Goldman Sachs: 4 Stock Picks Set To Soar 20%+

Goldman Sachs has just carried out a survey of 2,000 consumers. The survey revealed that consumer optimism is at record highs- while pessimism is at record lows. This is since the survey started back in 2005.

“The impact of strong demand drivers and strong consumer sentiment is evident in consumer spending,” writes Goldman’s consumer analyst Matthew Fassler. He adds, “We remain confident in the trajectory of the consumer recovery, as drivers of spending remain solid. We note signs of moderating momentum from May through July, and soft patches in housing, but remain constructive on the outlook for discretionary.”

As a result, the firm highlighted several consumer stocks on its elite Conviction Buy list.

Wyndham Hotels & Resorts – GS upside potential of 44%

With over 8,000 hotels to its name, Wyndham Hotels (NYSE: WH) is the largest hotel franchisor in the world.

Note that Goldman’s Stephen Grambling added WH to the firm’s Conviction List in June. This came with a Street-high $82 price target. Wyndham is well-positioned to reap the benefits of revenue-per-available-room out-performance, a momentum that he expects will continue into next year.

And as we can see WH has received only buy ratings in the last three months. This includes a recent bullish rating from top Oppenheimer analyst Ian Zaffino (Profile & Recommendations).

Following strong Q2 results, Zaffino concludes that Wyndham offers “robust growth, substantial free cash flow, an experienced and dedicated management team.” Plus he believes the $1.95 billion acquisition of La Quinta will make it the leader in the mid-scale segment. However, the analyst is sticking with a slightly more cautious price target of $69 (22% upside potential).

(Click on image to enlarge)

View WH Price Target & Analyst Rating Details

Aramark Holdings – GS upside potential of 38%

If you haven’t heard of Aramark (NYSE: ARMK) before, listen up! This is the company behind the food, facilities and uniform services of organizations around the world. Customers span everything from hospitals to schools.

Nomura’s Dan Dolev (Profile & Recommendations) has just reiterated his Buy rating and $48 price target. He made the move following solid earnings results. “Increasing FY revenue growth expectation in the legacy business from “at least 3%” to +3.5% is a key positive” states Dolev. Plus, “seeing overall organic growth accelerate from +2.30% to +3.95% is surely encouraging.”

(Click on image to enlarge)

View ARMK Price Target & Analyst Rating Details

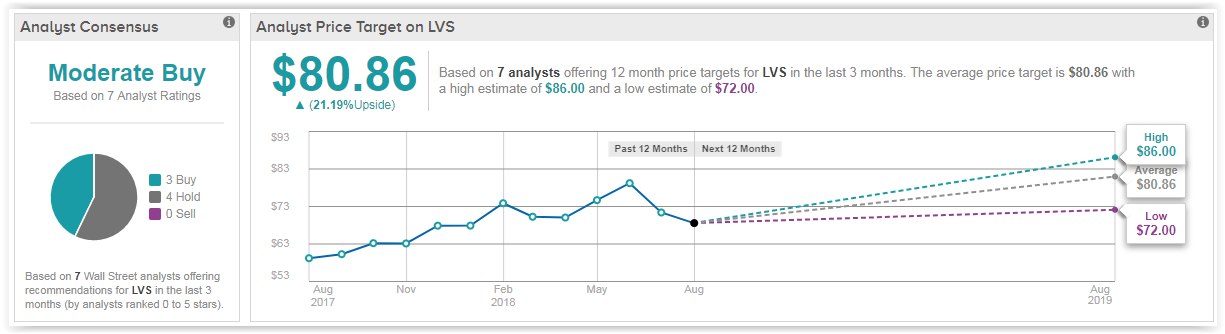

Las Vegas Sands – GS upside potential of 31%

Nevada-based Las Vegas Sands (NYSE: LVS) is the biggest casino owner in the US. Among its US casinos in the United States are two resorts on the Las Vegas Strip: The Venetian and The Palazzo. However, the company also owns a multitude of other properties including in Macau- known as the ‘Las Vegas of Asia’.

Goldman Sachs is positive on the company’s positioning in Macau, Singapore and Las Vegas. In particular, Senior VP, Daniel Briggs called out the Mass market in Macau showing notable strength with LVS positioning itself to take share.

Top Deutsche Bank analyst Carlo Santarelli (Profile & Recommendations) has a Hold rating on the stock. Growth remains impressive concedes Santarelli, but he wonders whether shares will fall victim to outperformance and high expectations. Interestingly, however, his $75 price target still suggests 12% upside potential.

(Click on image to enlarge)

View LVS Price Target & Analyst Rating Details

Mondelez International – GS upside potential of 23%

Sweet snack giant, Mondelez International, Inc. (Nasdaq: MDLZ) owns all the best billion-dollar brands from Ritz and Oreo to Toblerone and Cadbury.

“We forecast 2018 to be a year of steady topline improvement and double-digit total returns” cheers RBC Capital’s David Palmer (Profile & Recommendations). This five-star analyst has a $51 price target on the stock (22% upside potential).

He points out that Mondelez has a leadership position in a global snacking category that is growing 3-4%, yet is trading in line with large cap food peers with inferior category exposure.

Plus the longer-term outlook is promising. He concludes: “Change has been the norm for Mondelez—and so has outperformance. Among big-cap food companies, Mondelez may have the best chance to achieve solid long-term revenue and profit growth without M&A.”

(Click on image to enlarge)

Disclaimer: TipRanks is an independent cloud based service that measures and ranks digitally published financial advice. TipRanks' natural language processing (NLP) algorithms aggregate and ...

more