Canopy Growth Inc. (CGC), a constituent in the munKNEE Pure-Play Pot Stock Index, reported its financial results for the third quarter fiscal 2021 ended December 31, 2020, today with an eye-popping net loss of $829 million.

(Canopy published its Q3, 2021 financial results in comparison to the same period a year ago (Q3, 2020) but the following summary is in comparison to the previous quarter (Q2, 2021) to provide clearer insights into the on-going, and most recent, trend and health of their business.)

Q3 Financial Highlights

(All figures are in Canadian dollars and compared to the previous quarter - see here)

- Net Revenue: increased 12.7% to a quarterly record of $152.5M (and by 23% vs. Q3, 2020)

- Other Revenue: increased 24.9% to $53.7M

- Cannabis Revenue: increased 7.0% to $98.8M

- Business-to-Business Recreational: increased 2.1% to $43.1M

- driven by store openings across Canada and improved market share performance

- Business-to-Consumer Recreational: increased 8.0% to $20.2M

- due to a full quarter of sales from ten new stores in Alberta, and same-store sales growth of 4% over Q2 2021 resulting from seasonal sales and promotional programs

- Canadian Medical: increased 0.7% to $14.0M

- driven primarily by a higher number of orders

- International Medical: increased 22.9% to $21.5M

- due to resolution of packaging issue with distributor that limited sales in Q2 2021

- Business-to-Business Recreational: increased 2.1% to $43.1M

- Gross Margin: declined to 16% from 19%

- Adj. EBITDA (Loss): improved 20.2% to $(68.4)M

- driven by net revenue growth and a decline in operating expenses

- Net Income (Loss): increased 758% to $(829.3)M from $(96.6)M

- driven primarily by impairment and restructuring charges and other related charges of $416M

- Cash on Hand: decreased 7.6% to $1.59B

- reflecting the EBITDA loss and capital investments

Q3 Business & Operational Highlights

(All figures are compared to the previous quarter)

- Further strengthened competitive positioning in the Canadian recreational market

- Increased recreational cannabis market share by 30bps to 15.7%

- Increased flower category market share by 180 bps

- increased value flower category market share by 310bps to 16.8%

- Maintained beverage category market share at 34% in spite of new beverage brands entering the marketplace, retaining the top 3 brands

- Increased recreational cannabis market share by 30bps to 15.7%

- Built further momentum in the U.S. market

- Increased distribution of its Martha Stewart health and wellness CBD products into 580+ Vitamin Shoppe and Super Supplements retail locations and is now outselling over 94% of all CBD brands in the U.S. in just 4 months since launch

- Improved distribution and strong consumer pull ensured continued strong growth in its S&B vaporizer products

- Strengthened direct (TW.com, shopcanopy.com) and third-party ecommerce sales channels.

- Further streamlined operations and improved organizational focus

- Ceased operations at a number of production facilities in Canada

- Divested its ownership in Canopy Rivers

- Increased its direct conditional ownership of TerrAscend Corp.

- Increased its ownership of Vert Mirabel greenhouse

Expected Medium-Term Financial Guidance

- Net Revenue CAGR of 40%-50% from FY 2022 to FY 2024

- Adjusted EBITDA to be positive during the second half of FY 2022

- Adjusted EBITDA Margin of 20% for the full year FY 2024; and

- Operating Cash Flow for the full year FY 2023 to be positive

- Free Cash Flow to be positive for the full year FY 2024.

Key drivers underpinning the Company's financial targets include:

- Growth of 40% in the Canadian legal recreational cannabis market growth in FY 2022 and market share gains;

- Increase in CAGR of 25%-30% from FY 2022 to FY 2024;

- Gains in market share in a stable-to-declining Canada medical cannabis market;

- Growth in international medical cannabis driven by the German market;

- Growth of the Company's U.S. CBD business, and consumer packaged goods business as a result of new product launches and distribution expansion in the U.S.;

- Cost savings of $150M - $200M; and

- Reduction in Capital Expenditures to below $200 million per year in FY 2021 and FY 2022.

Management Comments:

- David Klein, CEO, said: "...We are building a track record of winning in our core markets, while also accelerating our U.S. growth strategy with the momentum building behind the promising cannabis reform in the U.S."

- Mike Lee, CFO, added: "We are executing against our cost savings program, with several initiatives already completed and more underway to build a leaner and more agile business...[and] these cost savings, along with our top-line growth and continued cost discipline, puts Canopy firmly on a path to achieve profitability during Fiscal 2022, with further improvement anticipated beyond."

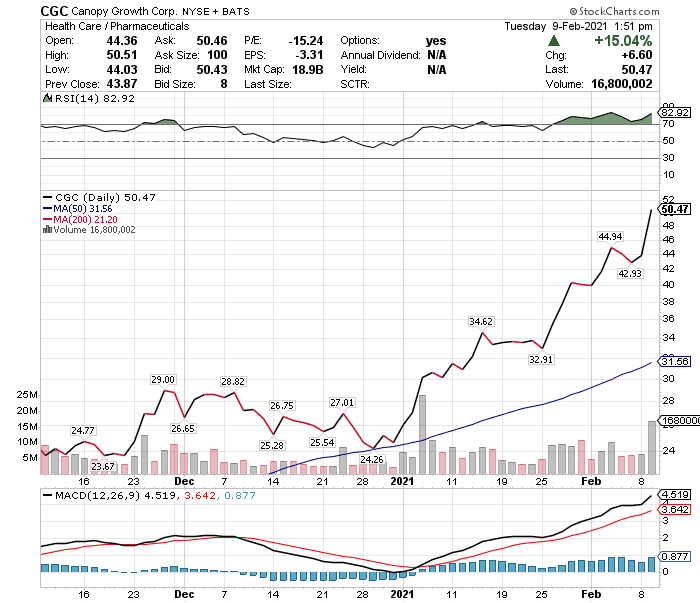

Stock Performance

As can be seen in the chart below Canopy Growth's stock price has been on a tear since the beginning of the year (up 78%) with no sign of it slowing down (+9.5% since the beginning of February) despite the poor Q3, 2021 financial results.

.webp)

Comments

Log in or sign up to join the conversation.