Fed Chairman Jerome Powell Does Not Rule Out Interest Rate Hikes At Every FOMC Meeting

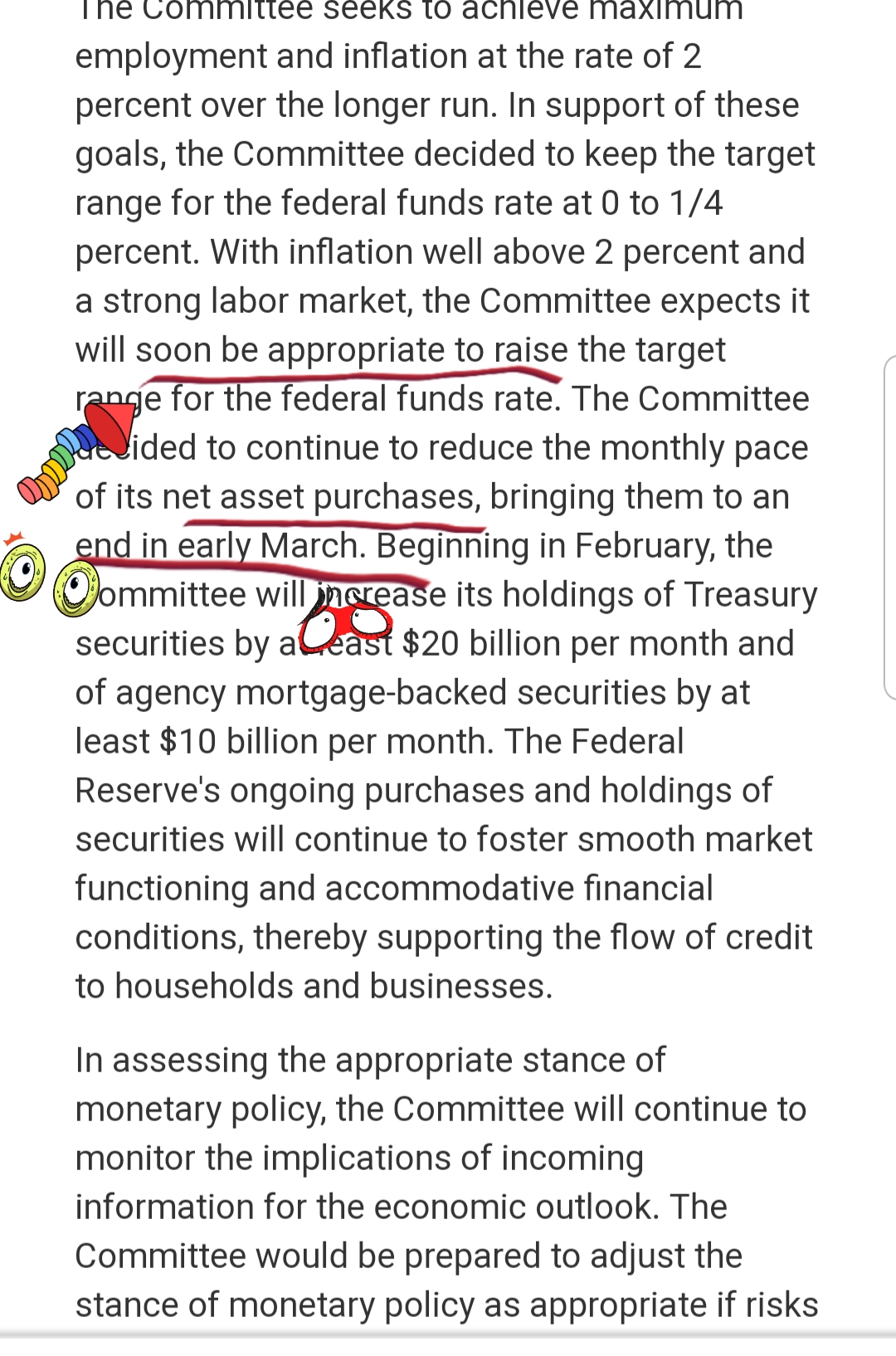

Yesterday, investors were focused on the Fed's interest rate decision and the speech by Fed Chairman Jerome Powell. The Federal Reserve kept the interest rate at 0.25%. The end of the QE program will occur in March, and the balance sheet reduction will not begin until after the start of the rate hike. If risks arise that prevent it from achieving its goals, the Fed is prepared to change its monetary policy stance as necessary. The Fed's decision coincided with the forecasts of economists and market participants.

Key talking points from Jerome Powell's speech:

- The economy no longer needs sustained high levels of support;

- The Fed does not rule out a rate hike at every FOMC meeting;

- The Fed may adjust policy if risks rise;

- Fiscal policy will be less conducive to growth this year;

- The fiscal stimulus for growth will be significantly reduced, which will also contribute to lower inflation;

- We have not made decisions on the timing or pace of balance sheet cuts. We will provide additional information on balance sheet cuts when the time comes;

- Factors in higher inflation are related to the epidemic;

- We expect inflation to decline during the year;

- Supply problems are more severe and longer-lasting than previously thought;

- There is widespread improvement in the labor market;

- Wages are rising at the fastest rate in many years;

- Pandemic supply and demand imbalances continue to contribute to high inflation.

The US stock market traded mixed yesterday. After Jerome Powell's speech, the markets began to lose the upward momentum which was formed during the day. At the close of the day, the Dow Jones (US30) decreased by 0.38%, the S&P 500 (US500) decreased by 0.15%, and the Nasdaq (US100) tech index added 0.02%.

On Wednesday, Tesla released its fourth-quarter results, which beat analysts' expectations. Tesla stock jumped by 1.08% yesterday. But Tesla's stock price lost 11% this year.

European stock indices ended the trading day in the green zone, recovering from a collapse earlier in the week. The German DAX (DE30) gained 2%, the French CAC 40 (FR40) jumped by 2%, the Spanish IBEX 35 (ES35) added 1.7%, and the British FTSE 100 (UK100) increased by 1.3%. The focus of market participants is still on the ongoing corporate reporting season for the fourth quarter of 2021. Deutsche Bank's 2021 net income quadrupled to 2.51 billion euros, the highest since 2011. Shares of Hungarian low-cost carrier Wizz Air decreased by 0.2% after the report. The company reported a rise in its October-December loss to €266.1 million from €115.9 million in the same period a year earlier and warned of a possible increase in losses in the current quarter. Deutsche Lufthansa AG's share price rose 5.2% on the report, and the company is among the leaders in the Stoxx Europe 600 index.

Despite a rise in stocks last week, oil rose on Wednesday, surpassing the $90 a barrel mark for the first time in seven years. This was caused by tight supply and rising political tensions between Russia and Ukraine, which increased fears of further disruptions in an already tight market. Brent crude jumped by 2% to $89.96 a barrel, surpassing the $90 mark for the first time since October 2014. The US West Texas Intermediate (WTI) crude also rose 2% to $87.35 a barrel.

There are sales in Asian markets. Japan's Nikkei 225 (JP225) lost 3.11% since opening, Hong Kong's Hang Seng (HK50) decreased by 2.55%, and Australia's ASX 200 lost 1.77%. Chinese IT stocks were among the drop leaders in the Hang Seng index: Alibaba Group Holding Ltd. fell by 6.1%, Netease Inc. dropped by 4.5%, and JD.com Inc. shares fell by 4.3%. Samsung Electronics' 2021 net income rose 1.5 times to $32.7 billion, and revenue rose 18% in the period. But despite the good report, the company's shares fell by 2.2%. Electronics and battery maker LG Corp. lost 3.5%. Shares of automaker Kia Corp. gained 1% on the report, while Hyundai Motor Co. shares fell by 1.6%.

Main market quotes:

- S&P 500 (F) (US500) 4,349.93 −6.52 (−0.15%)

- Dow Jones (US30) 34,168.09 −129.64 (−0.38%)

- DAX (DE40) 15,459.39 +335.52 (+2.22%)

- FTSE 100 (UK100) 7,469.78 +98.32 (+1.33%)

- USD Index 96.48 +0.54 (+0.56%)

Important events for today:

- US Core Durable Goods Orders (m/m) at 15:30 (GMT+2);

- US GDP (q/q) at 15:30 (GMT+2);

- US Initial Jobless Claims (w/w) at 15:30 (GMT+2);

- US Pending Home Sales (m/m) at 17:00 (GMT+2);

- US Natural Gas Storage (w/w) at 17:30 (GMT+2).

Disclosure: This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, ...

more

$QQQ $AMD $SPY $AMZN