In the short run, the market is a voting machine; in the long run, a weighing machine – Ben Graham

The great Ben Graham – teacher of Warren Buffett – encapsulated the two perennial approaches to investing in the quote above. Momentum investors invest in the hot stocks of the moment, riding the momentum caused by crowd psychology. Value investors play the long game, looking for mismatches between current prices and intrinsic value, waiting for the market to see what they see. Both approaches work. Which one you choose is largely a matter of temperament. Personally, I am a value investor but it’s not for everyone.

William O’Neil, the founder of Investors Business Daily, wrote the Bible of momentum investing How To Make Money In Stocks (1988). Mark Minervini is perhaps the greatest current practitioner of this style (see his Trade Like A Stock Market Wizard (2013)). As the market has become more casino-like, most have gravitated toward this type of investing, regardless of whether they identify as momentum investors or not. Trend following, for example, is a form of momentum investing.

O’Neil called is formula CANSLIM. C = Current Quarterly Earnings. A = Annual Earnings. N = New Products, Services or Management. S = Supply and Demand. L = Leaders vs Laggards. I = Institutional Support. M = Overall Market Direction. The key metric here is Relative Strength. O’Neil was interested in buying the stocks that are performing the best right now. His primary concern is how the stock is acting right now, not underlying value.

The risk with momentum investing is that the crowd can push stocks that don’t deserve it well beyond their intrinsic value – only to have them subsequently crash. Momentum investors ride the wave on the way up but need a disciplined way to get out to avoid the crash. Most do this by placing stops not far below their purchase price – generally 7% – and moving these stops up as the stock rises.

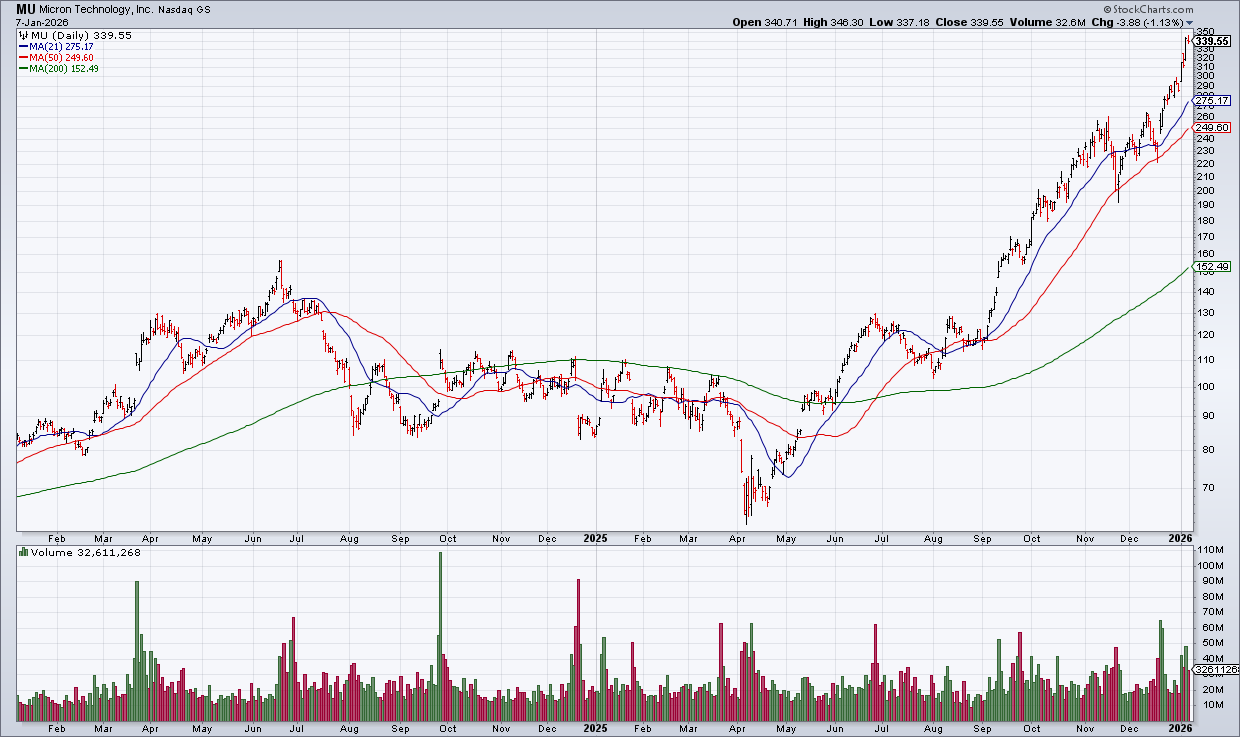

(Click on image to enlarge)

A perfect example of a momentum stock in the current market is Micron (MU). MU checks all of O’Neil’s boxes and is obviously working at the moment. But I promise you that there will be a nasty shakeout in the not too distant future. While MU just reported a blowout quarter, it is more than priced in and this kind of price action is not sustainable. Successful momentum investors understand this. They ride it up but will not ride it all the way back down.

Ben Graham’s The Intelligent Investor (1934) is the Bible of value investing – though the disciplined has evolved since then primarily due to the innovations of Warren Buffett. Whereas Ben Graham sought to buy stocks that were statistically cheap and flip them when reached intrinsic value, Buffett evolved the approach to focus on qualitative factors and compounders. Buffett beautifully summed up his approach in this aphorism: “It is better to buy a wonderful company at a fair price, than a fair company at a wonderful price”.

High quality compounders can grow earnings over long periods of time resulting in massive cumulative moves in their stock price as price follows earnings over the long term. In other words, value investors are interested in the weighing machine aspect of the market as opposed to the voting machine aspect.

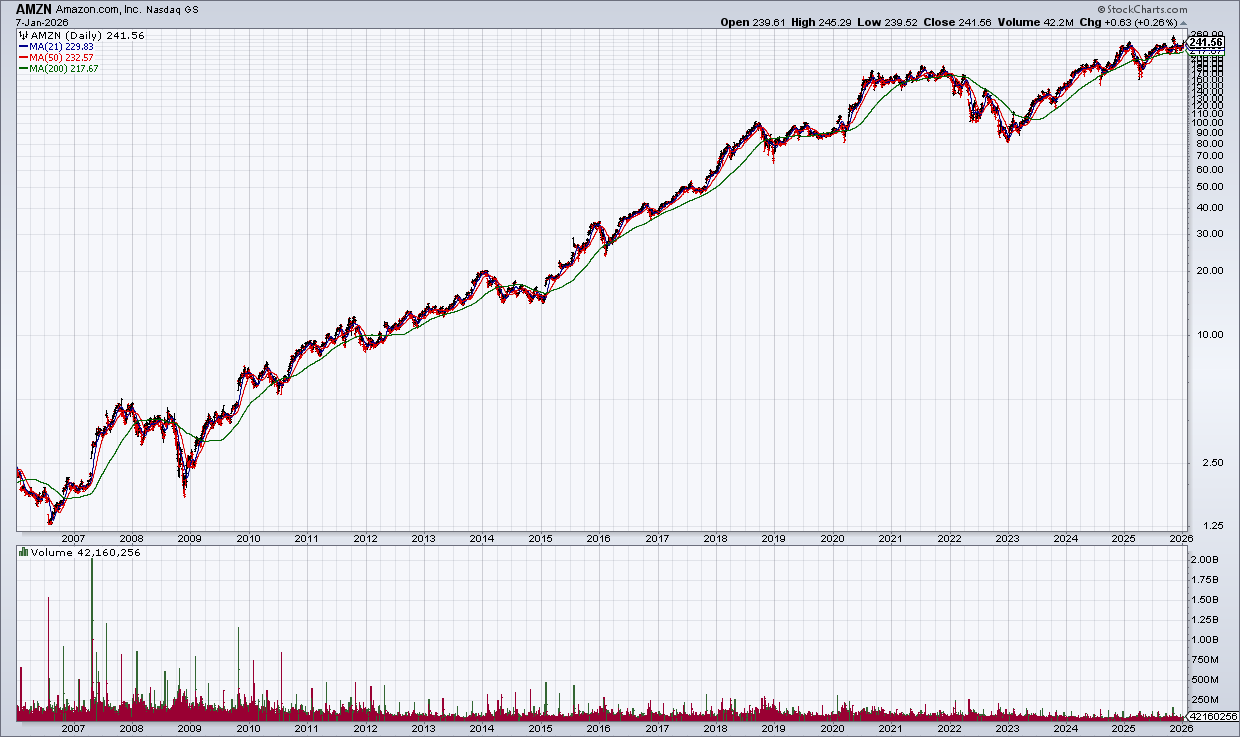

(Click on image to enlarge)

Think of Apple, Google or Amazon. While momentum investors would have been shaken out of these stocks many times over the years, value investors who believed in these companies could have ridden them for years to enormous profits. For example, Nick Sleep and Qais Zakaria of the Nomad Investment Partnership (2001-2014) made a big chunk of their profits simply by being massively overweight Amazon – and holding on.

Another approach – that has not worked for a very long time but whose time may have come – is macro. Macro investors try to profit from macroeconomic forces like interest rates, inflation, economic growth and decline, etc…

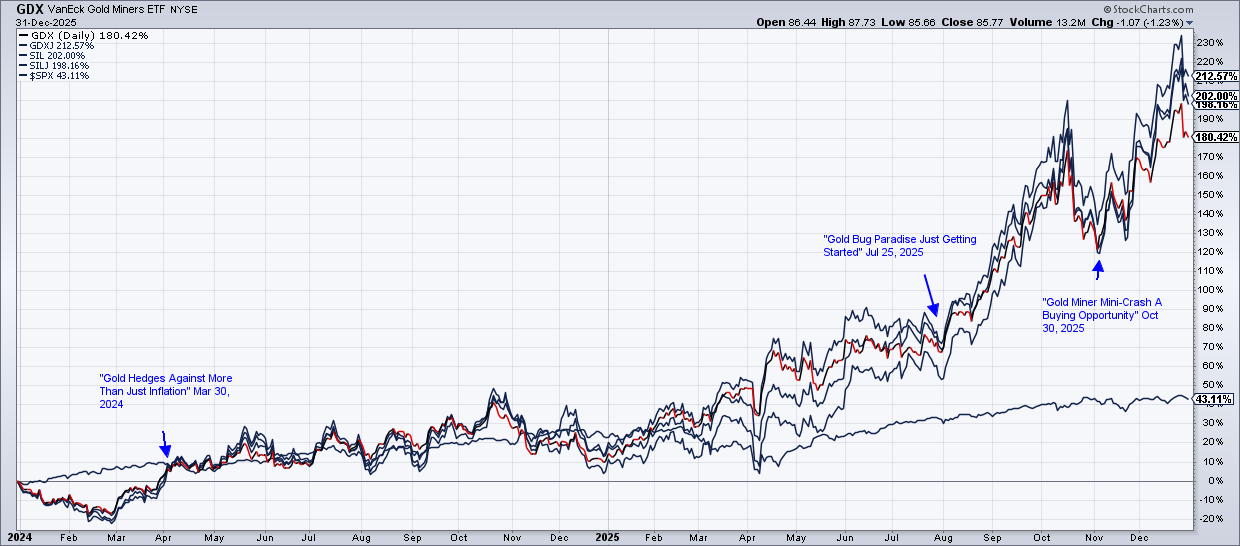

The current move in the precious metals is a perfect example. This move is the result of concerns about inflation and the degradation of fiat currency – concerns that have been around for a long time but are only recently beginning to be priced in by the market. (For more on the current macro environment see “The Roots Of Financial Nihilism”, December 22, 2025).

(Click on image to enlarge)

More By This Author:

The State Of The Market: Can The S&P Keep Going Up Without Tech Participation?The Case For MDLZ

Year-End Letter: Portfolio Returns 38% In 2025

Comments

Log in or sign up to join the conversation.