Image Source: Pexels

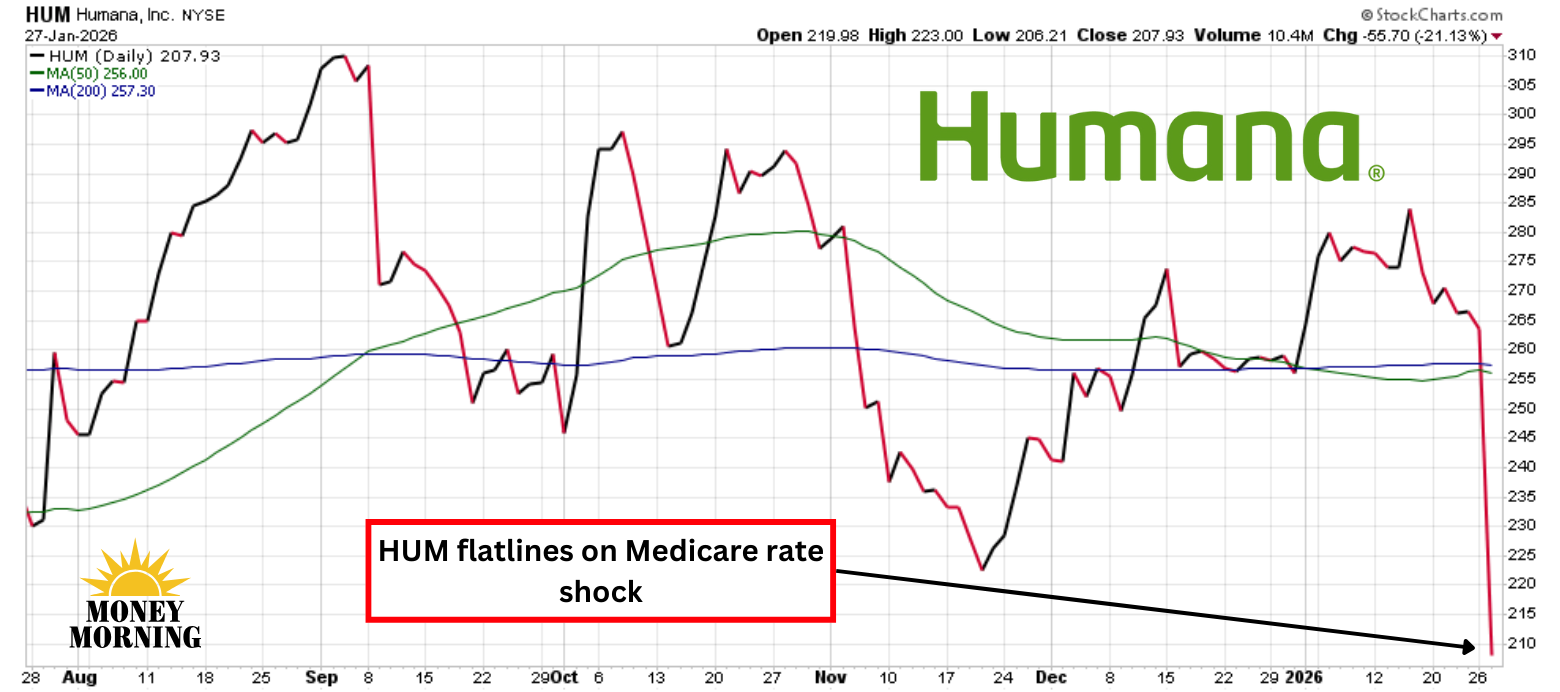

Humana (HUM) investors may have suffered cardiac arrest yesterday after shares of the health insurer cratered 21% to close below $208 – the lowest level since early 2017. This brutal selloff erased billions in market value and helped drag down the entire managed care sector, with rivals like UnitedHealth (UNH) tumbling 19% and CVS Health (CVS) dropping 13%.

The catalyst was a shockingly low proposed payment increase for Medicare Advantage (MA) plans in 2027 from the Centers for Medicare & Medicaid Services (CMS), clocking in at just 0.09% – a far cry from the 5% analysts had penciled in amid rising healthcare costs and utilization. For Humana, which derives about 80% of its revenue from MA, this is devastating, amplifying its ongoing struggles and raising questions about the stock's valuation.

Medicare Rate Proposal Ignites Market Panic

The CMS rate proposal delivered a gut-punch. Analysts had expected a 4% to 6% increase similar to last year to cover inflation, higher drug costs under the Inflation Reduction Act, and surging demand from aging baby boomers.The 0.9% increase – essentially flat after adjustments – could squeeze insurer margins further, forcing premium hikes, benefit cuts, or exiting markets – moves that risk alienating enrollees and stoking regulatory scrutiny.

For Humana, the stakes are sky-high. Unlike diversified peers like UnitedHealth, Humana's heavy MA reliance leaves it acutely vulnerable. The company has already trimmed its MA footprint, exiting plans affecting hundreds of thousands in 2025 and 2026 to combat rising costs. If the rates are finalized in April as proposed, Humana may need to accelerate these efforts, potentially denting 2027 growth.

(Click on image to enlarge)

A Sign of Things to Come

Although Humana's third-quarter results last November saw revenue climbed 11% year-over-year to $32.6 billion – driven by higher per-member premiums in Medicare and state-based contracts, as well as membership growth in stand-alone prescription drug plans (PDP) and Medicaid – profitability took a hit. Adjusted earnings came in at $3.24 per share, down 22%, though it beat Wall Street's estimates. The benefit ratio – a key measure of medical costs as a percentage of premiums – rose to 91.1% from 89.9%, pressured by a shift toward higher-ratio businesses like state-based contracts and PDP, plus changes from the IRA altering Medicare Part D seasonality. Operating costs also edged up, with the ratio hitting 11.8% adjusted.

Looking ahead to Q4 earnings scheduled for Feb. 11, investors aren't expecting much revenues around $30 billion to $32 billion, with adjusted earnings contributing to the full-year $17 per share target. But the new rates could prompt downward revisions to its 2026 outlook, factoring in higher benefit ratios (perhaps 91% to 92%) and slower membership gains due to tweaking benefits. CenterWell's growth in primary care and pharmacy might provide some cushion, but overall sentiment remains cautious.

Bottom Line

Humana's plunge to a nine-year low says "bargain" at first glance, as long-term tailwinds like Medicare enrollment growth (projected to hit 35 million by 2030) and Humana's consumer-focused strategy make it a classic buy-the-dip moment for patient investors.

Yet, the MA rate shock injects too much uncertainty: potential margin erosion, membership churn, and regulatory risks could prolong the pain. With Q4 earnings just two weeks away, the smart play is to wait for greater clarity on 2026 guidance before diving in. If the report reveals deeper wounds, the stock could fall further; if management signals optimism, it just might be time to pounce.

More By This Author:

IREN Soars 15% On Amazon Deal Rumor. Could It Happen?Pinterest Stock Keeps Falling. Is It Too Cheap To Ignore?

Need Another Reason To Buy Micron? Samsung Just Gave You 100 Of Them

Comments

Log in or sign up to join the conversation.