Cannabis Central: Wall Street Analysts Recommend These 14 "Pot" Stocks

The fragmented and overcrowded marijuana industry makes it difficult for investors to know which pot stocks will stand the test of time so this article identifies the 14 pot stocks followed by Wall Street analysts according to money.cnn.com and details their buy/hold/sell recommendations for the 7 companies with market capitalizations of C$1B or more, share prices of C$5/share or more (i.e. non-penny) and covered by at least 10 analysts.

- Canopy Growth (NYSE:CGC) is followed by 25 analysts of which 10 recommend a Buy, 10 a Hold and 1 a Sell. On average, they forecast a 12-month stock price appreciation of 55%. At its current price of approximately US$22.85/share that equates to a projected price of US$35.40/share.

- Aurora Cannabis (NYSE:ACB) is followed by 18 analysts of which 9 recommend a Buy, 7 a Hold and 2 a Sell. On average, they forecast a 12-month stock price appreciation of 80%. At its current price of approximately US$4.40/share that equates to US$7.90/share.

- Tilray Inc. (Nasdaq:TLRY) is followed by 17 analysts of which 5 recommend a Buy, 11 a Hold and 1 a Sell. Their average 12-month forecast is an increase of 98% to its current price of US$26.50/share which equates to a 1-year price of US$52.50/share.

- Hexo Inc. (NYSE:HEXO) is followed by 15 analysts of which 11 recommend a Buy, 3 a Hold and 1 a Sell. Their average 12-month forecast is an increase of 94% to its current price of US$4/share which equates to a 1-year price of US$7.75/share.

- Cronos Group (Nasdaq:CRON) is followed by 15 analysts of which 4 recommend a Buy, 10 a Hold and 1 a Sell. Their average 12-month forecast is an increase of 57% to its current price of US$9/share which equates to US$14/share.

- Aphria Inc. (NYSE:APHA) is followed by 11 analysts of which 8 recommend a Buy, 2 a Hold and 1 a Sell. Their average 12-month forecast is an increase of 93% to its current price of US$5.15/share which equates to US$9.95/share.

- Curaleaf Holdings (OTCQX:CURLF) is followed by 11 analysts of which 10 recommend a Buy and 1 a Hold. Their average 12-month forecast is an increase of 90% to its current price of US$5.40/share which equates to US$10.25/share.

On average, according to the Wall Street analysts covering them, the above 7 companies are expected to see their stock prices go up 81% in the next 12 months.

Not everyone is as optimistic as the above analysts, however. According to CIBC analyst John Zamparo, consensus revenue and EBITDA forecast from analysts for a number of cannabis companies are unachievable.

Consensus estimate for Aphria's F2020E revenue is $375M which, according to Zamparo, would have to grow by 54% per quarter, for the next four quarters, to meet this target. Below are a two reasons why Aphria could have difficulty achieving its $375M goal:

- its Double Diamond facility has been waiting on its Health Canada Cultivation license since January 2018 and, once approved, the facility would need two full crop rotations before being awarded its sales license which would further delay revenue from cannabis grown at the facility for an additional six months.

- the Company’s Extraction Center of Excellence has also been delayed and with limited extraction capabilities, the Company may not be ready for the legalization of edibles and derivative products expected in December.

- In addition, the current short volume ratio on Aphria is 30% which is up 58% from a month ago.

Analyst consensus estimate for Canopy Growth’s FY2020 revenue is $620M which, according to Zamparo, would necessitate its revenue having to grow by 37% per quarter, over the next three quarters, to meet the revenue target. This will be difficult for Canopy to achieve, as:

- it has been losing market to Aurora Cannabis,

- it has invested heavily in cannabis beverages and it is unclear whether beverages will take off and, as well,

- it has had problems with its oils and capsules ($8.0M in oils and capsules were returned in the Company’s last quarter).

Analyst consensus estimate for F2020E revenue for HEXO is $505M and again, according to Zamparo, it would necessitate HEXO having to grow revenue by 80% per quarter, for the next five quarters, to meet this target. HEXO could face some headwinds in achieving this target as:

- its revenues are derived primarily from Quebec and, as of June 2019, Quebec had the lowest amount of retail stores at 15, the lowest of any major Canadian province.

- Additionally, the Quebec government has limited the sale of derivatives and edible products, with the sale of candies, confections and desserts (including chocolate) banned. Edibles are expected to drive much of the revenue growth for Cannabis 2.0 and this ban could limit HEXO’s growth opportunity.

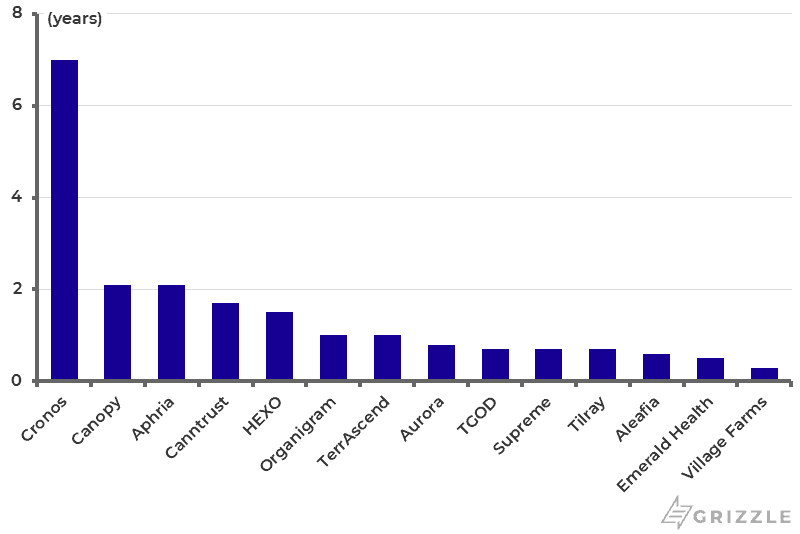

It also should be noted that it is imperative to pick companies with the lowest cash burn and the deepest discount to net assets so they can weather any storm that comes their way and, as the charts below show, a number of the companies mentioned in this article don't have many years - or even months - of cash in their coffers. These companies are Aurora, Tilray, Curaleaf, MedMen and Village Farms.

Source: Sedar, Sec.Gov, Grizzle Estimates.

Source: Sedar, Grizzle Estimates, Sec.Gov

Source: Sedar, Sec.Gov, Grizzle Estimates.

The additional 7 companies below are being covered by between 5 and 9 analysts each with all of them seeing their stock prices go UP in the next 12 months, namely:

- iAnthus (ITHUF) +333%

- Harvest Health (HRVSF) +275%

- Trulieve Cannabis (TCNNF) +170%

- MedMen Enterprises (MMNFF) +168%

- Village Farms (Nasdaq:VFF) +149%

- Green Thumb Industries (GTBIF) + 97%

- Charlotte's Web (CWBHF) +54%

The cannabis stock universe has had a wild ride over the past 6 months. Hopefully, the above analysis will provide some pertinent information to help you assess how best to invest in this volatile market going forward.

Good summary but it doesn't say much else - what's your personal take on these stocks?