Image Source: Pixabay

High-yield stocks pay out dividends that are significantly higher than the market average. For example, the S&P 500’s current yield is only ~1.2%.

High-yield stocks can be particularly beneficial in supplementing income after retirement. A $120,000 investment in stocks with an average dividend yield of 5% creates an average of $500 a month in dividends.

Prospect Capital Corporation (PSEC) is part of our ‘High Dividend 50’ series, which covers the 50 highest-yielding stocks in the Sure Analysis Research Database.

Prospect Capital’s dividend yield is more than 19%, more than six times that of the average S&P 500 Index. Our full list of stocks with 5%+ dividend yields is here.

Prospect’s high dividend yield and monthly dividend payments are two of the reasons why the company merits further research. This article will discuss the investment prospects of Prospect Capital Corporation in detail.

Business Overview

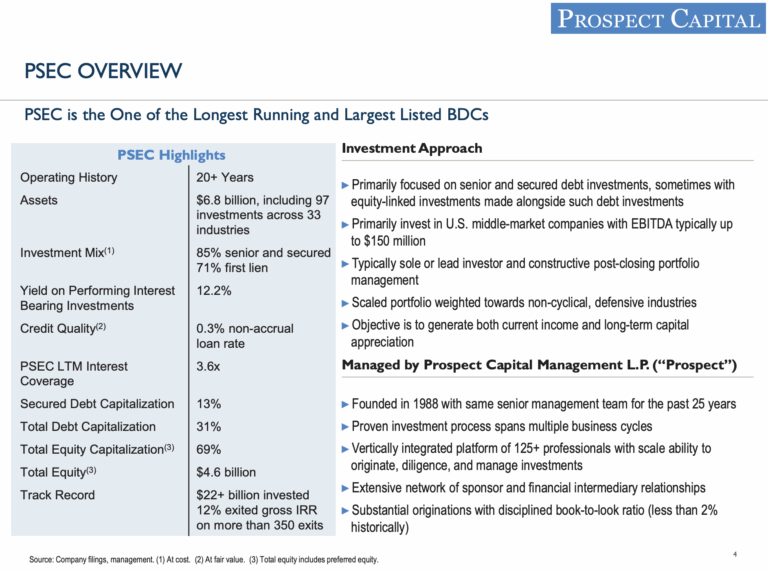

Prospect Capital Corporation is a Business Development Company founded in 2004. It is one of the largest, with a market cap of almost $1.3 billion.

Details about Prospect Capital’s business model are presented below.

Source: Investor Presentation

Prospect Capital is a leading provider of private equity and private debt financing for middle-market companies, broadly defined as a company with between 100 and 2,000 employees.

Prospect Capital benefits from operating in the middle market because it lacks competition from larger, more established lenders.

Middle-market companies are generally too small to be customers of commercial banks but too large to be served by the small business representatives of retail banks. Prospect Capital does business in the “sweet spot” between these two services. This lack of competition in this sector has allowed Prospect Capital to finance some truly attractive deals.

Investors should note that Prospect Capital is highly exposed to interest rate volatility. This is because the company’s liabilities are primarily at fixed rates, while its investments are largely floating-rate instruments. That means interest expense is largely fixed, while interest income fluctuates in proportion to prevailing interest rates.

As interest rates rise, the revenues from Prospects’ floating-rate interest-bearing assets will increase. At the same time, Prospect’s interest expense will remain constant since most of its debt is fixed. Of course, the opposite is true, as falling rates generally mean declining interest income.

This makes Prospect Capital a great portfolio hedge against interest-sensitive securities, such as REITs and utilities; however, it underperforms when interest rates are very low or when rates are declining.

Prospect Capital’s flexible origination mix is also a significant advantage from an investor’s perspective, as the wide variety of instruments it uses to generate income enables it to identify the best opportunities.

The company offers nine different investment options for target companies, including various types of debt and equity. They all have different risk levels and rates of return.

Prospect Capital’s willingness to seek out the best instruments — and having the scale to do so — is a major advantage over other middle-market BDCs. The company’s investment strategy is central to its long-term growth.

Growth Prospects

Prospect Capital’s growth prospects stem largely from the company’s ability to:

- Raise new capital via debt or equity offerings

- Invest this new capital in deal originations with an internal rate of return higher than the cost of capital raised in Step 1

Prospect’s ability to source new deals that offer appropriate risk-adjusted returns is the most important part of this process.

Fortunately for the company (and its investors), there is no shortage of new deals for Prospect’s consideration. The company has thousands of deal opportunities each year, allowing it to be very selective in its investment decision-making.

Prospect Capital Corp. reported a net investment income (NII) of $79.0 million ($0.17 per share) for the quarter ended June 30, 2025, down from $83.5 million ($0.19 per share) in the prior quarter. The company posted a net loss of $226.4 million ($0.50 per share), primarily due to unrealized losses and asset markdowns.

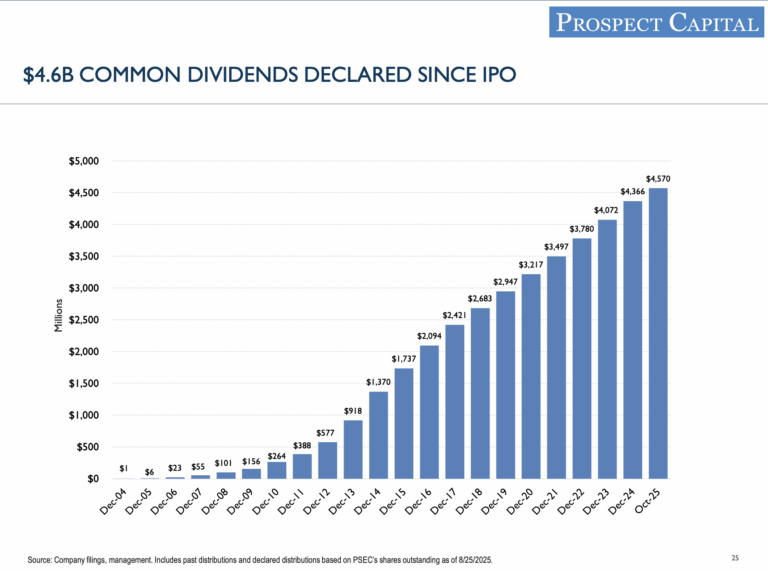

Net asset value (NAV) declined to $6.56 per share, compared to $7.25 in the previous quarter and $8.74 a year earlier, reflecting ongoing portfolio adjustments and fair value changes. Prospect maintained its monthly dividend of $0.045 per share, with declared payments through October 2025, resulting in cumulative distributions of $21.66 per share since inception—over $4.6 billion in total. The firm’s total assets fell slightly to $6.8 billion, and its net debt-to-equity ratio rose modestly to 44.4%, remaining within a conservative leverage range.

Management continued to shift the portfolio toward core first-lien senior secured middle-market loans, which now make up 70.5% of investments (up 642 basis points year-over-year), while reducing exposure to second-lien and structured notes, the latter of which now account for just 0.6% of the portfolio. Prospect also made selective exits from equity-linked assets and real estate, including six property sales over the past six quarters, while its National Property REIT Corp.

(NPRC) The portfolio, focused on multifamily real estate, has generated an impressive 24% unlevered IRR since its inception. Looking ahead, Prospect plans to continue recycling capital into first-lien secured loans with selective equity participation, while maintaining ample liquidity of $1.3 billion and a cost-efficient revolving credit facility. Despite a challenging credit environment, the firm’s diversified funding, strong insider ownership (28.5%), and focus on stable income generation position it to preserve dividends and gradually rebuild NAV over time.

This is the result of higher prevailing interest rates. We continue to see 45 cents in net investment income for this year, but note that 2024 may represent the top for the medium term, given favorable interest rate conditions.

Source: Investor Presentation

Competitive Advantages & Recession Performance

One of the issues with business development companies is that competitive advantages are very difficult to come by, and Prospect is certainly no exception. Scale is the name of the game for BDCs, and with a stagnant balance sheet, Prospect has lost some of its relative scale over time. Prospect’s assets are on the decline once more, producing yet another headwind for earnings and the dividend.

The company’s payout ratio was over 100% for several years in the past decade and is expected to be again in 2026. We believe it may be some time before the payout is covered by earnings again, and we believe the newly reduced dividend may also be at risk in the coming years.

The company performed poorly during the previous major economic downturn, the Great Recession of 2008-2009:

- 2008 earnings-per-share: $1.91

- 2009 earnings-per-share: $1.87

- 2010 earnings-per-share: $2.12

Dividend Analysis

Prospect Capital’s dividend is the obvious reason investors would choose to own the stock; therefore, it is critical that the dividend is as secure as possible. As a BDC, Prospect Capital has no choice but to distribute essentially all of its taxable income to shareholders. Because of this, its payout ratio will always be very high and sometimes variable.

In other words, the dividend is actually covered by net investment income and has been for some time, meaning the payout should be relatively safe, barring a sizable impact from any potential economic downturn.

Source: Investor Presentation

Clearly, the draw for Prospect Capital lies in its ability to generate cash and return it to shareholders, and over time, it has done so effectively.

The dividend appears safe for now, but investors should continuously monitor the company’s net investment income for any signs of trouble that could potentially lead to further cuts down the road. We don’t see that as a threat at the moment, as the company has consistently covered its payout in the past several quarters.

Final Thoughts

Prospect Capital’s high 19%+ dividend yield and monthly distributions are two key reasons an investor might be interested in this stock.

Taking a closer look reveals that this BDC has a high-caliber leadership team and has positioned itself to thrive in most environments.

The dividend appears sustainable for the time being, meaning Prospect is worth a look for investors seeking high levels of current income and monthly payments, while also being willing to stomach the inherent risks of owning a BDC. However, we have a Sell recommendation.

More By This Author:

High Dividend 50: Blue Owl Capital Corporation10 High Dividend Stocks Trading Near 52 Week Lows

3 Wealth-Building Dividend Growth Stocks For The Long Run

Comments

Log in or sign up to join the conversation.