The market continued its strong performance in July as receding inflation reports and solid economic performance increased optimism for an attractive scenario where the Federal Reserve will not need to continue raising rates, inflation will be manageable, and the economy will continue growing. This is by no means certain and surprises happen all the time, but so far the data looks good.

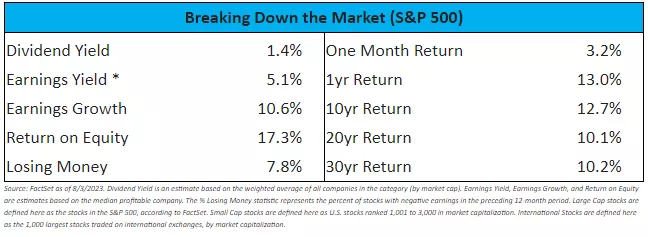

Despite the recent optimism, I think it is appropriate to be somewhat cautious, minimize debt, and maintain adequate safety reserves. But I am still seeing plenty of good quality companies trading at 5-7% earnings yields and offering expected earnings growth of around 7-10% a year. At those earnings yields and growth rates, I am happy to invest for the long-term.

* “Earnings yield” is an investor’s share of earnings for every dollar invested (i.e., earnings per share / price per share). It’s the same as the more famous Price / Earnings (P/E) ratio, but expressed as a yield rather than as a multiple. I use it to compare stocks more clearly with bonds and other asset classes.“Equity Risk Premium” equals the Earnings Yield minus the 10-year Treasury Inflation Protected Securities yield.

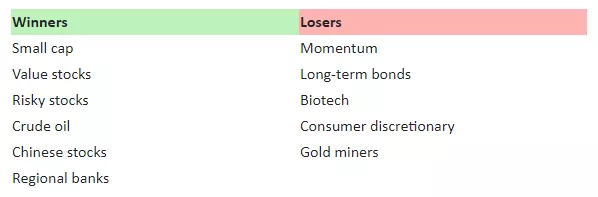

Last Month’s Winners and Losers

The market continued its positive run in July, with particularly strong results at regional banks, small cap stocks, and risky stocks in general. Long-term bonds were weak and what worked earlier in the year did not work well in July (i.e., there was a reversal in momentum).

Income: Inflation Cooling?

Core inflation for each of the last two months came in within the 2-3% annualized rate. While this is not yet a trend, it is a positive sign. The Federal Reserve raised rates again, which seems more like an insurance policy to keep pressing inflation down. Given the lags as rate hikes flow through the economy and the stress that higher rates have placed on the banking system, I think continued rate rises would be unwise. That said, the Federal Reserve has its own processes and tends to be focused on lagging data, so it’s unclear what they will do.

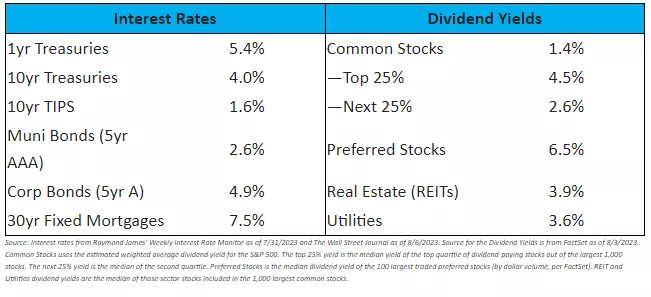

Long-term rates imply around 2.4% inflation over the next 10 years*. Although I believe this is optimistic, it is plausible given the recent data. However, I believe there is more risk to investors if inflation were to come in higher than if inflation were to come in lower. For this reason, I believe investors are better served by sticking with short-term instruments for the fixed income portion of their portfolio.

* Implied inflation expectations are derived from taking the 10-Year Treasury rate and subtracting the 10-Year Treasury Inflation Protected Securities (TIPS) rate. For example, if the yield on 10-year treasuries is 2.8% and the yield on 10-year TIPS is 0.4%, they are roughly equivalent investments if inflation comes in at the difference (2.8% - 0.4% = 2.4%).

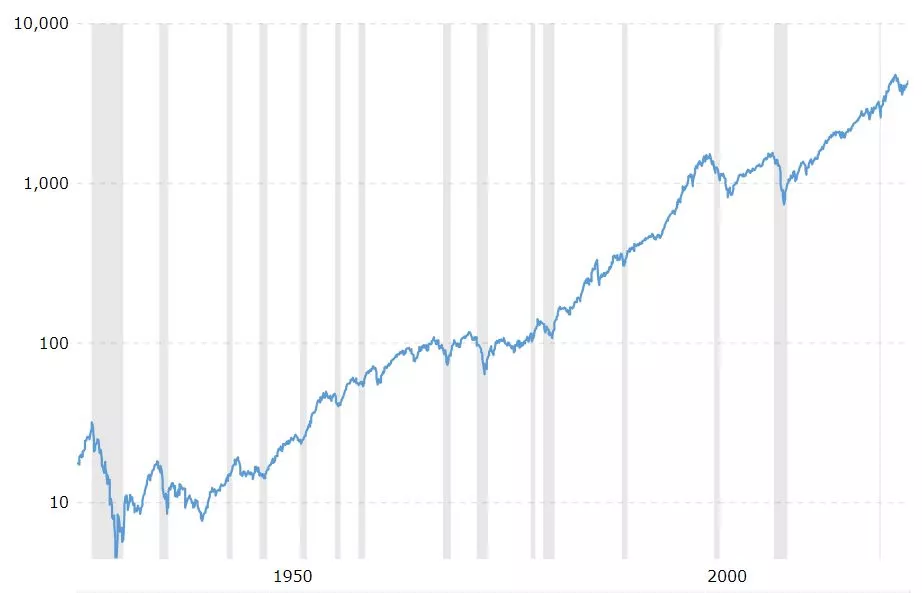

The Long View

Source: MacroTrends.net

For the last 20, 30, and 100 years, stocks have averaged around an 8-10% return, driven by dividend yield, reinvestment of earnings, and earnings growth. Long-term bonds have yielded about 5% on average over the last century while inflation has been about 3%.

Throughout this period, there have been major upheavals, such as the Great Depression, World War II, The Korean War, The Vietnam War, dropping the gold standard, 1970s high inflation, 1987’s Black Monday Crash, the Dot.com bust, the 9/11 terror attacks, the Global Financial Crisis, and the Covid Crash, among others.

These events led to severe market downturns about once every decade, with a median price decline of 33% and a median time to recover back to the previous high of 3.5 years. If we were to include dividends, the recovery to previous highs is actually a little faster. *

Meanwhile, a 3% inflation rate results in a 59% decline in the value of a dollar over 30 years. Meaning that people who retire at 60 years old on a fixed income face a high risk of a lower quality of life as they get further into retirement. *

* Source: Morningstar Direct via cfainstitute.org, FactSet. Past performance is not necessarily indicative of future performance. Depreciation of the dollar: $1 / (1 + 3%)^30 = $0.41 real value 30 years later.

Market Outlook

Now I’ll put on my “Nostradamus Hat” and make some predictions, for whatever they’re worth:

- Inflation will average 2-4% over the next 10 years.

- Interest rates will fall in the 3-5% range for 10yr Treasuries over the next several years, in line with inflation and historical experience.

- The economy will grow 2-3% in real terms over the next several years, though we will probably slip into a recession this year.

- Stocks will average an 8-10% return over the next 10+ years. After subtracting inflation, this will translate into about a 5% real return. There is likely to be at least one big decline every decade or so.

From the standpoint of where you and your family will be in 30 years, none of this matters. What matters is finding good quality investments that are likely to grow over the decades. For this reason, I largely ignore my own general market forecast and invest whenever I find a business that I am confident in and that trades at an attractive valuation.

Comments

Log in or sign up to join the conversation.