Image source: Unsplash

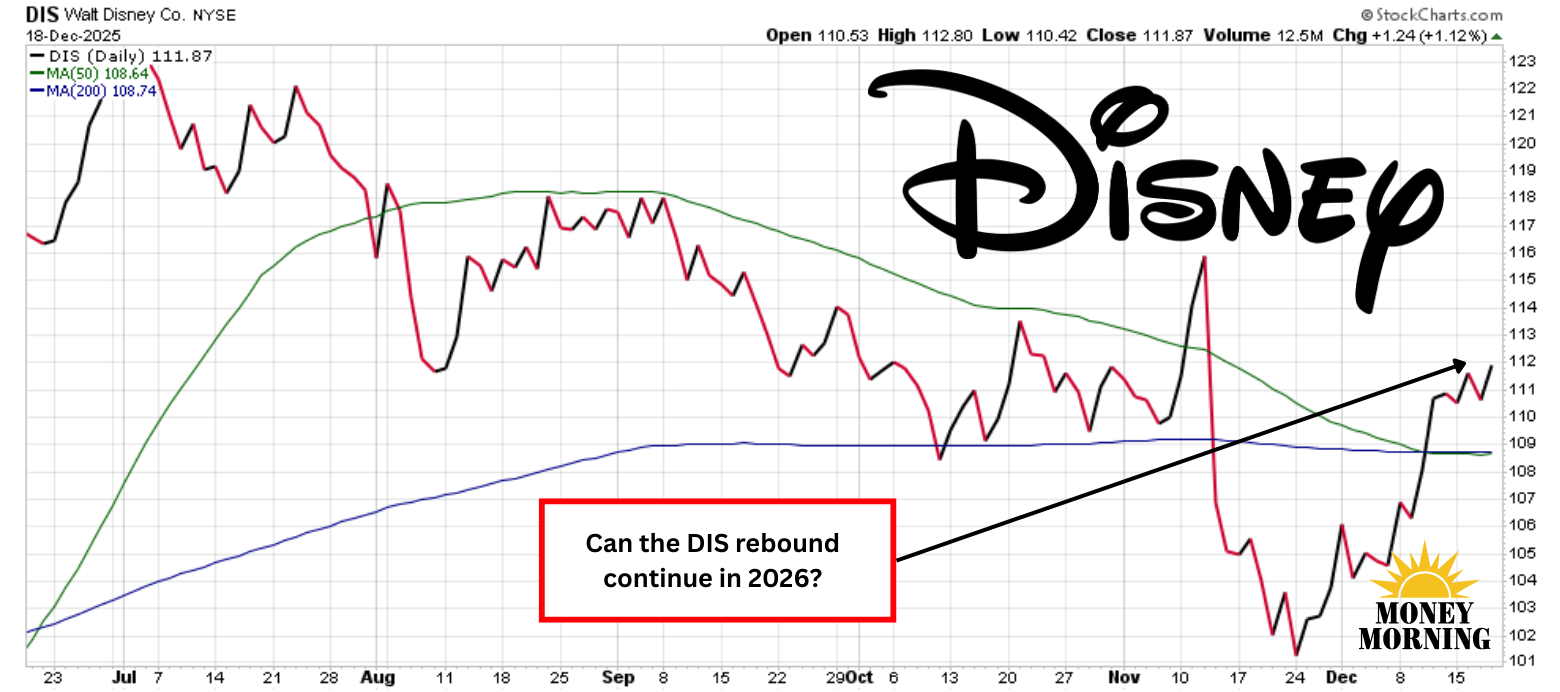

In 2025, shares of Disney (DIS) have gone essentially nowhere, up a meager 0.4% year-to-date. This flat performance was a disappointment for investors, especially when the S&P 500 rose 15%, and even Netflix (NFLX) – despite tumbling 30% from its 52-week high – has managed a 5% gain.

Other media stocks have fared far better, too. Fox (FOX)(FOXA) and Paramount Skydance (PSKY) have posted double-digit advances, and Warner Bros. Discovery (WBD) has surged on recurring strategic shifts and takeover news. Disney's stagnation stands out as particularly lackluster in a year of sector volatility.

Why Disney Lagged in 2025

Disney's underwhelming stock performance in 2025 stems from a combination of structural challenges and cyclical pressures across its key businesses. The company's linear TV networks continued their steep decline, with falling viewership and advertising revenue eroding profits in the Entertainment segment. Legacy media remains a drag, as cord-cutting accelerates and political ad cycles ended.

Streaming profitability improved – Disney+ finally turned the corner with positive contributions – but subscriber growth slowed as intense competition and price hikes risked churn. Only modest forecasts for Disney+ additions failed to excite investors, who remain wary of high content spending in a saturated market.

(Click on image to enlarge)

Theme parks, historically a reliable profit engine, faced headwinds from softer domestic attendance, higher operational costs, and macroeconomic uncertainty. Its international parks performed strongly, but U.S. operations saw tempered demand.

Broader concerns, including CEO succession as Bob Iger's tenure nears its 2026 end and lingering effects from prior restructuring charges, also weighed on sentiment. These factors collectively kept multiples compressed, leaving DIS trading at a discount to historical norms despite operational progress.

Prospects for a 2026 Rebound

Looking ahead, 2026 could mark a turning point for Disney, with several catalysts potentially driving growth and margin expansion. Analysts largely maintain a Buy consensus, with average price targets around $132 – implying 18% upside from its current price near $112.

Streaming is expected to build momentum, with Disney+ and Hulu targeting 10% operating margins through further price adjustments, bundling, and ad-tier adoption. The standalone ESPN direct-to-consumer service, along with integrated sports offerings, should boost ARPU and capture more of the shifting sports viewing landscape.

The Experiences segment holds particular promise, with new cruise ships launching in 2026 projected to nearly double Disney Cruise Line revenue, adding high-margin contributions. Theme parks could benefit from ongoing investments, but high prices remain a headwind.

Disney's content slate – including major releases like Avatar: Fire and Ash, Toy Story 5, and live-action Moana – could help revitalize studio performance, while disciplined expense management and share buybacks should support double-digit EPS growth, potentially expanding valuations as profitability increases.

Bottom Line

The streaming landscape is rapidly consolidating, with ad-supported models and bundling gaining traction as cord-cutting accelerates. Movie studios, however, face ongoing pressure from declining attendance and box office receipts as audiences grow selective and competition mounts.

Yet Disney's theme parks continue to hold enduring promise, delivering immersive experiences that remain despite premium pricing. Its sports offerings – anchored by ESPN – is a defensive moat in a fragmenting media world, with direct-to-consumer transitions unlocking new revenue streams.

Overall, Disney appears well-positioned for a rebound in 2026, blending defensive assets with growth levers. Risks about, but the stock offers attractive value for patient investors seeking a diversified entertainment leader.

More By This Author:

How Micron Technology Became The Best Nasdaq 100 Stock In 2025

Rocket Lab Launches Higher As SpaceX Prepares For 2026 IPO

Broadcom Is First Casualty Of The "Oracle Effect"

Comments

Log in or sign up to join the conversation.