Image Source: Pixabay

We’ve got another full slate of earnings next week, with a wide variety of companies slated to report.

And when it comes to reports that investors should watch out for, Disney (DIS) should undoubtedly be on that list. The company is scheduled to reveal quarterly results on November 8th after the market’s close.

But how do expectations stack up heading into the release? We can use streaming results from Netflix (NFLX) as a small read-through concerning the company’s Disney+ results.

Let’s take a closer look.

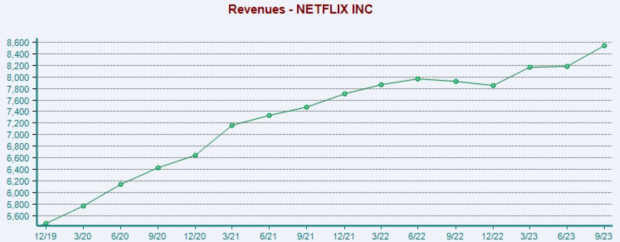

Netflix

Regarding headline figures, Netflix reported quarterly EPS of $3.73, beating the Zacks Consensus EPS Estimate of $3.46 handily and improving 20% year-over-year.

Quarterly revenue totaled $8.5 billion, improving 8% from the year-ago quarter and above the company’s previous forecast due to better-than-expected membership growth.

Image Source: Zacks Investment Research

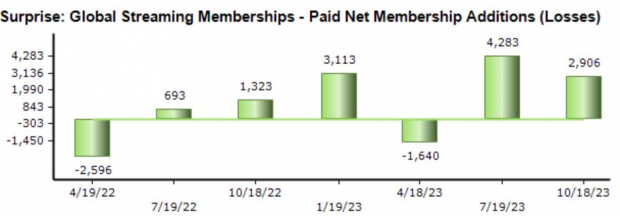

Paid Net Membership additions totaled 9 million, crushing expectations and boosted by the adoption of the company’s new ad-supported plans. Impressively, ad-supported memberships grew 70% quarter-over-quarter.

As we can see below, the company has consistently positively surprised on this metric as of late.

Image Source: Zacks Investment Research

To top it off, Netflix provided solid guidance, raising its free cash flow outlook and announcing more price hikes for membership plans in the US, UK, and France. Investors cheered on the news of price hikes and better-than-expected membership growth, with Netflix shares popping in the after-hours.

Disney

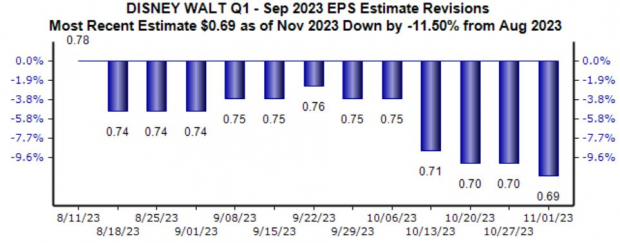

Analysts have been bearish for the quarter to be reported, with the $0.69 Zacks Consensus EPS Estimate down roughly 12% since just August. The value reflects a sizable 100% recovery in earnings from the year-ago quarter.

Image Source: Zacks Investment Research

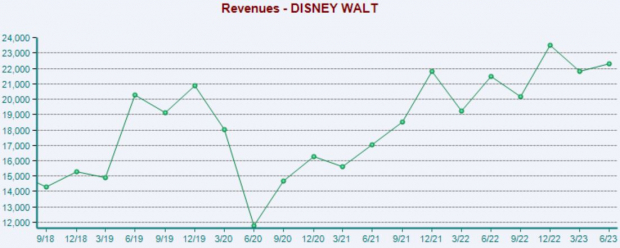

Top line expectations haven’t seen much movement, with the $21.7 billion consensus estimate down a fractional 0.5% during the same period and reflecting growth of 6% from the year-ago period.

Image Source: Zacks Investment Research

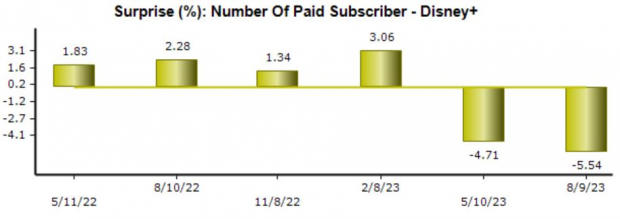

For the quarter to be reported, the Zacks Consensus Estimate for Disney+ subscribers stands at 146 million, reflecting an 11% decline from the year-ago period and zero change sequentially.

The company has fallen short of consensus Disney+ subscriber expectations in back-to-back releases, snapping a previous streak of positive beats.

Image Source: Zacks Investment Research

Bottom Line

Earnings season continues to chug along, with various companies reporting daily.

And next week, one notable release to watch for is entertainment titan Disney. Analysts have lowered their expectations for the quarter to be reported, with earnings forecasted to jump higher on 6% higher revenues.

Within the print, investors will undoubtedly be focused on Disney+ subscribers, an area that’s been expected to be a key growth driver for the company.

More By This Author:

Markets Up Big Again; Apple Beats Modestly3 Goldman Sachs Mutual Funds For Impressive Returns

PayPal Reports Q3 Earnings: What Key Metrics Have To Say

Comments

Log in or sign up to join the conversation.