Image Source: Unsplash

Story Theme: The Spending Squeeze Is Moving Up the Chain

The signs are on the wall, and they’re ones investors have seen before.

It starts small: people eat out less, skip the extra latte, hold off on a vacation. Then the slowdown spreads to bigger-ticket items like home improvements and, finally, cars.

That last part is where Carvana (CVNA) enters the story.

Consumer spending is tightening, and the auto sector is one of the first to feel the pinch once discretionary income dries up.

Over the past two weeks, auto parts giants AutoZone (AZO) and O’Reilly (ORLY) have both issued lowered outlooks, signaling slowing demand across the auto ecosystem.

Add to that, the Manheim Used Vehicle Value Index, which now shows prices leveling off, with a real possibility of moving higher again.

Rising wholesale prices mean Carvana’s inventory costs could climb just as consumer demand is rolling over. That’s a dangerous combination that eats into margins and pressures the bottom line, the exact same setup we saw in 2021 before CVNA’s major correction.

Earnings and News Note: A Partnership That Won’t Move the Needle

The company’s most recent announcement - a multi-year partnership with Stanford Athletics, the all-time NCAA team championship leader - may generate some feel-good headlines, but it won’t drive revenue or restore confidence in Carvana’s growth story.

This is marketing optics, not a fundamental catalyst.

Investors have seen this kind of PR-driven news cycle before: flashy sponsorships meant to maintain brand visibility in an increasingly difficult business environment. But right now, the market’s not rewarding sentiment, it’s punishing weak consumer trends.

Sentiment Note: “Buy the Dip” Is Losing Its Magic

Investor sentiment remains broadly optimistic, but it’s starting to turn complacent. The “buy-the-dip” crowd — which helped fuel Carvana’s meteoric rebound off its 2023 lows — is finally running out of conviction.

Each rebound attempt over the last month has been weaker than the last. The stock has now formed a pattern of lower highs and lower lows, the classic early warning sign of a deeper trend reversal. In other words, confidence is cracking beneath the surface, even if the headline numbers haven’t fully caught up yet.

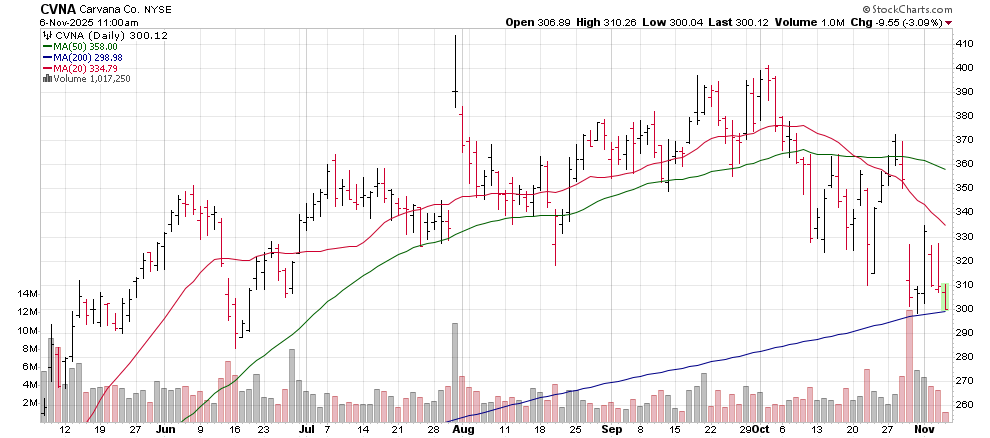

Technical Analysis Summary

Technically, the warning lights are flashing red.

Carvana’s 50-day moving average turned lower several weeks ago — a key sign of an intermediate bear trend developing. The last time this shift happened, in early 2025, CVNA dropped roughly 36% in the months that followed.

(Click on image to enlarge)

The stock is now sitting directly on its 200-day moving average, around $300, which is both a technical and psychological line in the sand.

The stock successfully tested this support back in April, but that test came with heavy volatility and strong follow-through buying. This time, the setup looks weaker, volume is drying up, and sentiment is fading.

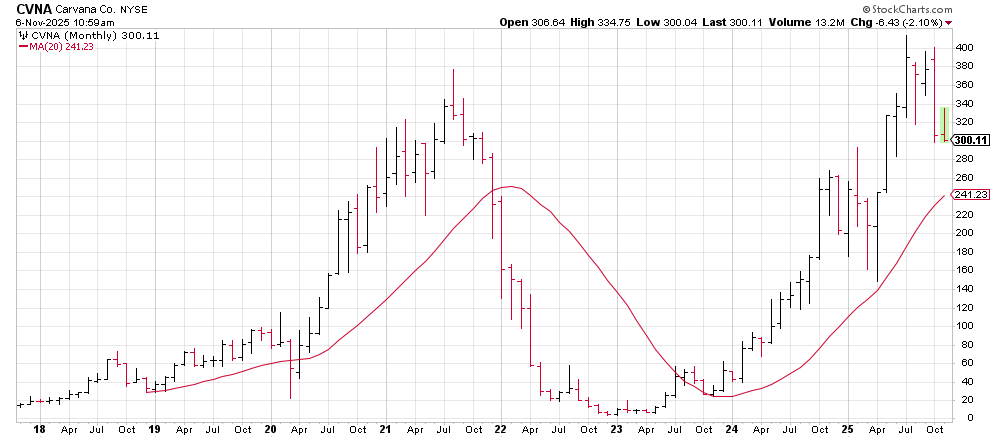

A break below $300 would likely trigger algorithmic and institutional selling. From there, downside momentum could build quickly, with the first target at $250, about 18% below current levels. Just below that, the 20-month moving average at $241 marks the long-term bull/bear demarcation line.

If Carvana loses that level, the long-term trend officially flips bearish.

Buy the Dip Price: $250 (High Risk Zone)

At $250, Carvana would enter a speculative support range where aggressive traders could look for short-term reversals — but only if market breadth improves and selling volume begins to fade.

Bear Market Tripline: $240 (Confirmed Long-Term Support)

(Click on image to enlarge)

If shares hit $240–$241, that would coincide with the 20-month moving average and could mark a durable long-term entry point if macro and consumer data stabilize. Until then, momentum remains firmly on the downside.

Bottom Line

The same signs that warned investors in 2021 are flashing again.

Consumer spending is contracting, used vehicle prices are plateauing, and the speculative bid in high-volatility names like Carvana is fading fast.

This is no longer a market driven by emotion, it’s one being driven by math, and the math says Carvana’s margin squeeze is just beginning.

If the $300 level breaks, buckle up — CVNA could be in for a sharp descent toward $250 or lower before the next real buying opportunity appears.

More By This Author:

Navitas Semiconductor Is Crashing Hard: Here’s What Investors Can Expect NextMcDonald’s Still A Buy After Earnings Miss… Here’s Why

Starbucks Bitter Brew: Coffee Shop Beating Swift Retreat In China

Comments

Log in or sign up to join the conversation.