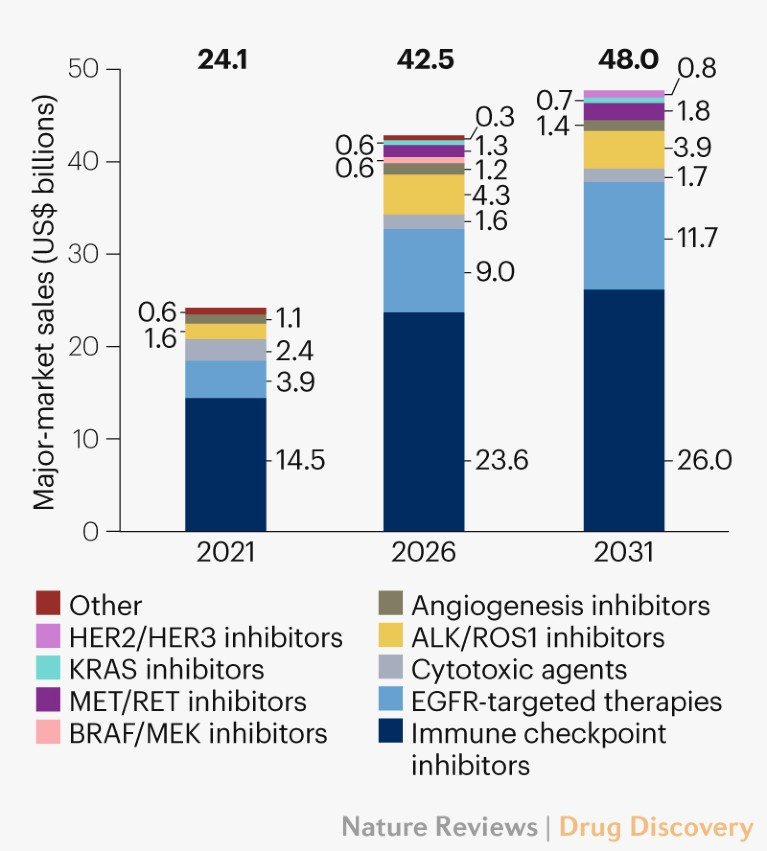

The non-small-cell lung cancer drug market

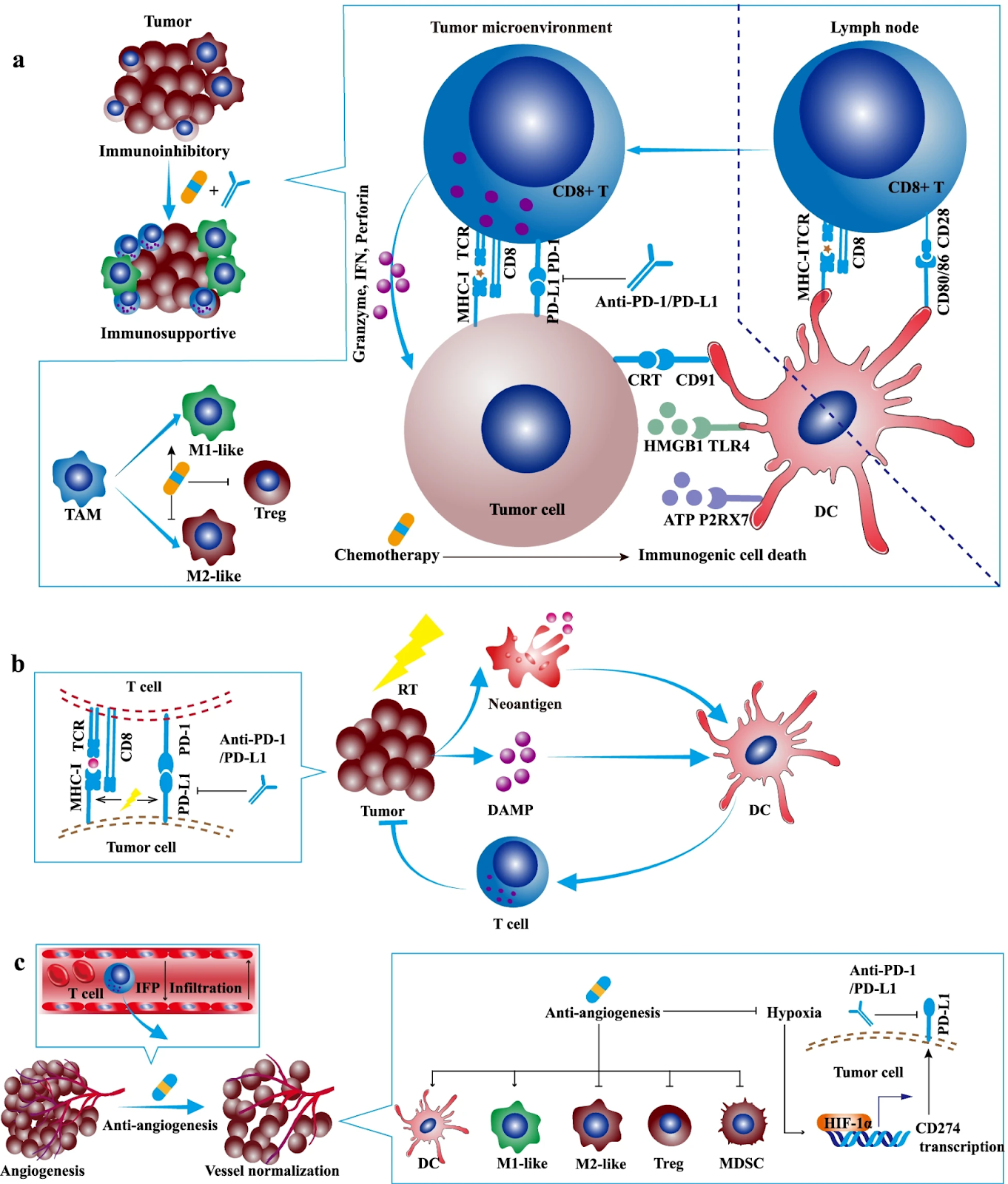

The tricky part of competing in the oncology field is that there are a lot of ongoing therapeutic strategies being pursued in combination with PD-1/PD-L1/L2 inhibitors in several cancer types. This includes approaches meant to improve immune cell recognition of cancer, immune cell activation, direct cancer-killing agents, reducing blood vessel growth to cancers (anti-angiogenic), repolarizing cancer-protecting immune cells, radiotherapy, additional/different checkpoint inhibitors, and more.

Combination strategies with PD-1/PD-L1 blockade: current advances and future directions

Running clinical trials can cost tens to hundreds of millions of dollars, and then biotechs that finally succeed with FDA approval have to compete against big pharma and their sales and distribution powerhouses. But big pharma also often licenses promising drugs from small biotech companies, or buys biotech companies outright to strengthen their positions.

The good news for MAIA is that they have demonstrated early signs of very robust efficacy in the clinic, and across a variety of cancers preclinically. The data is very promising and sets MAIA apart from the crowd.

MAIA’s THIO Cancer Data

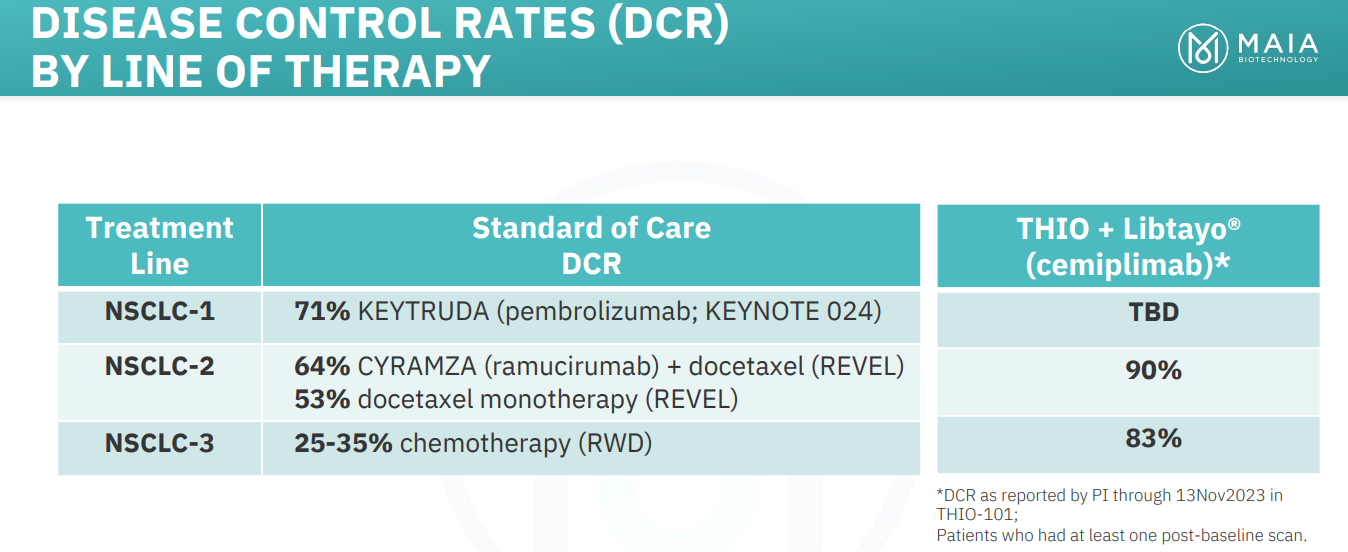

MAIA licensed its oncology drug, THIO (6-THIO-dg) from the University of Texas. They have gathered data suggesting efficacy in patients with varying stages of NSCLC, with unprecedented disease control rates (DCR, i.e. no cancer progression) for an NSCLC trial, and with patients appearing to receive benefits from therapy (i.e. immune memory) long after discontinuing THIO. MAIA has selected a dose (180mg/cycle) for its further studies—this dose showed a preliminary 90% DCR in 2nd line and 83% in 3rd line NSCLC patients. This compares favorably against standard of care (SoC) for each line tested.

MAIA Biotech Showcase Investor Presentation

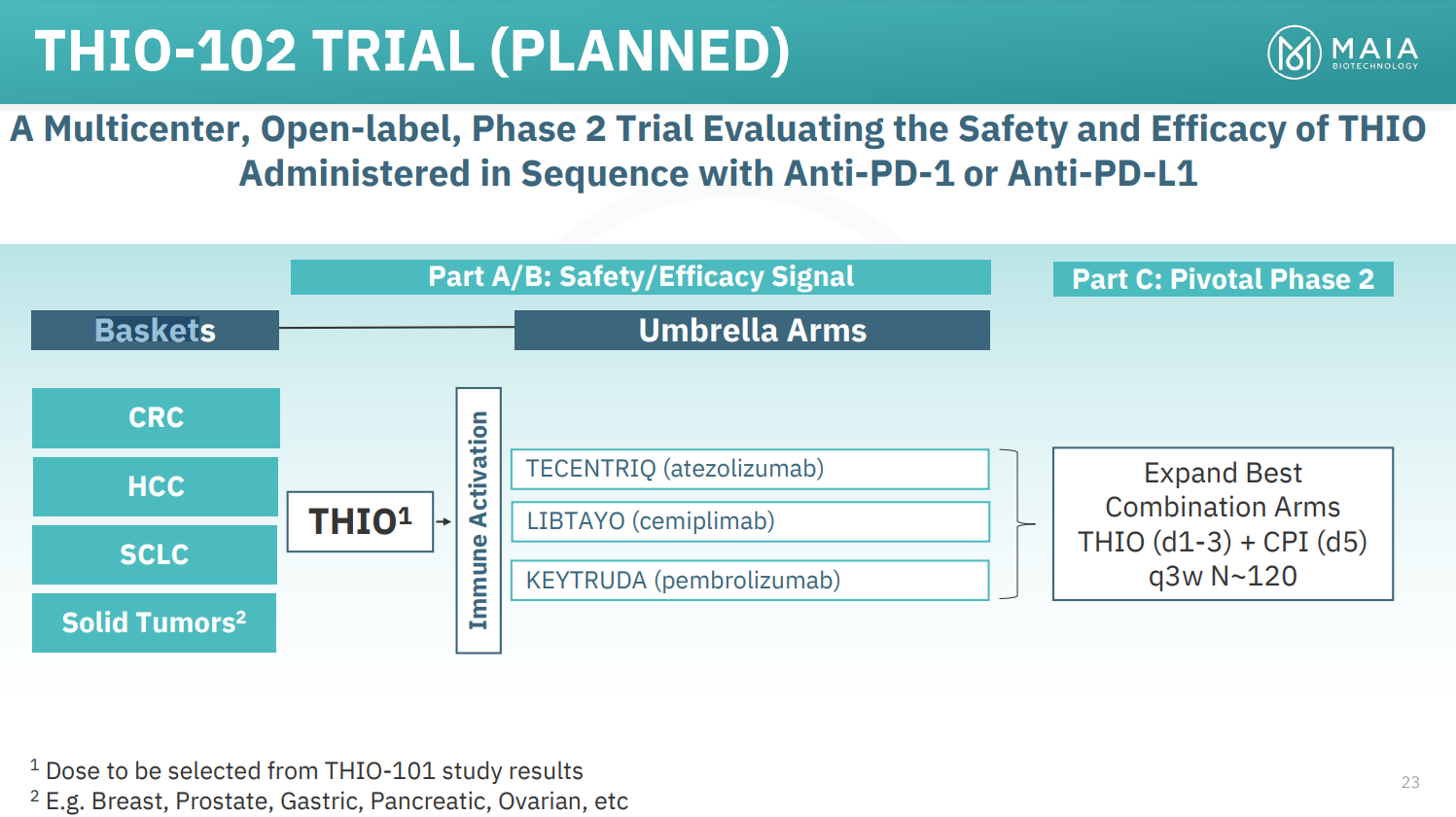

THIO also looks promising based on preclinical tests in several cancers, and as such is expected to enter into a phase 2 basket trial for cancers in combination with several checkpoint inhibitors, including CRC, HCC, and SCLC (and potentially other solid tumors including breast, prostate, gastric, pancreatic, and ovarian cancers). Based on preclinical studies, the FDA has granted the company orphan drug designations for hepatocellular carcinoma (HCC), small cell lung cancer (SCLC), and glioblastoma (GBM). The idea is to explore the most powerful combinations in several cancers and move forward based on that.

Telomere Targeting and its Promise as a Cancer Treatment

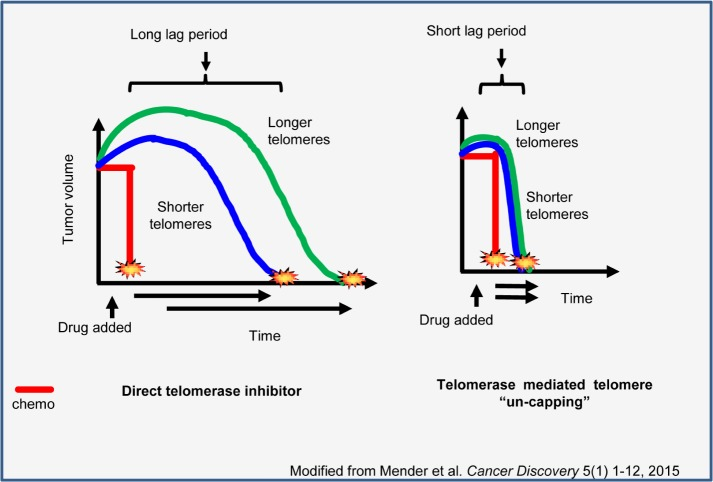

Telomeres are located at the ends of chromosomes and protect the ends of the DNA from being damaged. Telomeres shorten with age (every time a cell divides). Once the telomeres shorten to a critical point, cells undergo replicative senescence or apoptosis. Telomerase is a reverse transcriptase that adds new nucleotides to the ends of telomerase during cell division. Telomerase preferentially acts on the shortest telomeres. In the case of cancer, telomerase is activated to keep the cells alive but also telomeres can remain short due to cancer proliferation. Thus, preventing the regeneration of telomeres is a logical strategy for killing cancer—the cells with short telomeres that are closest to senescence will be most susceptible to cell death if telomerase becomes inactive. This can be done with several methods, including blocking telomerase.

Geron Corporation (Nasdaq: GERN), a billion-dollar biotech company, has worked for years to employ this strategy in several cancers; however, healthy cells need telomerase too, so there are side effects. Also, blocking telomerase takes time to work as one has to wait for cells to undergo multiple divisions and for the cells to undergo apoptosis. As such, Geron has struggled with the dosing of its lead telomerase inhibitor, imetelstat, with patients having to discontinue the drug due to side effects while waiting for a response. MAIA has a better approach to targeting telomeres which avoids these dosing issues.

The reason Geron, MAIA, and the oncology field are interested in telomeres as a cancer target is because this mechanism is required for a cancer to survive. It’s somewhat of a biological lynchpin. MAIA, however, has a more direct and theoretically robust way of targeting telomeres. Their drug, THIO (a nucleoside analog called 6-thio-2’-deoxyguanosine), directly induces telomere damage in one division cycle. The drug is a Trojan horse recognized by telomerase and therefore woven into new telomeres. Once incorporated into the telomeres, it compromises the telomere structure and function. From there, the telomeres uncap, resulting in selective cancer cell death, and an immunogenic DNA damage response. This accomplishes cancer killing without the lag time or adverse effects associated with directly blocking telomerase (like Geron does).

Comparison of two different approaches to telomerase targeted therapies

In addition, 85% of cancers are telomerase positive, and those cancers have continuously active telomerase. In contrast, a small number of healthy cells are telomerase-positive at a given time, so the rapid and selective targeting of cancer is feasible while reducing any side effects. It’s also interesting to note that “normal human cells including stem cells [despite their proliferative capacity] have lower telomerase activity and generally maintain telomeres at longer lengths compared to cancer cells.” This further supports THIO being well-tolerated.

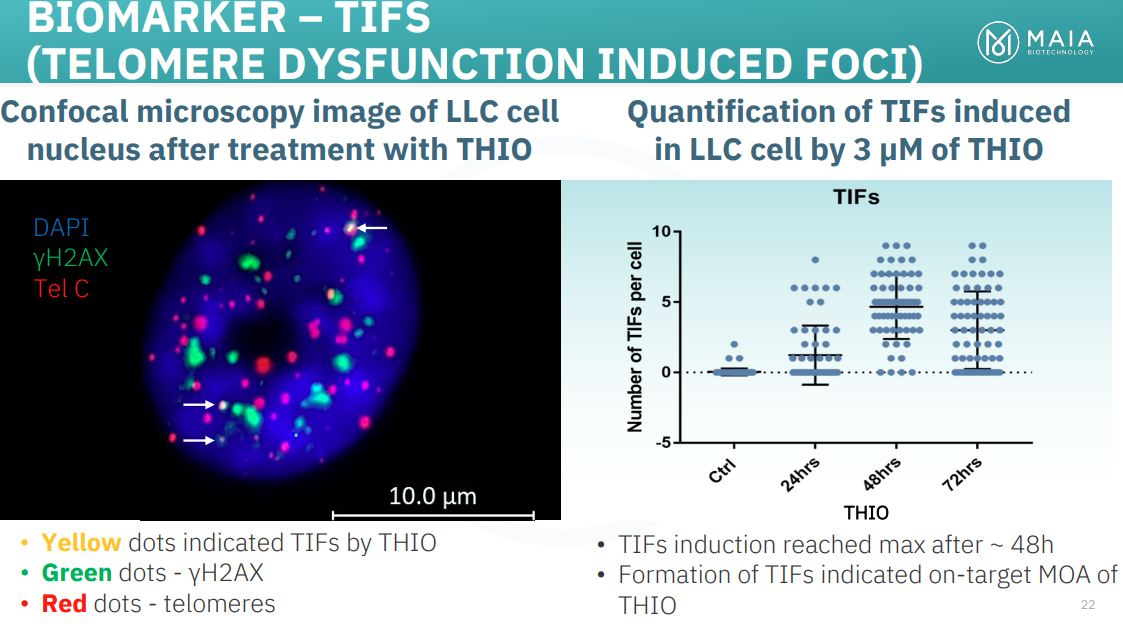

Activity Biomarkers

MAIA has also linked a biomarker to its drug’s (THIO) activity—telomere dysfunction induced foci (aka TIFs). These TIFs are identified where DNA damage markers are colocalized with telomere markers, which implies a damaged telomere. This way, MAIA knows that their drug is directly and rapidly damaging cancer’s telomeres.

Additionally, the robust DNA damage response activates the immune system enough to warrant combination therapy with PD-1 inhibitors (immune checkpoint inhibitors). Preclinical studies have shown that THIO overcomes PD-1 blockade resistance, which means that the combination is working; THIO + PD-1 inhibitors should be better than PD-1 inhibitors alone.

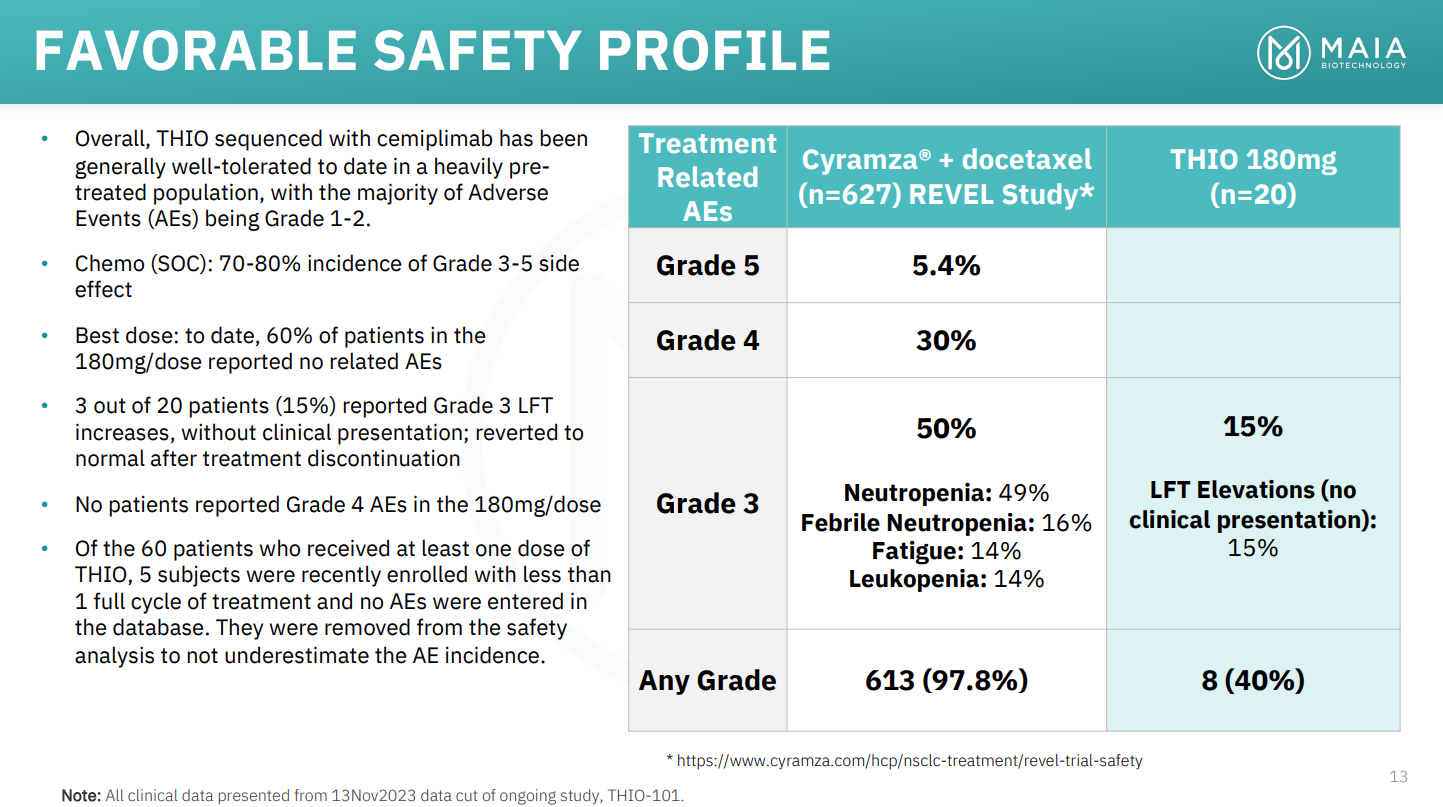

THIO’s Safety Profile

Indeed, congruent with theory, THIO largely does not affect healthy cells. To date, in the company’s ongoing clinical trial, there are about 50 patients with recorded safety scans, with only four of them experiencing grade 3 serious adverse events (SAEs), all of which were liver function tests that had no clinical presentation and all of which resolved within four weeks. All in all, these safety signals probably just indicate an on-target immunogenic effect. This compares very favorably with chemotherapy where up to 70-80% of patients experience SAEs, and a significant percentage of patients die from grade 5 SAE. Furthermore, it is notable that MAIA has chosen to move forward with the 180mg/cycle THIO dose, which exhibited the best clinical results as well as a majority of patients on this dose exhibiting no drug-related SAEs.

MAIA Biotech Showcase Investor Presentation

Clinical Response Rates (ORR) Still in Question: Phase 2 Not Yet Complete

While disease control rates seem promising so far, overall response rate (ORR) is considered a more relevant endpoint for drug efficacy since THIO is a direct tumoricidal agent, not a tumoristatic agent that staves off growth. ORR is also a more commonly chosen primary endpoint in cancer therapy, but in the case of NSCLC, DCR correlates better with survival, which is the ultimate endpoint. However, overall survival data takes a long time to develop compared with DCR and ORR. Because responses to immunotherapy do not always happen immediately, as the study progresses it will become clearer what kind of response rate THIO + cemiplimab can achieve. Additionally, meta analysis has found that, for NSCLC-2nd line treatments, DCR correlates with overall survival (OS) better than ORR correlates with OS.

MAIA Biotech Showcase Investor Presentation

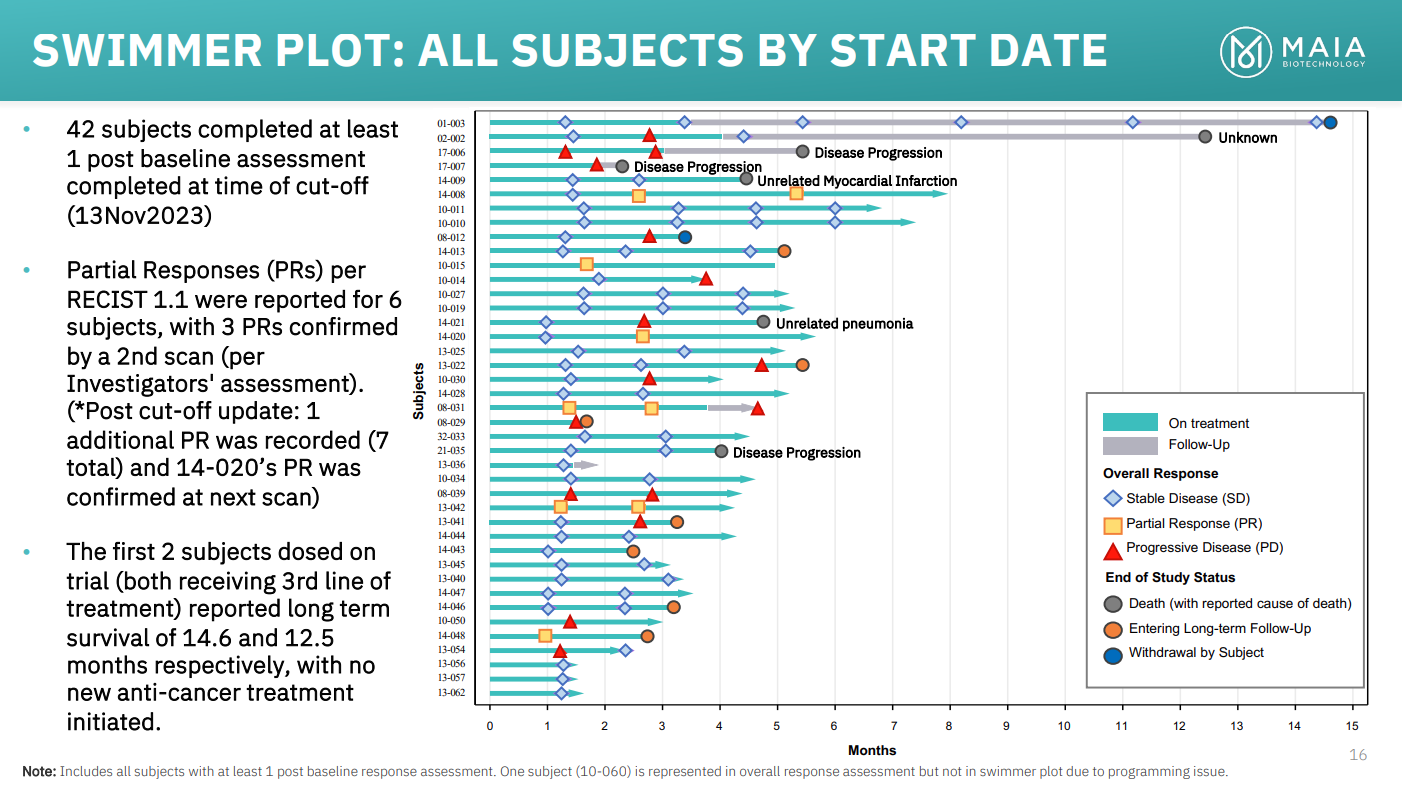

According to the swimmer plot presented at the Biotech Showcase, there have been 7/42 (17%) recorded partial responses in all cases. It appears that, if one subtracts out the NSCLC-3 patients, there are only 2 partial responses of 22 NSCLC-2 patients, or an initial ORR of (11%), versus a progressive disease rate of 7/22 (32%). Certain patients may be undergoing pseudoprogression, where immune cell infiltration and inflammation initially enlarge a tumor before it is destroyed, which can be seen in two of the patients in the swimmer plot above. This phenomenon usually takes place 6-12 weeks from initializing therapy, and correlates with increased survival, though stable disease or partial response after pseudoprogression has been observed up to 420 days after the observed progression. The incidence varies in studies partially because there is no standard test for detecting it; however, generally, it occurs in around 5% of NSCLC patients. More patients may respond to therapy over time, though certainly some could end up progressing over time. Perhaps the data needs more time to mature and potentially is why the stock sold off immediately after the company’s presentation at the Biotech Showcase. Oftentimes, patient scans 2, 3, or 4 (12, 18, or 24 weeks respectively) will finally detect a patient’s response to immunotherapy, so conclusions based on early data are premature.

When contemplating the chances for accelerated approval in NSCLC-2, the chances are very unclear; however, THIO’s DCR in NSCLC being superb, as well as DCR correlating with OS suggest that the drug may be keeping patients alive longer. Overall the picture is not complete or clear so time will tell how well patients respond to THIO and this will elucidate MAIA’s path forward with the FDA. However, the disease control rates still appear to be outperforming the standard of care by a significant margin.

Management

CEO Vlad Vitoc has experience in development, which is critical for microcap biotechnology companies. In his career he has gained experience managing and supporting 20 early, launch, and mature-stage drugs, which have included targeted therapies and immune therapies across more than 25 tumor types, including colorectal cancer, hepatocellular carcinoma, lung cancer, breast cancer, prostate cancer, and renal cell carcinoma, at large pharmaceutical companies including Bayer (OTCMKTS: BAYRY), Astellas (OTCMKTS: ALPMY), and Novartis (NYSE: NVS), so he has direct experience in critical areas relevant to MAIA.

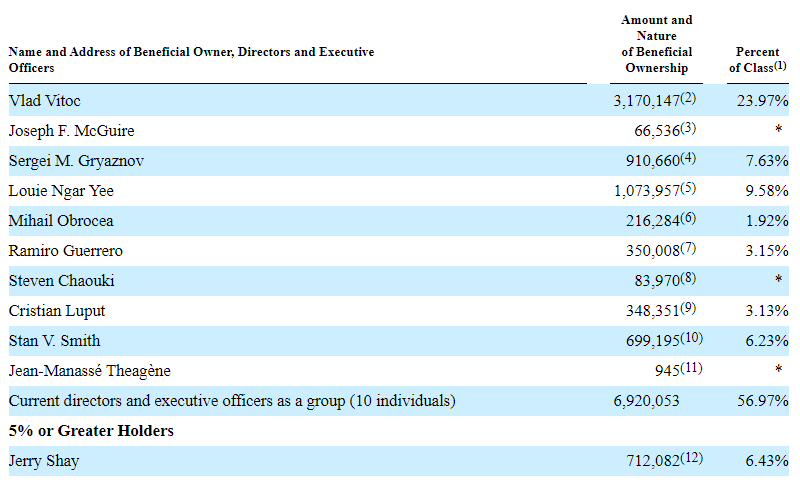

Insider ownership per Yahoo Finance is fairly strong at 24.37%; the chart from the company’s proxy filing below included options that do not appear to have been exercised. The company is paying its directors entirely through options grants ($60,000/year) and management partially through stock and options. This serves as a heavy incentive for success but also significantly dilutes shareholders in a way where directors and executives may receive more options at depressed prices for the total same dollar value.

Insider ownership according to 2023 Schedule 14

The company’s investors are primarily high-net-worth individuals and family offices, i.e. long-term investors. However, there are no big funds invested in MAIA at this time. The company and their investors’ goal is to make their investment exit much bigger than where they are currently. However, when going public, the company’s shares collapsed in line with the vast majority of similar small-cap biotechnology companies. Understandably as a result, recent investors have been not as committed. However, the CEO and his business development team is currently pursuing investment from biotech and pharma companies (multiple CDAs signed), though this can be said for basically all companies in MAIA’s development and financial position.

Business Development

MAIA inked a clinical supply agreement with Regeneron prior to the start of their phase 2 NSCLC trial, whereby Regeneron would supply Libtayo, their PD-1 inhibitor, to MAIA for free for the trial in exchange for limited time exclusivity for combination therapy with THIO in NSCLC:

“Under the terms of the collaboration, MAIA will sponsor and fund the planned clinical trial and Regeneron will provide Libtayo. MAIA maintains global development and commercial rights to THIO and is free to develop the program in combination with other agents outside of NSCLC.”

While this isn’t a huge deal with upfront cash, it goes a long way in reducing trial operational costs as these PD-1 inhibitor biologics are quite expensive and may add up to several million dollars when nearly a hundred patients are enrolled in a trial. With potentially more positive data in hand in the coming months from the THIO-101 phase 2 trial, MAIA may be in the position to perform larger business development deals that make sense for both parties.

MAIA currently burns just over $4 million quarterly and had about $11 million of cash at the end of the 3Q23 when adjusting for the $4 million capital raise the company completed in November. As such they have a limited cash runway and may do another share offering in the coming months if they don’t execute a partnership with big pharma yet.

Valuation

If THIO performs in NSCLC as they expect per their powerpoints, then the results will be similar to the results of Mirati’s KRAS inhibitor, adagrasib. Mirati was bought by Bristol Myers recently for $4.8 billion upfront (and $1 billion in CVRs), presumably for the promise of its KRAS inhibitors, the first of which was approved based on results treating second-line NSCLC patients with KRAS mutations (14% of all NSCLC patients).

In MAIA’s corporate presentation from November 2023, they call out Mirati, Zentalis (Nasdaq: ZNTL), Iovance (Nasdaq: IOVA), Kura Oncology (Nasdaq: KURA), and Turning Point Therapeutics (another company with a TKI for NSCLC, acquired by BMY for $4.1 billion in cash), as comparisons for their potential value. These companies are all American companies and cases of outstanding efficacy demonstrated in cancer without being cell therapies (besides Iovance). MAIA has the potential to demonstrate efficacy similar to these companies’ drugs and therefore, especially with THIO being applicable to 85% of cancers, be a highly valued oncology company. In the comp table below I include these five companies plus Geron Corporation as its a late stage telomerase inhibitor company with a PDUFA date this year. Theoretically, anything Geron achieves with imetelstat, MAIA should be able to do better and therefore it's a good target valuation for MAIA.

|

Company Name |

Market Cap |

Stage |

Enterprise Value |

|

Mirati Therapeutics |

$5.8 billion |

FDA Approved |

$2.21 billion |

|

Zentalis Pharmaceuticals |

$947 million |

Phase 3 |

$476 million |

|

Iovance Biotherapeutics |

$2.14 billion |

Phase 3 |

$1.86 billion |

|

Kura Oncology |

$1.13 billion |

Phase 2 |

$692 million |

|

Turning Point Therapeutics |

$4.1 billion |

Phase 2 |

$3.28 billion |

|

Geron Corporation |

$1.07 billion |

Phase 3 |

$745 million |

These companies are all better funded than MAIA and further along in development, but they serve as a good target or goal of what kind of value MAIA can achieve in the coming year as MAIA completes its phase 2 NSCLC trial. MAIA has concentrated risks in targeting telomeres, but multiple shots on goal against several cancers and in combination with several ICIs; indeed, 100% response rates in preclinical models are uncommon. If THIO works, the company can pursue massive label expansion. In addition, their pipeline, which contains even more potent telomere-targeting agents, will appear even more attractive. 7 of 84 of these molecules demonstrated activity magnitudes of order more potent than THIO. Three of these molecules are moving forward for now, and with proper funding the company will move these into the clinic next year. These molecules are tumoricidal and immune stimulating, similar to Celgene’s Revlimid, which grew to almost $13 billion in annual sales before recently seeing generic competition from Teva (NYSE: TEVA).

With respect to MAIA’s comps, it's important to note that Mirati was in development for first line therapy in NSCLC for just 14% of the patient population when they were acquired, and Turning Point was also acquired before it obtained phase 2 results. Both of these companies had one main asset. So MAIA doesn’t necessarily need to make it all the way to the finish line or have a large pipeline to get a massive valuation. They just need to show Big Pharma that THIO works.

Assuming MAIA can achieve the enterprise value of just ½ the average value of its peers ($1.543 billion / $772 million) in the next year based on outstanding THIO results, there is a lot of room for upside. That is the blue sky scenario. The maximum downside is practically $0 of value, and the approximate chances of success for any given phase 2 trial, historically, is 30%. Given the company had 28.1 million fully diluted shares as of its prospectus detailings its most recent capital raise, the shares could be worth approximately $27.50. The risk-adjusted present value of shares (i.e. what the company should be worth before the full phase 2 results are known), assuming a bit more dilution of about 7 million shares will be required to reach a data readout, would be about $6.6/share, or over 300% upside from these current levels. Considering the potential upside should be weighed against the significant risks of dilution or negative clinical trial results.

Risks

MAIA is a clinical-stage biotech company with limited resources and negative cash flow, similar to most clinical-stage biotech companies. Biotechs like these almost always carry a defined set of risks for investors including topline clinical data releases which are often perceived as binary for the sake of the company's stock price, and fundraising risks which can result in significant dilution of shares. MAIA has additional concentrated risks in its entire pipeline targeting telomeres, but this risk is lower since telomeres are known to be central to cancer as a disease. One additional risk is that the oncology field is highly competitive and companies like MAIA do rely to some extent on support from larger pharma companies to break into the space commercially.

Conclusion

MAIA is pursuing the best strategy when it comes to telomeres in oncology. It has been cited in medical journals that what is necessary for telomeres/telomerase to become a successful cancer target is to improve upon what Geron is doing:

“Clinical trials with telomerase inhibitors have established telomerase as a viable target, but the time lag between drug administration and clinical response is long. Continued treatment is required for successful clinical outcome, which may lead to severe toxicity in patients. Therefore, a major challenge is to develop a telomerase inhibitor that rapidly kills telomerase-positive tumor cells while sparing normal telomerase-carrying cells.”

This is exactly what MAIA is doing. While Geron is in late-stage trials and closer to a potential FDA approval with the ability to become a revenue-producing company, the strategic approach undertaken by MAIA to disrupt telomerase rapidly and without significant hematological adverse effects should make its THIO asset theoretically much more valuable than imetelstat. In this way, the value disparity between GERN and MAIA suggests that MAIA is significantly undervalued, and at least has significant upside potential to reach a market cap equal to or greater than GERN based on the successful completion of phase 2 and phase 3 pivotal trials in combination with checkpoint inhibitors for cancer immunotherapy.

Other comparisons to companies with outstanding oncology data in large cancer markets support immense potential value realization with MAIA. The reasons the company’s shares aren’t already trading in the hundreds of millions or billions are twofold: 1) because the data needs to become clearer with a larger dataset of stage 2 NSCLC patients to adequately compare to standard of care, and 2) because the biotech markets have bottomed out, especially with regards to smaller biotech companies struggling to find funds for R&D. Positive data or improvement in the company’s financial position through a friendly financing or a business development deal with major pharma could rocket shares higher towards the company’s true value. In lieu of a major partnership, the company has a funding gap so careful investment position sizing for risk tolerance is warranted.

Comments

Log in or sign up to join the conversation.