Is American Express Stock: 5 Things Investors Might Be Missing In 2025

Image Source: Unsplash

American Express (AXP) has built its reputation on prestige, loyalty, and spending power. Known for its iconic Platinum and Centurion cards, the company isn’t just a payment processor, it’s a financial lifestyle brand that commands a premium audience.

In Q2 2025, American Express delivered another strong performance, with earnings and revenue slightly beating expectations. Return on equity remains well above peers at 36.3%, and net card fee growth surged 20% thanks to a rising number of premium cardholders.

Yet, despite the solid numbers, Wall Street’s reaction was muted. Shares slipped modestly following the results, not because of bad news, but because expectations were already sky high.

This begs the question: is the market underestimating American Express’ long-term value?

While Visa (V) and Mastercard (MA) focus on transaction volume, American Express has a different game plan. Its closed-loop model allows it to capture more economic profit per transaction, owning the entire customer journey – from issuing the card to processing the payment to managing merchant relationships.

Combine that with a loyal, high spending user base and expanding international card volume, and you’ve got a business with moat like durability.

Still, the stock isn’t without challenges. Growth in commercial card spending is slowing, and global acceptance, especially outside the U.S., still lags competitors. But with card refreshes planned and premium customer acquisition on the rise, Amex is quietly positioning itself for long term momentum that may not yet be fully priced in.

Let’s take a deeper look at American Express using the IDDA Framework: Capital, Intentional, Fundamentals, Sentimental, and Technical.

IDDA Point 1 & 2: Capital & Intentional

Before investing in American Express, ask yourself:

Do you want exposure to a company that benefits from both card fees and lending but isn’t overly reliant on interest income?

Are you looking to align with a brand that targets high income consumers and businesses?

Do you believe lifestyle driven financial services are the future of loyalty and retention?

American Express isn’t trying to serve everyone, it’s doubling down on premium. Over 70% of new card accounts come from fee paying products. Its intentional strategy focuses on acquiring high spending consumers and small businesses that don’t carry revolving balances but use their cards often and heavily. These customers are less sensitive to interest rates and more loyal to brands that offer experiences, rewards, and prestige.

By offering luxury travel perks, curated partnerships (like Fine Hotels & Resorts), and elevated digital experiences, Amex has carved out a niche that’s hard for others to replicate. It’s not chasing volume, it’s cultivating value.

IDDA Point 3: Fundamentals

American Express has experienced several years of strong fundamental growth, with new card acquisitions and loan growth outpacing peers. While traditionally a payment network with only about 25% of revenue from net interest income, the company’s strategic shift toward a younger, more credit-active customer base led to a 26.1% compound annual growth rate in net interest income from 2021 to 2024.

American Express had a strong Q2, with revenue up 9% to $17.9 billion and earnings per share rising 17% to $4.08. The company delivered a solid 36.3% return on equity. Growth came from strong customer acquisition where cards in use grew 4%, and 71% of new accounts were fee-paying, driving a 20% rise in net card fees. International spending rose 12%, helping balance weak commercial card use, which stayed in the low single digits.

Looking ahead, American Express plans to refresh its U.S. Platinum card line by year-end, which typically includes higher annual fees, a move expected to sustain strong card fee growth into 2026.

American Express remains fundamentally strong due to its premium customer base of high-spending individuals and small businesses. This spending power makes the company appealing to merchants and has enabled valuable partnerships. Furthermore, the company’s cardholder base has expanded in the mid-single digits as its repositioning toward premium lifestyle products continues to attract younger consumers.

American Express possesses a wide economic moat built on a unique closed-loop operating model, enabling it to capture the full economic value from each card transaction by acting as issuer, network, and merchant partner. This model generates roughly 75% of its revenue from non interest income, making it less reliant on net interest income than peers and well positioned to serve high income consumers and businesses. Its entrenched network benefits from strong brand positioning, premium card offerings, and long-standing partnerships, such as with Delta and its Fine Hotels & Resorts program, which create network effects and customer loyalty that are hard for competitors to replicate.

On the commercial side, American Express holds a dominant position by offering SME focused cards with high spending limits, flexible repayment structures, and built-in rewards, creating significant switching costs. This fully integrated structure supports durable competitive advantages and high returns on equity, reinforcing American Express’s leadership in both consumer and commercial payments.

Fundamental Risk: Low – Medium

IDDA Point 4: Sentimental

Strengths

Closed-Loop Advantage: American Express’ closed-loop network lets it capture more profit per transaction compared to rivals.

Good Financials & Strong Q2 Earnings: The company reported solid financial performance, with strong Q2 results and consistent profitability.

Successful Brand Shift: Its repositioning toward lifestyle-focused cards has boosted new card acquisitions, especially among younger customers.

Risks

Limited Product Scope: Compared to competitors, American Express offers fewer deposit and lending products, reducing diversification.

Weaker Global Reach: While U.S. acceptance has improved, international merchant acceptance still lags behind Visa and Mastercard.

Economic Sensitivity: The company’s spending-driven model is vulnerable to downturns, with commercial card growth already slowing.

While the Q2 results slightly beat expectations, investor sentiment was cautious. Shares dipped modestly following the announcement, likely reflecting already high expectations built on the company’s consistent earnings growth and strong track record. The market appears to be pricing in a continuation of strong performance, meaning even solid results may not be enough to spark upside in the near term.

Analysts see the stock as modestly overvalued at current levels, with sentiment hinging on American Express’s ability to maintain spending growth amid potential headwinds. The upcoming card refresh and ongoing fee momentum are positive drivers, but with net interest income growth slowing, the company faces pressure to keep up its pace of operational execution to meet revenue guidance.

Sentimental Risk: Medium

IDDA Point 5: Technical

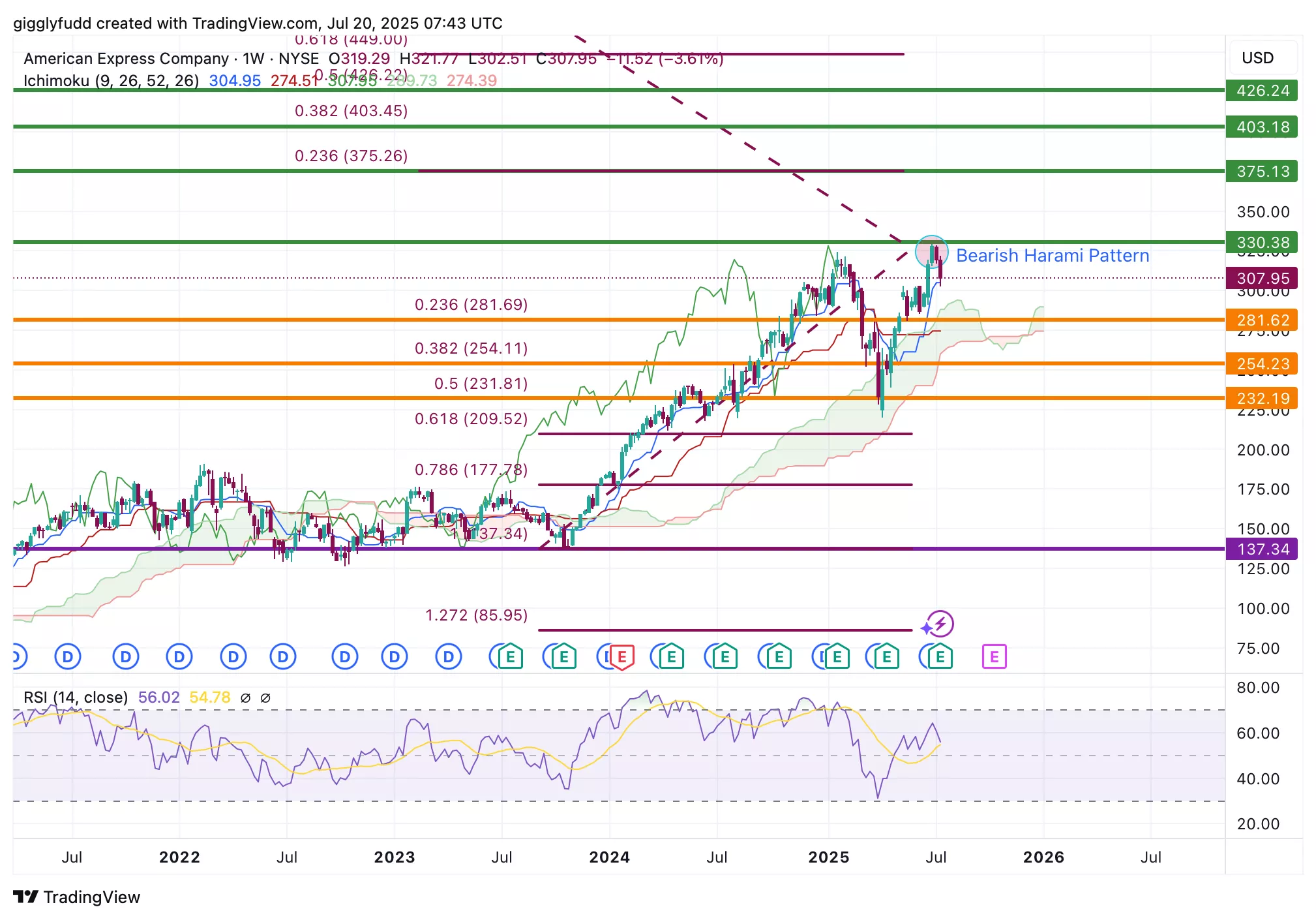

On the weekly chart:

The future Ichimoku cloud is bullish, indicating continued upward momentum.

Price action is mostly holding above the cloud, which continues to act as a strong support zone.

The recent formation of a Bearish Harami pattern (a large bullish candlestick followed by a smaller bearish candlestick – circled in red) suggests a potential short-term pullback.

On the weekly chart, American Express (AMEX) experienced a period of consolidation between 2021 and 2023. From 2024 onward, the stock began trending upwards, gaining over 200%. In 2025, it pulled back by as much as 50%, testing the Ichimoku cloud as a support zone, which successfully held. Since then, the stock has resumed its uptrend, recently reaching a new high of $330.

The future Ichimoku cloud remains bullish, supporting continued upward momentum, with the candlesticks positioned above the cloud further reinforcing the bullish outlook. The cloud continues to act as a strong support zone in the long term.

A Bearish Harami pattern has recently formed, signaling a possible shift from an uptrend to a downtrend. It consists of a large bullish candle followed by a smaller bearish candle that sits within the body of the first. This indicates weakening buying pressure and could be an early sign of a pullback, potentially offering an opportunity for investors looking to buy the dip.

(Click on image to enlarge)

Investors looking to get in KO can consider these Buy Limit Entries:

Current market price 307.95 (High Risk – FOMO entry)

281.62 (High Risk)

254.23 (Medium Risk)

232.19 (Low Risk)

Investors looking to take profit can consider these Sell Limit Levels:

375.13

403.18

426.24

Hold long term

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your

- CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: Medium

Final Thoughts on American Express (AXP)

American Express (AXP) continues to cement its position as a premium financial brand with a loyal, high-spending customer base.

Its unique closed-loop model allows it to capture more profit per transaction compared to traditional credit card networks. In Q2 2025, Amex delivered strong results whereby revenue rose 9% year-over-year to $17.9B and adjusted EPS jumped 17%, driven by premium card acquisitions and a 20% surge in net card fees.

Its return on equity remains high at 36.3%. Yet despite this performance, the stock dipped slightly after earnings. Why? Because expectations were already sky high, and the market seems to be pricing in perfection.

Here are 5 key things Wall Street might be missing:

- Strong Q2 Earnings Masked by High Expectations

Amex beat on revenue and earnings, but shares dipped due to elevated expectations. Despite consistent profitability and high ROE, investor sentiment remains cautious, possibly overlooking the company’s long-term strength. - The Power of the Closed-Loop Model

Unlike Visa and Mastercard, Amex controls the entire transaction flow, issuing the card, running the network, and managing the merchant relationship. This enables deeper customer insights and higher margins, a structural advantage that’s often underappreciated. - Premium Customer Base = Sticky Revenue

With over 70% of new accounts being fee-paying and average annual spending per cardholder exceeding $24K, Amex’s focus on high-income individuals and small businesses results in resilient, high-quality revenue. - Underrated International Growth Potential

While global acceptance still trails Visa and Mastercard, international card spending jumped 12% year-over-year. As emerging markets grow wealthier, this segment could be a major growth engine. - Upcoming Product Refreshes Could Drive Fee Growth

Amex is planning a refresh of its U.S. Platinum cards by year-end, which typically includes fee hikes and added perks. This move is expected to extend strong net card fee growth into 2026 and beyond.

AXP remains in a long term uptrend after breaking out of a two year consolidation phase (2021–2023). Since early 2024, the stock has gained over 200%, with a healthy yet substantial pullback in 2025 that tested and held the Ichimoku cloud as support.

It recently hit a new high of $330. However, a Bearish Harami pattern has formed on the weekly chart, signaling a possible short-term pullback. Still, with price action above the cloud and the future cloud looking bullish, the long-term trend remains intact.

Recommendation: Buy or Hold / Long Term Accumulation Play

American Express offers a compelling opportunity for long-term investors who value strong fundamentals, moat driven economics, and premium brand positioning.

While short-term gains may be capped due to high expectations and commercial card softness, its structural advantages, global growth runway, and loyal customer base make AXP a standout compounder in any diversified portfolio.

Overall Stock Risk: Medium

More By This Author:

Forget Nvidia? Why Savvy Investors Are Quietly Buying TSM Stock Right Now3 Strategic Shifts That Could Put SoFi Stock Ahead Of The Pack

Fluor Stock: A Boring Business That Might Outrun The Market?