Image Source: Pexels

It is reasonable for earnings estimates to be coming down in the face of Fed tightening. And the central bank has more than demonstrated its resolve by front-loading the tightening process. Monetary policy works with a lag, but there is no question that higher interest rates will lead to slower economic growth which, in turn, will show up in moderating corporate revenue and earnings growth.

There are some in the market that can’t see the Fed getting on top of the inflation problem without pushing the economy into a recession. Variations of this view show up in public comments from prominent business leaders and even the bond market where the yield curve appears again to be heading towards inversion.

A recessionary outcome for the economy is neither the consensus view nor what the Zacks economic team is projecting at present. But what everyone agrees on, however, is that the economy should start slowing as the cumulative effect of higher interest rates seep through into the economy.

We are not there yet, but we are starting to see some tell-tale signs of moderation, with some companies announcing hiring freezes or even lay-offs. Financial conditions have tightened already and we are starting to see its effects on all aspects of the housing industry, the most rate-sensitive part of the economy. If consumer spending is as tied to consumer confidence, as we all intuitively feel should be the case, then it’s only a matter of time after the latest University of Michigan survey before spending slows.

It is still early, but these signs suggest that the Fed’s actions are steering the economy in the desirable direction. The market should have ‘gotten the memo’ of the Fed’s resolve to fight inflation after the largest rate hike since 1994.

With respect to the evolution of earnings estimates, we should point out that while estimates have come down a bit, they are nowhere near what would be consistent with a significant economic slowdown.

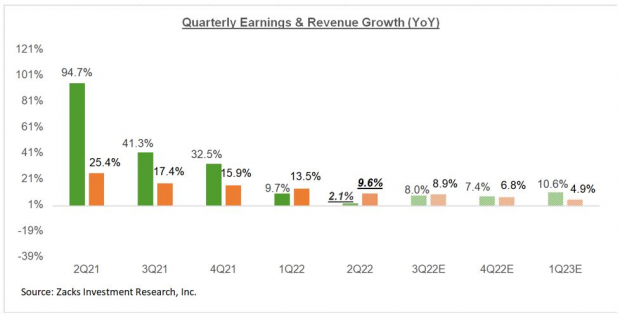

For example, 2022 Q2 earnings for the S&P 500 index companies are currently expected to increase +2.1% from the year-earlier level on +9.6% higher revenues.

If we look at the revisions trend in the aggregate, at the S&P 500 level, we don’t see a lot of movement, as you can see in the chart below that plots the evolution of aggregate Q2 earnings growth estimates for the index since the start of 2022.

Image Source: Zacks Investment Research

What this chart is showing is that expected Q2 earnings growth in the aggregate has declined from +2.8% on March 30th to +2.1% today (up from +1.9% last week).

That said, there are plenty of cross-currents at the sector level, with positive revisions to the Energy sector offsetting declines in most other sectors.

Second-quarter 2022 Earnings estimates for the Zacks Energy sector have increased +49.2% since the start of April.

Energy is not the only sector that has enjoyed positive Q2 estimate revisions; there are 5 other sectors whose estimates have gone up in varying magnitudes.

Since the start of Q2 on April 1st, earnings estimates have gone up for the Transportation, Basic Materials, Autos, Construction, and Consumer Staples sectors. Of these 5 sectors, the upgrade to the Q2 earnings outlook is particularly significant for the Transportation and Basic Materials sectors.

If we look at the aggregate Q2 revisions, after excluding the Energy sector from the mix, then the picture changes, as you can see below.

Image Source: Zacks Investment Research

Pretty much the same trend is at play with the revisions trend on an annual basis, with aggregate estimates stable or even modestly up since the start of the year, but starting to come down on an ex-Energy basis.

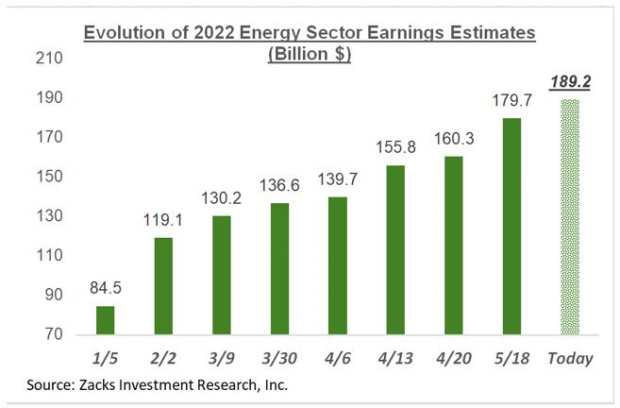

I will not share those charts here to keep the length of this piece manageable, but I think it will be useful for you to see what has happened to full-year 2022 earnings estimates for the Energy sector since the start of the year.

Image Source: Zacks Investment Research

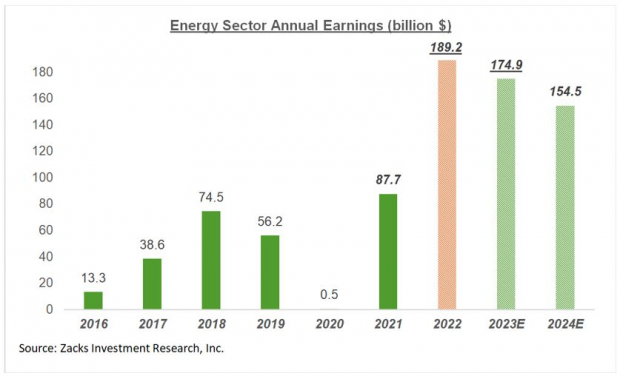

Any way you look at it, the Energy sector is in a good place at present, with a very strong earnings outlook, as a relatively long-term view of the sector’s earnings picture shows below.

Image Source: Zacks Investment Research

This Week’s Earnings Results

We have 6 S&P 500 members on deck to report quarterly results this week. Of these 6, we will be closely watching management commentary and guidance from three – Accenture (ACN - Free Report), Lennar (LEN - Free Report), and FedEx (FDX - Free Report) – to add to visibility about some of the big-picture questions that the market has been grappling with lately.

We heard a fair amount from FedEx on their recent ‘analyst day’, but Accenture and Lennar will give us more color on what they are seeing with business trends in Tech spending and the housing space. On the housing side, we will also be getting a quarterly report from KB Home (KBH - Free Report) this week, which should help us get a sense of the fast-evolving housing scene.

With respect to the earnings outlook for the Tech sector, the June quarter is typically a seasonally weak period. And we have started hearing about the impact of the strong U.S. Dollar on profitability, as we heard from Microsoft (MSFT - Free Report) recently and from Adobe (ADBE - Free Report) in its quarterly release.

Corporate guidance is always the most important part of any quarterly release. But I strongly feel that it will be even more significant this time around given how keyed in all of us are on reading earnings tea leaves.

Q2 Earnings Season Scorecard

We mentioned the Adobe earnings report earlier, which was for the company’s fiscal period ending in May. In addition to Adobe, we have recently seen fiscal May-quarter results from three other S&P 500 members, namely Costco, AutoZone and Oracle. All of these fiscal May-quarter results get clubbed with the June-quarter results and form part of our 2022 Q2 tally.

For these 4 index members that have reported Q2 results already, total earnings are down -4.2% from the same period last year on +13.6% higher revenues, with all 4 beating both EPS and revenue estimates.

The comparison charts below put the Q2 earnings and revenue growth rates for these 4 index members in a historical context.

Image Source: Zacks Investment Research

We are not drawing any conclusions from this small and unrepresentative sample, but it nevertheless gives us a good sense of the ongoing margin pressures. As you can see, year-over-year growth of +13.6% for these 4 index members has not been enough to produce bottom-line growth.

MSFTThe Current Earnings Backdrop

The chart below shows current expectations (and actuals) on a quarterly basis.

Image Source: Zacks Investment Research

Please note that the +2.1% earnings growth expected in 2022 Q2 is solely due to strong gains in the Energy sector. On an ex-Energy basis, Q2 earnings growth drops to a decline of -5.2%.

The chart below presents the earnings picture on an annual basis.

Image Source: Zacks Investment Research

Comments

Log in or sign up to join the conversation.