Growth Trap: Why Is Earnings Growth Not Always A Good Thing?

Public companies are enthusiastic about reporting high EPS growth. That is what the market usually cheers about, pushing stock prices higher as we often see post earning reports. Several studies show that reporting companies could see their shares move on average as much as four times the normal daily average. Theoretically, shortsighted Mr. Market is right since EPS increase/decrease should lead to the ups and downs of the stock price given that P/E ratio would stay the same. However, those long-term-thinking quality-focused investors may want to think twice.

What is really missing in the P/E and EPS is the matter of how much capital would be needed to generate the earning. Many investors should be familiar with the concept around return on capital, such as return on equity, which is one of Warren Buffett's favorite metrics. The higher the return on equity, the lower the equity capital needed to generate the same amount of earnings to owners.

Apparently, investors are looking for a high return on capital. But how high is enough? This is all about opportunity cost for the shareholder (i.e., the required rate of return or cost of capital). For example, an investor who has the investment opportunity to generate 10% somewhere else would be happy to see the company s/he invests in has continuous growth with a 30% return on equity and no dividend payment. On the contrary, the same investor would hope for no growth at all and simply get the dividend payment if the company could only deliver 3% ROE. Think of it this way: how is reinvesting at a government bond type of return any better than just paying her/him a dividend for better opportunities somewhere else?

The Importance of ROIC

High growth with low ROE means costing a large amount of equity capital to expand businesses and it is usually done at the expense of shareholder value.

In my view, companies with an ROE below 10% (or ROIC below 5%) should always pay out all its earnings back to shareholders as dividends. Only those companies with 20%+ ROE (or 15%+ ROIC) should solely worry about generating more growth.

I also cover the importance of ROIC in this article, and below are a couple of picks with both high returns on capital and growth potentials.

Domino's Pizza (DPZ)

Delivering more than 2 million pizzas a day worldwide, Domino's is the recognized world leader in pizza delivery operating a network of 15,000 company-owned and franchise-owned stores in more than 85 countries around the world. The company runs on negative equity capital (i.e., total liability > total asset). Therefore, we check return on assets over the past 10 years (see below) and it has been consistently over 10% and rising.

Source: Morningstar; data as of 7/9/2018.

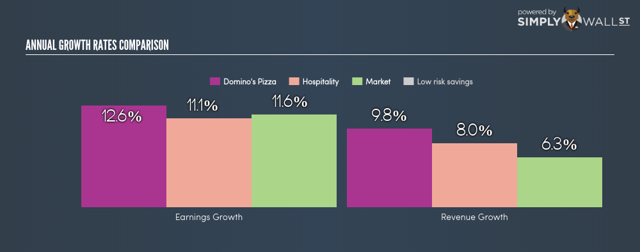

The business is expected to grow its earnings by 12.6% moving forward according to Simply Wall Street (see below), 16% per Morningstar, and 23.1% per FinViz.

Source: SimplyWallSt; data as of 7/9/2018.

Tencent Holdings (TCEHY) (TCTZF)

Tencent is most famous for its mobile-first social network app, WeChat, which dominates the mobile internet market in China. The company has maintained its ROE consistently above 30% and ROIC above 15% for the past decade (see below).

Source: Morningstar; data as of 7/9/2018.

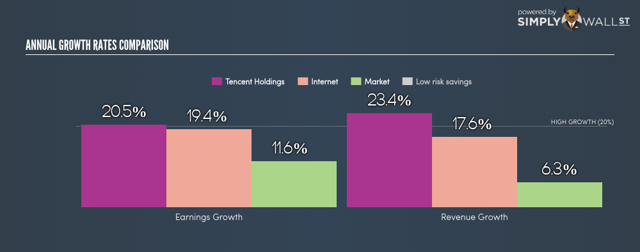

Moving forward, Tencent is expected to grow its earnings by 20.5% according to Simply Wall Street (see below), and 23% per Morningstar.

Source: SimplyWallSt; data as of 7/9/2018.

Hargreaves Lansdown (HRGLY) (HRGLF)

Founded in 1981 by its two founders who had initially traded from a bedroom, Hargreaves Lansdown now claims to be the UK's No. 1 investment platform for private investors. The management has done an excellent job delivering astonishingly high ROIC/ROE (60%+) for its owners over the past 10 years (see below)

Source: Morningstar; data as of 7/9/2018.

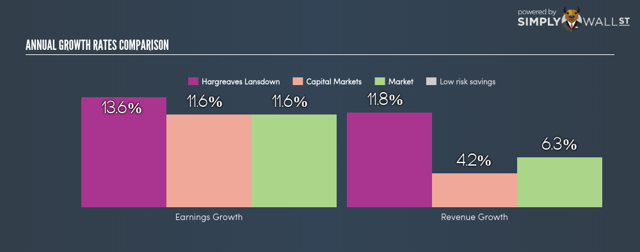

The business is expected to grow its earnings by 13.6% moving forward according to Simply Wall Street (see below).

Source: SimplyWallSt; data as of 7/9/2018.

Evolution Gaming Group (EVVTY)

Evolution Gaming is a leading B2B provider of Live Casino systems in Europe, with a vision to be the global leader in the space. The business has earned extraordinary returns on capital (see below) every year since it went public.

Source: Morningstar; data as of 7/9/2018.

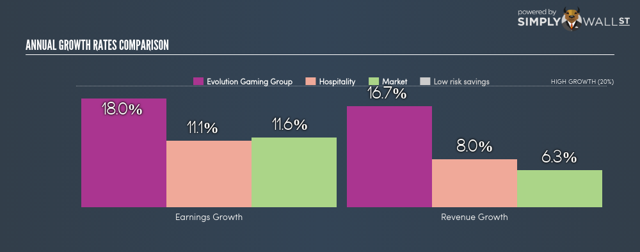

Moving forward, Evolution Gaming is expected to grow its earnings by 18% according to Simply Wall Street (see below).

Source: SimplyWallSt; data as of 7/9/2018.

Summary

Under what circumstances does growth add value for shareholders? The answer hangs on whether future returns on capital exceed or fall short of the cost of capital. For example, if ROE is expected to exceed the cost of equity capital, the more growth the better. But if the management cannot improve profitability and capital efficiency, companies in such a position should consider a policy of rapid negative growth or divestiture to avoid shareholder value destructions.

In short, return on capital is the key. If you’ve got it, flaunt it. If you haven’t got it, try to get it. If you can’t get it, get out.