Image Source: Pixabay

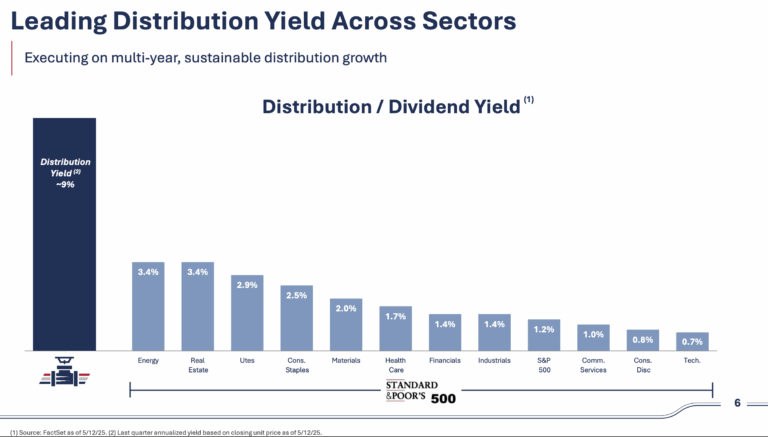

High-yield stocks pay out dividends that are significantly higher than the market average. For example, the S&P 500’s current yield is only ~1.2%.

High-yield stocks can be particularly beneficial in supplementing income after retirement. A $120,000 investment in stocks with an average dividend yield of 5% creates an average of $500 a month in dividends.

Next on our list of high-dividend stocks to review is Plains All American Pipeline, L.P. (PAA).

Business Overview

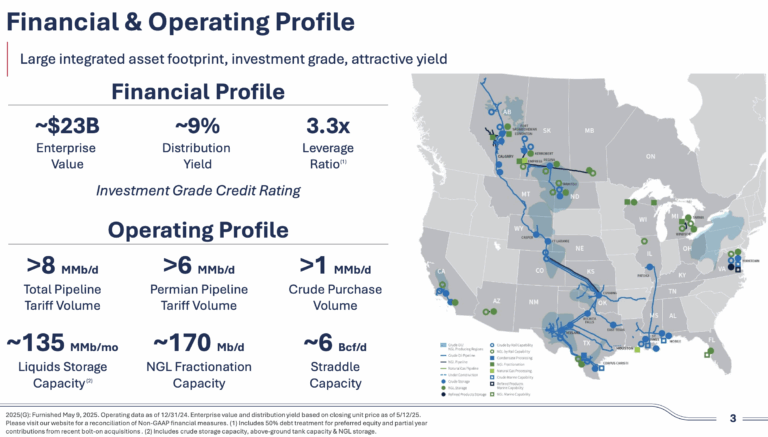

Plains All American Pipeline, L.P. is a leading midstream energy infrastructure company that focuses on transporting, storing, and marketing crude oil and natural gas liquids (NGLs). The company operates one of the largest and most integrated networks of pipeline systems across key producing regions and market hubs in the United States and Canada. Its operations include pipeline transportation, storage facilities, and gathering systems, which play a critical role in efficiently moving energy products from production sites to refineries and end markets.

On average, Plains All American handles over 7 million barrels per day of crude oil and NGLs through approximately 18,370 miles of active pipelines. This extensive infrastructure enables the company to support North America’s energy supply chain while maintaining strong operational reliability and efficiency. By leveraging its scale and strategic assets, Plains All American continues to position itself as a vital link in the midstream sector, providing stable cash flow and long-term value for investors.

The company reported solid second-quarter 2025 results, with earnings per share of $0.36, beating estimates by $0.03, and revenue of $10.64 billion, down 17.7% year over year. Net income was $210 million, and adjusted EBITDA totaled $672 million. The company ended the quarter with a 3.3x leverage ratio, near the low end of its target range, showing continued financial discipline.

During the quarter, Plains agreed to sell most of its natural gas liquids (NGL) business for $5.15 billion CAD ($3.75 billion USD), with closing expected in early 2026. The proceeds will be used for acquisitions, preferred unit repurchases, and common unit buybacks. Plains also increased its ownership in the BridgeTex Pipeline to 40%, further strengthening its Permian Basin presence.

Operationally, crude oil results remained steady year over year, supported by higher volumes and recent acquisitions, while NGL earnings declined due to weaker market spreads. Overall, Plains remains focused on optimizing its crude oil assets, maintaining strong cash flow, and returning value to unitholders.

Source: Investor Relations

Growth Prospects

The company has shown resilience through the energy sector’s volatility over the past decade. After DCFU peaked at $3.74 in 2015, declines in 2016–2017 and the COVID-19 pandemic in 2020 significantly reduced cash flow. The company responded by strengthening its balance sheet, optimizing assets, and controlling costs, which helped DCFU recover and stabilize around $2.49 by 2023–2024. These actions established a more sustainable operational foundation.

Looking forward, PAA is positioned for steady growth, with analysts projecting DCFU to rise about 5% annually through 2030 and distributions to grow 12% over the medium term. Strategic moves, including targeted acquisitions, divestiture of non-core NGL assets, and share buybacks, are expected to enhance cash flow and operational efficiency, supporting long-term value creation for unitholders.

(Click on image to enlarge)

Source: Investor Relations

Competitive Advantages & Recession Performance

Plains All American Pipeline, L.P. (PAA) benefits from a highly integrated and extensive midstream infrastructure network, including over 18,000 miles of pipelines, storage, and gathering assets across key U.S. and Canadian energy hubs. This scale provides operational efficiency, strong market access, and stable fee-based cash flows, giving the company a competitive edge in crude oil and NGL transportation. Strategic investments, such as expanding its Permian Basin footprint through the BridgeTex Pipeline and optimizing core assets, further strengthen its market position.

PAA has also demonstrated resilience during economic downturns and energy market volatility. Historical performance shows that even after sharp declines in distributable cash flow during the 2016–2017 oil slump and the COVID-19 pandemic, the company’s disciplined cost management, asset optimization, and strong balance sheet enabled a swift recovery. This track record highlights PAA’s ability to maintain stability, generate cash flow, and continue distributions to unitholders during recessions or market stress.

The company performed well during the previous major economic downturn, the Great Recession of 2008-2009:

- 2008 earnings-per-share: $1.48

- 2009 earnings-per-share: $1.57

- 2010 earnings-per-share: $1.52

Dividend Analysis

The company’s annual dividend is $1.52 per share. At its recent share price, the stock has a high yield of 8.9%.

Given the company’s 2025 earnings outlook, EPS is expected to be $2.65 per share. As a result, the company is expected to pay out roughly 57% of its EPS to shareholders in dividends.

(Click on image to enlarge)

Source: Investor Relations

Final Thoughts

In recent years, Plains All American has delivered strong returns, reflecting its disciplined operations and strategic asset management. Looking ahead, the company shows potential for continued gains, with an 8.9% yield and possible valuation improvements driving an estimated annual return of 16.2% over the medium term. While these prospects are attractive, we maintain a hold rating due to the relatively short track record of consistent dividend growth.

That said, Plains’ solid infrastructure, resilient cash flow, and focus on capital discipline position it well to capitalize on growth opportunities and navigate market volatility. Investors seeking income combined with moderate growth may find it a compelling option, particularly if the company continues its strategic initiatives and strengthens its dividend consistency over time.

More By This Author:

High Dividend 50: Timbercreek Financial Corp.

High Dividend 50: GeoPark Limited

High Dividend 50: Delek Logistics Partners

Comments

Log in or sign up to join the conversation.