Image: Bigstock

Costco Wholesale Corporation (COST - Free Report), renowned for its membership-based warehouse model, recently released its sales results for September. This data offers fresh insights into the company's performance within a rapidly evolving retail landscape. As investors evaluate the performance, a crucial question arises: Should they buy, hold, or sell Costco stock?

The September sales figures arrive at a moment when inflation, ongoing geopolitical tensions, and a contentious presidential election are influencing consumer behavior. Despite these dynamics, Costco has positioned itself to meet the demands of price-conscious consumers by offering quality products at competitive prices. This strategy not only attracts new customers, but also nurtures strong loyalty among existing members.

Costco’s September Sales Reflect Continued Demand

Costco's ability to offer products at lower prices than many of its competitors is a major draw for its customer base. The company’s bulk purchasing model allows it to negotiate favorable terms with suppliers and pass the savings on to consumers. This pricing strategy attracts a broad demographic, from budget-conscious families to small businesses, enhancing Costco's appeal across various market segments.

For the five weeks ending Oct. 6, comparable sales rose 6.7%. This stellar performance follows consecutive increases of 5% and 5.2% in August and July, respectively. September’s total and comparable retail sales saw a boost of about 2% in the United States and one and 1.5% globally, driven by solid consumer demand in the final week of the month, largely influenced by Hurricane Helene and disruptions from port strikes.

When adjusting for the effects of gasoline prices and foreign exchange rates, Costco’s comparable sales paint an even more impressive picture. The company’s total comparable sales, excluding these external factors, increased by 8.9% in the last month.

As a result, Costco's net sales for September rose 9%, reaching $24.62 billion, up from $22.59 billion in the same period last year. This follows a sales improvement of 7.1% reported in both August and July, reflecting a strong and consistent sales performance in the past few months.

Costco’s Membership Model Pivotal to Business Strategy

Costco’s membership model, where customers pay an annual fee for access to its warehouse stores, ensures a steady revenue stream. This is a unique advantage that sets Costco apart from many other retailers, providing it with a more predictable income, even in uncertain economic conditions. The company benefits from substantial recurring revenues through membership fees, with renewal rates exceeding 90% in key markets such as the United States and Canada.

Last month, Costco raised its membership fees for U.S. and Canadian customers. Gold Star, Business, and Business add-on memberships now cost $65 annually, reflecting a $5 increase, while Executive Memberships have increased from $120 to $130. This move also comes with a boost in the maximum annual 2% Reward for Executive Members, up from $1,000 to $1,250.

We note that Costco ended the final quarter of fiscal 2024 with 76.2 million paid household members, up 7.3% from the prior year. Executive memberships, a more profitable category for Costco, grew by 9.6% year-over-year to reach 35.4 million, now accounting for 46.5% of all paid members and driving 73.5% of worldwide sales.

Can Costco Maintain Its Edge?

Costco's impressive sales figures are part of a larger retail picture where competition is intensifying. Rivals like Walmart (WMT - Free Report) and BJ’s Wholesale Club (BJ - Free Report), which also cater to value-conscious consumers, are investing in expanding their e-commerce capabilities and enhancing customer experience. Amazon (AMZN - Free Report) continues to dominate online shopping, pushing traditional retailers to innovate rapidly.

Costco’s membership model and bulk-buying advantages give it a notable edge in customer retention and operational efficiency. However, to stay ahead, Costco must effectively leverage its strengths while adapting to shifting consumer behaviors and technological advancements.

Costco’s efforts in expanding its online presence, which include improving its digital shopping experience and logistics, are key to its success. The company registered a 22.9% increase in e-commerce comparable sales in September.

Is Costco’s Stock Price Overvalued or Premium Justified?

Costco stock has been a standout performer, with shares rallying 24.8% over the past six months, outpacing the industry's rise of 14.4%. This impressive growth underscores investor confidence in Costco’s business model.

Image Source: Zacks Investment Research

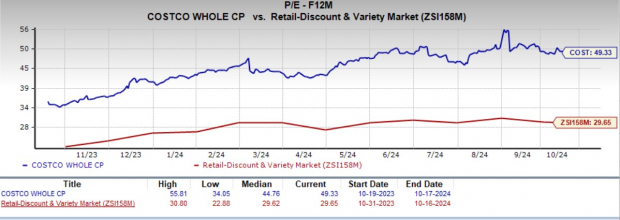

However, the stock has recently been trading at a significant premium to its peers. Costco's forward 12-month price-to-earnings ratio stands at 49.33, higher than the industry’s ratio of 29.65 and the S&P 500's ratio of 22.2.

Image Source: Zacks Investment Research

Now the question arises: Is Costco’s recent price warranted, or is it overvalued in today’s market?

Well, Costco’s premium valuation reflects investor confidence in the company’s ability to deliver consistent growth and maintain its competitive advantage. While the stock’s recent price may seem high, its robust business model, strong customer base, and reliable revenue streams justify the premium.

Costco Stock: Buy, Hold or Sell?

Costco's robust membership model, combined with its ability to adapt to evolving market trends, solidifies its position as a leader in the retail sector. Although the stock's premium valuation may cause hesitation among some investors, Costco's favorable product mix, consistent store traffic, and strong pricing power mitigate these concerns.

Its solid liquidity position reinforces the company's capacity to navigate economic uncertainties effectively. With a Zacks Rank of #2 (Buy), Costco demonstrates strong potential for continued growth, suggesting that investors may find compelling upside opportunities in its stock.

More By This Author:

Netflix Earnings Review: Still Winning The Streaming Wars?2 Stocks To Watch After Blasting Q3 Earnings Expectations: AA, TCBI

Bull Of The Day: Vertex

Comments

Log in or sign up to join the conversation.