High Dividend 50 - Washington Trust Bancorp

Image Source: Pixabay

High-yield stocks pay out dividends that are significantly more than market average dividends. For example, the S&P 500’s current yield is only ~1.3%, which is quite low on an absolute basis, but also on a historical basis.

High-yield stocks can be very helpful to shore up income after retirement. A $120,000 investment in stocks with an average dividend yield of 5% creates $500 a month in dividends.

Washington Trust Bancorp Inc (WASH) is part of our ‘High Dividend 50’ series, where we cover the 50 highest-yielding stocks in the Sure Analysis Research Database.

Next on our list of high dividend stocks high-dividend stocks to review is Washington Trust Bancorp, which offers a nearly 9% dividend yield at the current price.

This article will evaluate Washington Trust’s potential as a safe source of income.

Business Overview

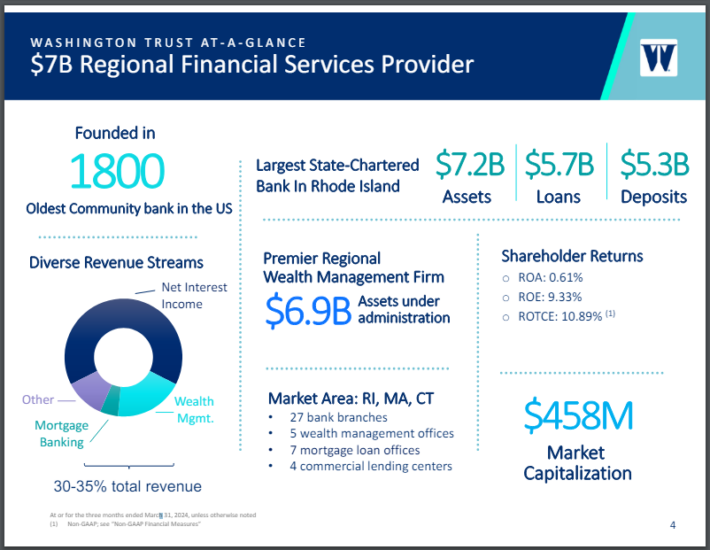

Washington Trust was founded in 1800, making it the oldest community bank in the U.S. The bank is the largest state-charted bank in Rhode Island and has small operations in Massachusetts and Connecticut.

Source: Investor Relations

Washington Trust operates as a holding company, with assets totaling more than $7 billion. The bank provides additional banking services, such as savings accounts, certificates of deposit, and money market accounts to its customers as well.

The bank also offers loans for residential, commercial, consumer, and construction customers, as well as reverse mortgages.

Finally, Washington Trust has nearly $7 billion in assets under management in its wealth management business, where it provides financial planning and advisory services.

Washington Trust has a market capitalization of just ~$437 million, making it one of the smallest financial institutions in our coverage universe.

Washington Trust reported first-quarter earnings results on April 22nd, 2024. Revenue declined 3.3% to $48.82 million for the period, but this was almost $3 million better than expected. Adjusted earnings-per-share of $0.64 was down from $0.74 per share in the prior year but came in $0.19 per share ahead of estimates.

Total loans improved 1% to $5.7 billion from the preceding quarter, while provisions for credit losses were up slightly to $41.9 million. Total deposits continued to decline sequentially, falling 5% from the fourth quarter of 2023 to $4.7. However, deposits were stable year-over-year.

By far the strongest business within the company was Washington Trust’s wealth management division. Revenue improved 5% to $9.3 million as assets under management improved 7% to $6.9 billion. We project that Washington Trust will earn $2.06 per share in 2024.

Growth Prospects

While approximately a third of annual revenue comes from wealth management, mortgage banking, and other sources, the bulk of Washington Trust’s revenue and net income come from the company’s net interest income.

Net interest income and margin largely expanded in the periods following the Federal Reserve increasing interest rates. This worked to the bank’s advantage when interest rates were rising and loan growth remained steady.

That demand has tapered off as rates remain elevated, which costs customers more to secure a loan from the bank. Total mortgage loan originations for Washington Trust fell 25% in the most recent quarter, reflecting a decreasing demand from customers.

Net interest income declined 3% to $31.7 million in the most recent quarter while the net interest margin contracted 4 basis points to 1.84%. The net interest margin was as high as 2.82% as recently as 2022.

Washington Trust’s future growth prospects are also limited by the company’s small scale. The company has less than 30 bank branches in Rhode Island and 1 in Connecticut to go along with several mortgage branches in Massachusetts. This limits the potential client pool to just these areas.

Where Washington Trust does stand out is in its wealth management business, which has a tremendous amount of assets under management relative to its size. This was one of the few bright spots in the bank’s most recent quarterly report and has benefited from rising market conditions.

Washington Trust’s earnings-per-share have a compound annual growth rate of just 1.8% over the last decade. With the company starting from a low base, we believe 5% annual earnings growth is achievable through 2029.

Competitive Advantages & Recession Performance

Given its size, we believe Washington Trust to have no discernable competitive advantages as any service that the bank can offer, the larger names in the industry can as well. Most of the bank’s branches are in Rhode Island, which has just over 1 million people currently living within its borders.

The company’s assets under management do separate it from the average community bank in the sheer size. This has added to revenue results in recent quarters, helping to offset weakness in the net interest income portion of the business.

Like many financial institutions, Washington Trust struggled during the 2007 to 2009 period as the bank experienced a large draw-down in earnings-per-share during the Great Recession:

- 2007 earnings-per-share: $1.75

- 2008 earnings-per-share: $1.57 (10.3% decline)

- 2009 earnings-per-share: $1.00 (36.3% decline)

- 2010 earnings-per-share: $1.49 (49% increase)

While Washington Trust did see a sizeable decrease in earnings-per-share during the period, the company returned to growth the following year and established a new high by 2011.

Washington Trust performed even better during the Covid-19 pandemic as earnings-per-share improved slightly from 2019 to 2020.

The performance of the company during these time periods speaks to its ability overcome difficult economic environments.

Dividend Analysis

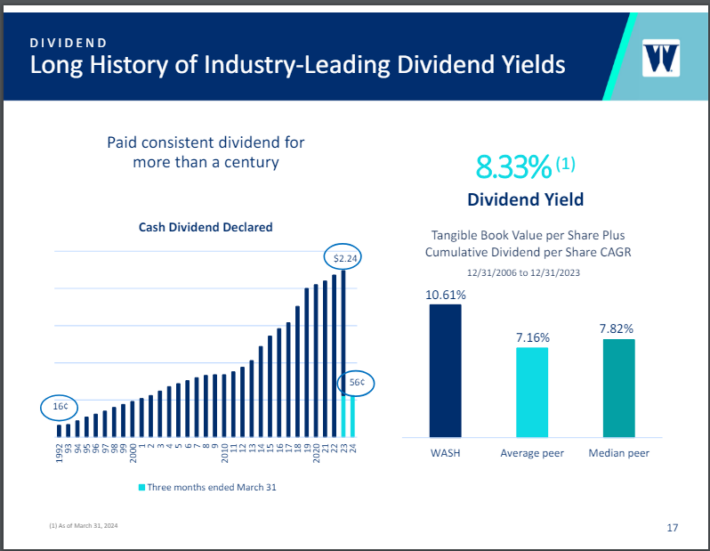

Washington Trust has distributed dividends to shareholders for more than a century.

Source: Investor Relations

When earnings-per-share fell sharply during the Great Recession, Washington Trust paused its dividend growth. Unlike many financial institutions of the time, the bank did not have to cut its dividend.

In 2011, Washington Trust began to raise its dividend, and has now done so for 13 consecutive years. Shares yield 8.7% currently, which is one of the highest yields in the stock’s history.

Very high yields can often serve as a warning sign and this could apply in the case of Washington Trust. The company pays an annualized dividend of $2.24, which equates to a projected payout ratio of 109% for 2024. In most years, Washington Trust’s payout ratio is approximately 50%.

The elevated pay ratio is concerning, as the dividend could be at risk for a cut. Washington Trust has now paid the same quarterly rate of 56 cents for six consecutive quarters.

Final Thoughts

Washington Trust has a dividend yield of almost 9%, which is nearly seven times the average yield of the S&P 500 Index.

While the yield is attractive and certain portions of the business are performing well, like wealth management, we find the extremely high payout ratio to be concerning.

If earnings growth does not return, the dividend could be at risk of being reduced. We urge investors, especially those looking for income, to be cautious with Washington Trust.

More By This Author:

High Dividend 50: First Interstate Bank3 Water Utility Stock For Long Term Dividend Growth

3 Dividend Stocks For Growth At A Reasonable Price

Disclaimer: SureDividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities. However, the publishers of Sure ...

more