Image Source: Pixabay

Fast-growing AI infrastructure and cloud provider Nebius Group (NBIS) experienced a wild ride last week that underscored the market’s heightened sensitivity to conflicting signals the market is giving off about the sector.

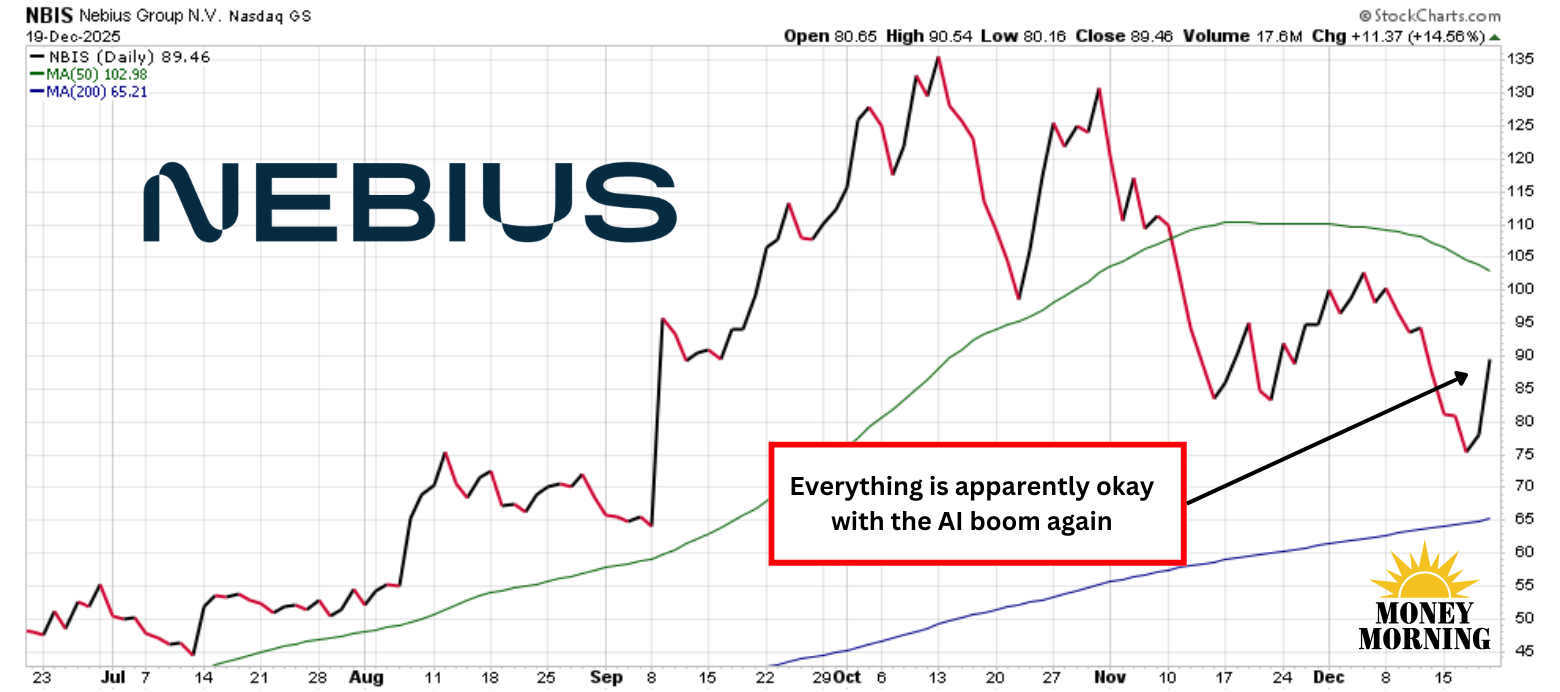

Earlier in the week, growing concerns about AI investment returns, profitability, the capital-intensive nature of AI data-center buildouts, and rising debt levels triggered a broad sell-off in AI-related stocks. Nebius shares plunged as much as 12% in the first two trading sessions as investors feared that its aggressive debt-financed expansion could become unsustainable if AI spending slows. By midweek, the stock appeared headed for a meaningful correction.

Yet, in a sharp reversal, NBIS rallied 14.6% on Friday, finishing the week roughly 2% above its prior Friday close and erasing much of the earlier losses.

Rally Fueled by Renewed Confidence in AI Demand

The catalyst for the comeback was Micron Technology’s (MU) latest quarterly earnings report, which delivered a resounding vote of confidence in AI-driven demand. Micron reported stronger-than-expected results, raised its guidance, and emphasized robust orders for high-bandwidth memory (HBM) used in AI training and inference. The report effectively punctured the narrative that the AI boom might be a bubble, reassuring investors that hyperscalers and enterprise customers remain committed to building out massive compute capacity.

(Click on image to enlarge)

The positive sentiment quickly spilled over to other AI infrastructure names. Analysts also began upgrading Nebius’s peer CoreWeave (CRWV), a high-growth but heavily leveraged player that has been under scrutiny for its rising debt load. Citigroup reiterated its Buy rating on CRWV while trimming its price target from $190 to $135 per share– still implying near double the upside from recent levels. Mizuho, meanwhile, initiated coverage with a $92 per share target, suggesting roughly 35% potential gains. These moves fueled a 23% single-day surge in CRWV shares that helped lift the entire AI cloud subsector.

Nebius is particularly well positioned to benefit. Unlike CoreWeave, which carries significant debt to fund its aggressive expansion, Nebius maintains a much healthier balance sheet. Although long-term debt ballooned to over $4 billion from zero in the third quarter, it has nearly $4.8 billion in cash and equivalents, giving it a negative net debt profile. It also displays a disciplined approach to capital spending.

Recent multiyear contracts with Microsoft (MSFT) and Meta Platforms (META) further bolster its revenue visibility and competitive moat in GPU cloud services.

Bottom Line

Micron’s results largely only confirmed what Nvidia’s (NVDA) earlier blowout quarter had already signaled: AI compute demand remains structurally strong and not yet showing signs of meaningful slowdown.

That said, the debt bomb ticking across the sector hasn’t disappeared. Rising interest rates, execution risks in data-center construction, and the possibility that enterprise AI projects fail to deliver expected ROI could still pressure valuations. Nebius, with its cleaner financial profile, is better insulated than many peers, but its elevated multiples leave little room for disappointment.

That is not enough to issue a clear sell order given the long-term AI tailwinds, but aggressive buying at current levels also carries meaningful risk in a market that remains prone to sharp sentiment shifts. Investors would do well to be more cautious and not rush into the AI hype storm again.

More By This Author:

Intuitive Machines Stock Heads To The Moon. Time To Hop Aboard?Can SoFi Technologies Really Become A $1 Trillion Stock?

President Trump Signs Cannabis Executive Order: Canopy Growth Collapses

Comments

Log in or sign up to join the conversation.