High Dividend 50: Vector Group

Vector Group Ltd. (VGR) is a high-yield dividend stock that had to cut its dividend during the COVID-19 pandemic in 2020. Because of the dividend cut, the dividend looks to be fairly safe now.

For the next high-yield stocks in this series, we will review a diversified holding company Vector Group Ltd., which currently has a dividend yield of 7.9%.

Business Overview

Vector Group Ltd. is a diversified holding company headquartered in Miami, Florida, with an executive office in Manhattan and tobacco operations in North Carolina. The company is a combination of a cigarette company and a real estate firm. The company owns and controls two tobacco companies: Liggett Group, LLC and Vector Tobacco, Inc. Vector Group also own New Valley LLC, which is a real estate investment business. The company is also a constituent of the S&P SmallCap 600 Index and the Russell 2000 Index.

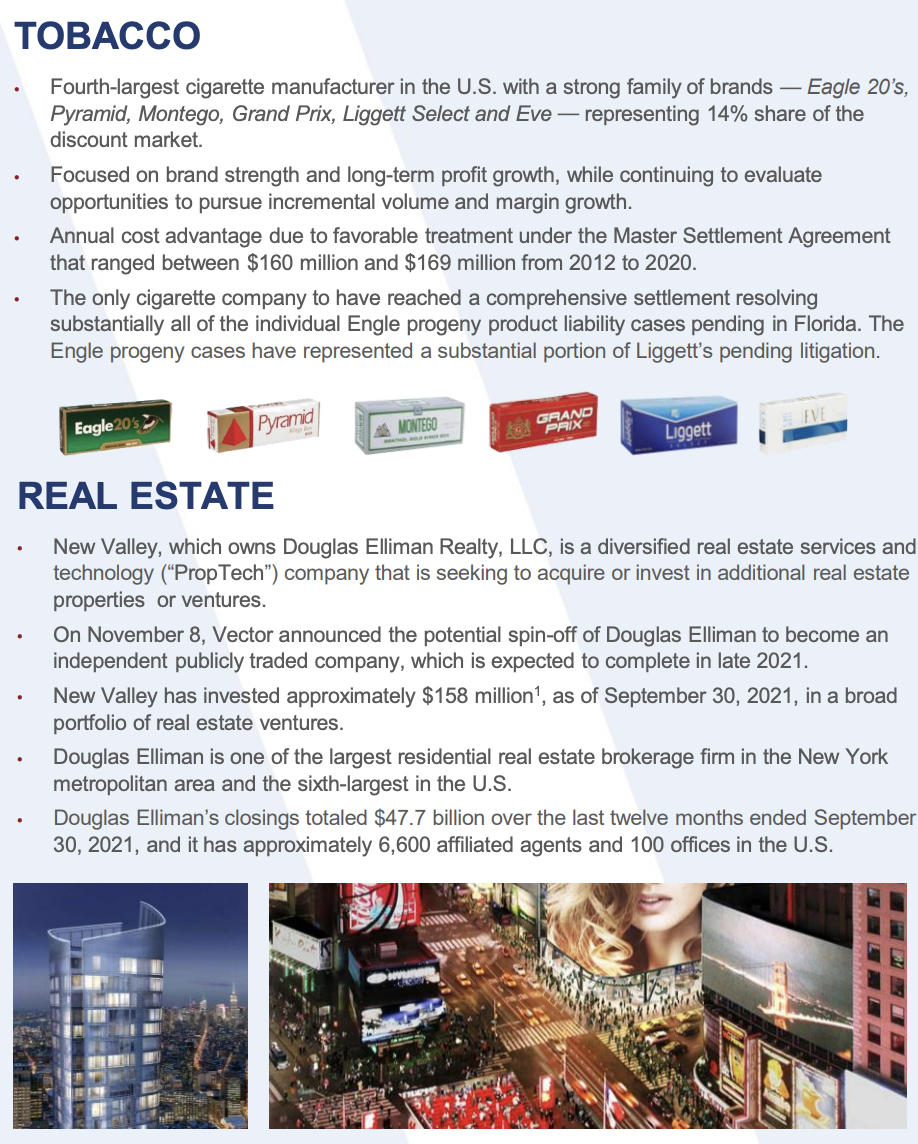

The Tobacco segment primarily sells discount cigarette brands, including Eagle ’20s, Pyramid, Grand Prix, Liggett Select, and Eve. The company is the 4th largest cigarette manufacturer, in terms of volume, in the United States. The real estate segment New Valley has invested approximately $158 million, as of September 30, 2021, in a broad portfolio of real estate ventures.

Source: Investor Presentation

On March 1st, 2022, the company reported fourth-quarter and full-year results for Fiscal Year (FY)2021. For the quarter, the company made $313.7 million, up 9% or $26.5 million compared to the prior-year period. The tobacco segment increased revenue by 7.2% to $306 million compared to 4Q2020 on higher volumes. Wholesale shipments rose to 2.22 billion from 2.12 billion in comparable periods. While the real estate segment, grew revenue 569% versus the prior-year period. Overall, the tobacco segment represents 98% of the company’s total revenue.

Net income for the fourth quarter was $45.3 million, or $0.29 per diluted common share, compared to net income of $32.3 million, or $0.21 per diluted common share, in the fourth quarter of 2020.

For the fiscal year, revenues were $1.22 billion, compared to revenues of $1.23 billion for the 2020 year. The company recorded an operating income of $320.4 million for the year, versus to an operating income of $294.4 million for 2020. Overall, net income was $219.5 million, or $1.40 per diluted common share, compared to net income of $92.9 million, or $0.60 per diluted common share, for 2020.

Adjusted net income from continuing operations was $174.8 million, or $1.12 per diluted share, for the last fiscal year. This compares favorably to $129.9 million, or $0.85 per diluted share, for 2020. This represents an increase of 31.8% year-over-year.

Growth Prospects

Future growth prospects for the company will come from an increase in market share in the tobacco industry. This can be obtained through pricing its products more competitively. For example, VRG holds a significant advantage when compared to larger companies such as Altria (MO) and Philip Morris (PM). VGR to sell cigarettes at a discount due to the Master Settlement Agreement (MSA). Essentially, it gives VGR a $0.80 per pack advantage over the larger companies.

Another growth driver would be a better marking campaign of its brands. This will help bring new customers to its cheaper products.

(Click on image to enlarge)

Source: Investor Presentation

Since the tobacco segment is the company’s biggest source of top and bottom line, acquiring more real estate will help drive growth for the company. As mentioned above, the company has approximately $158 million invested, as of September 30, 2021, in a broad portfolio of real estate ventures. This should help increase revenue and profit.

Competitive Advantages & Recession Performance

Vector Group’s main competitive advantage is the tobacco business, which tends to have stable cash flows. However, e-cigarettes represent a threat and cigarette volumes are declining. Vector Group is also starting to lose market share despite the cost advantage of its discount brands. The New Valley business does not have a competitive advantage. This is why it is important that the company continued to invest in new high-quality real estate properties to grow its portfolio.

As for recession performance, the company did fairly well during the 2008-2009 Great Recession.

LUMN’s earnings-per-share throughout the Great Recession:

- 2007 earnings-per-share of $0.35

- 2008 earnings-per-share of $0.35 (flat)

- 2009 earnings-per-share of $0.31 (11% decrease)

- 2010 earnings-per-share of $0.37 (17% increase)

As you see, the company did reasonably well during the 2008-2009 Great Recession. Also, the dividend was not cut during this period. However, during the COVID-19 pandemic, the company increased earnings from $0.50 per share in 2019 to $0.64 per share in 2020, but the company cut its dividend from $1.09 per share for 2019 to $0.57 per share in 2020. But, because of the recent dividend cut, the current dividend looks much safer compared to period years.

Dividend Analysis

The company pays out a hefty dividend yield of 7.9%. In this section of the article, we will determine if the dividend is safe for dividend and income focus investors. The company has been raising its dividend since 2004 with a dividend growth rate of 5.4% compounded annually until 2020.

In 2020, as mentioned above, the company had to cut its dividend because of the COVID-19 pandemic. They cut the dividend even though earnings were growing from 2018 to 2020. The dividend cut was a 47.7% decrease.

However, with the increase in earnings in recent years and because of the dividend cut, the current dividend looks to be a lot safer compared to a few years ago. For example, in 2019, the company earned $0.64 per share while paying a dividend of $0.57 for the year. This was a payout ratio of89%. This is a high payout ratio. In 2021, the dividend payout ratio was 51%. This provides a much better and safer payout ratio.

We expect the company will make $1.15 per share in 2022 with an earnings growth rate of 3% for the next five years. Thus, this will provide a dividend payout ratio of 49% based on the fiscal year 2022’s expected earnings of $1.15 per share. For that reason, we think that the dividend is fairly safe for the foreseeable future.

In addition, the company has a poor balance sheet, with an interest coverage ratio of 2.9. This is a low level of interest coverage. Also, the company has an S&P credit rating of B+, which is not an investment-grade credit rating.

However, with all the information we have now, we view the dividend of Vector Group as fairly safe for the foreseeable future. Thus, investors should not expect much higher dividend growth and only accept the current high yield.

Final Thoughts

Vector performed well in 2021. The company took advantage of the strong NYC real estate market and announced the spinoff of Douglas Elliman, which is the 6th largest real estate brokerage in the US. Despite a little improvements in the balance sheet, we remain negative for the long-term about Vector due to the cut in the dividend two years ago, high debt, declining cigarette volumes, and pressure on market share.

However, the dividend looks safe and income-driven investors can benefit from the high current dividend yield while they wait for price appreciation.

Disclaimer: Sure Dividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities. However, the publishers of Sure ...

more