Dollar General Corp.(DG) shares plummeted in the New York premarket trading following a weaker-than-expected second-quarter earnings report. The discount retailer faces its first annual decline and has lowered its profit forecast for the second quarter in a row amid "softer sales trends." Troubles at Dollar General mirrors challenges faced by other retail businesses, pointing to the potential cracking of low/mid-tier consumers.

(Click on image to enlarge)

Source: ZeroHedge

The discount retailer posted earnings of $2.13 a share on revenue of $9.8 billion. Analysts surveyed by FactSet forecasted $2.47 a share on sales of $9.9 billion. Same-store sales declined .1%, while analysts were expecting a .9% rise, driven by a slowdown in consumer traffic.

Dollar General's second-quarter highlights:

- Comparable sales -0.1% vs. +4.6% y/y, estimate +0.92%

- EPS $2.13 vs. $2.98 y/y

- 2-year same-store sales stack +4.5% vs. -0.32% y/y, estimate +5.37%

- Net sales $9.80 billion, +3.9% y/y, estimate $9.91 billion

- Gross margin 31.1% vs. 32.3% y/y, estimate 31.7%

- SG&A as a percentage of revenue 24% vs. 22.6% y/y, estimate 23.5%

- Operating profit $692.3 million, -24% y/y, estimate $785.1 million

"This gross profit rate decrease was primarily attributable to lower inventory markups and increased shrink, markdowns, and inventory damages, as well as a greater proportion of sales coming from the consumables category, which generally has a lower gross profit rate than other product categories," Dollar General said.

CEO Jeff Owen wrote, "While we are not satisfied with our overall financial results, we made significant progress in the second quarter improving execution in our supply chain and our stores, as well as reducing our inventory growth rate and further strengthening our price position."

The retailer slashed its fiscal 2023 outlook as it takes "certain actions to accelerate the pace of its inventory reduction efforts and making additional investments in targeted areas, such as retail labor, to further elevate the in-store experience and better serve its customers." It noted, "softer sales trends and an increase in expected inventory shrink for the second half of 2023" are some of the reasons for revising its outlook for fiscal year 2023 that was last provided on June 1 (read: here).

Shares crashed as much as 16% in the premarket session.

(Click on image to enlarge)

What's alarming about the "softer sales trends" comment from the retailer is that 40% of its customer base earns less than $40,000 a year. This clearly indicates that no matter how much the White House tries to spin the 'best economy ever ' -- 'Bidenomics' is failing the working poor.

Sales headwinds are being reported at many US retailers. We outlined this in a note titled Do Plunging Retail Stocks Signal The US Consumer Is Finally Done. Our short answer: most likely.

With Covid helicopter cash evaporated, personal savings drained, insurmountable credit card debt, and the lack of financial safety nets, the average consumer in the Biden era has been crushed after two years of negative real wages.

Just wait until student debt repayments begin come October... CEOs are already panicking (read: Corporate America Panics As 'Student Loan' Chatter Hits Record On Earnings Calls).

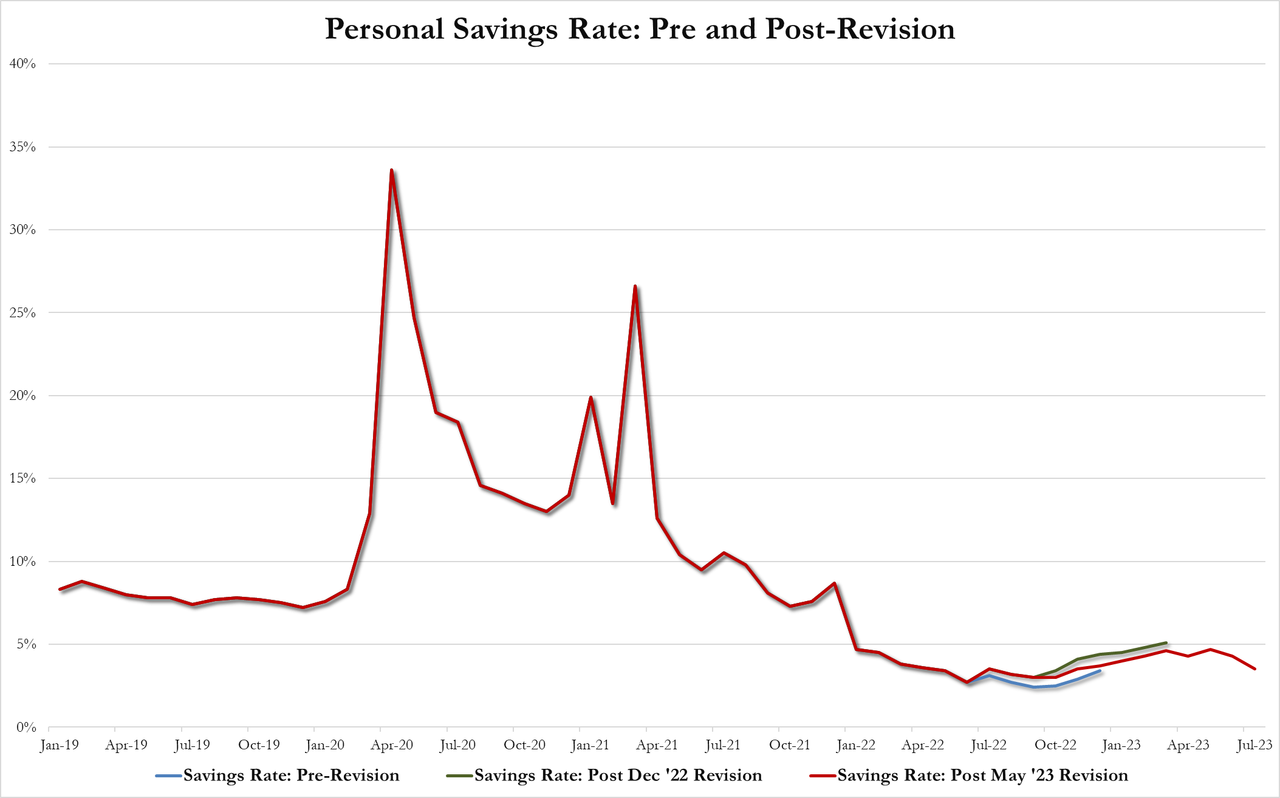

None of this should be a surprise after this morning's plunge in the savings rate...

(Click on image to enlarge)

The emergence of a consumer spending cliff has arrived.

More By This Author:

US Pending Home Sales Unexpectedly Jumped In July

Investor Home Purchases Crash 45% In Biggest Drop Since 2008

WTI Extends Gains After US Crude Stocks Hit Lowest Since 2022

Comments

Log in or sign up to join the conversation.