Bank stocks are getting slaughtered on the heels of Silicon Valley Bank’s failure.

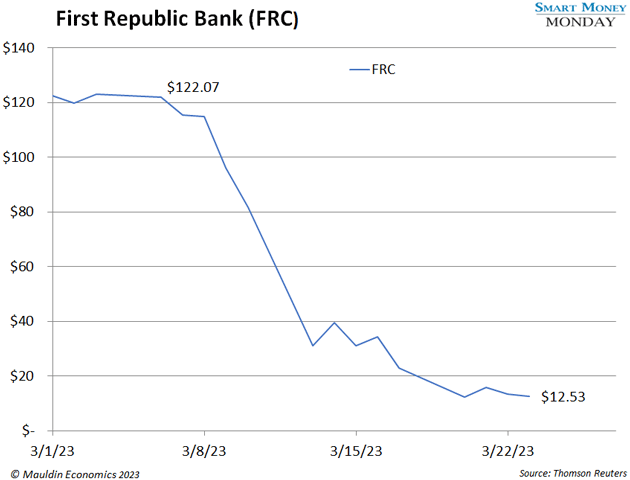

Look no further than First Republic Bank (FRC), which is down 90% since March 6, the week Silicon Valley Bank collapsed:

The banking crisis has ignited the investing world, and bargain-hunting friends of mine have been asking: “Should I buy the First Republic?”

After all, First Republic is prestigious. Facebook founder Mark Zuckerberg got a mortgage there. Dozens of customer surveys rate its satisfaction scores higher than super-brands like Apple and Ritz-Carlton.

If First Republic is truly a high-quality asset that’s 90% on sale… we should be rushing to buy.

Comparing FRC to SVB

At the 2006 Berkshire Hathaway annual meeting, super investor Warren Buffett talked about how he and partner Charlie Munger look at investment opportunities:

“We’ve got three boxes at the company: in, out, and too hard.”

I’ve looked up and down First Republic’s capital structure. It even has some preferred stock that could be a “safer” way to play it.

But First Republic’s issues mirror the ones faced by Silicon Valley Bank…

It has a number of long-duration loans on its books. These are predominantly residential mortgages. The mortgages are fixed at around 3% and likely extend out over a decade.

Like I wrote last week, a 3% loan—were it to be sold—would be worth considerably less than 100 cents on the dollar in a 5% interest rate world.

When you adjust First Republic’s balance sheet to “fair value,” it turns out that total equity in the bank was negative $10 billion as of the end of 2022. That’s not good.

On top of that, First Republic was heavily funded with customer deposits. Customers were happy to use the bank for their deposits, just like they were with Silicon Valley Bank… until they weren’t.

As of the end of 2022, First Republic reported $119 billion in uninsured deposits. This pencils out to two-thirds of its $176 billion in deposits. That’s a big number.

Depositors ran the numbers and, en masse, pulled their money out in fear that they’d lose their money above and beyond the insurance limits.

First Republic, just like Silicon Valley Bank, had a massive bank run.

Big banks like JP Morgan have injected $30 billion in cash in the form of deposits in an attempt to calm the markets and keep the bank solvent.

But it’s probably too little too late.

Toss FRC into the Too-Hard Pile

Right now, too many things need to go right for me to seriously consider FRC. That’s a telltale sign of a “too-hard” investment.

Going forward, nearly everyone will connect “First Republic” with “bank run.” I believe the brand is permanently impaired. And that means investors will choose to put their money into better opportunities.

Deposit flight (all depositors pulling their money out of a bank) is a continued risk with the First Republic, and no bank stock is cheap enough to factor in major deposit flight risk and brand destruction.

In short, avoid stocks in the too-hard pile such as FRC.

You’re better off sticking with simple, easy-to-follow stories when hunting for bargain-priced stocks.

More By This Author:

Silicon Valley Bank’s Collapse Offers A Crucial Reminder

VST: A Transformational Acquisition for This Proven Utilities Winner

The Truth Behind The CO2 Crisis… And The Smart Way To Play It

Comments

Log in or sign up to join the conversation.