Image: Bigstock

The Zacks Consumer Staples Sector has weathered a brutal macroeconomic storm better than most in 2022, down a marginal 2% and extensively outperforming the general market. However, the sector’s 4% uptick over the last month has marginally lagged the S&P 500’s 6% gain.

Companies within the Consumer Staples sector generate revenue in the face of both good and bad economic times, helping explain why it’s displayed such remarkable relative strength year-to-date.

A widely-recognized company in the sector, Campbell Soup (CPB - Free Report) , is on deck to unveil Q4 results on September 1st before market open.

Campbell Soup is a worldwide manufacturer and marketer of high-quality, branded convenience food products. We see their items on shelves at seemingly every store. Currently, the company sports a Zacks Rank #2 (Buy) with an overall VGM Score of an A.

How does everything stack up for the food titan heading into the print? Let’s take a closer look.

Share Performance & Valuation

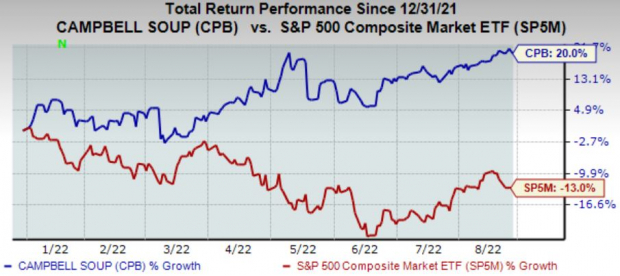

Year-to-date, CPB shares have been notably strong, tacking on a stellar 20% in value and absolutely crushing the S&P 500’s performance.

Image Source: Zacks Investment Research

Over the last month, Campbell Soup shares have continued their market-beating trajectory, tacking on nearly 5% in value vs. the S&P 500’s 3% gain.

Image Source: Zacks Investment Research

The favorable price action of CPB shares tells us that buyers have had a tough grip on shares all year long, undoubtedly a positive amid all of the red in 2022.

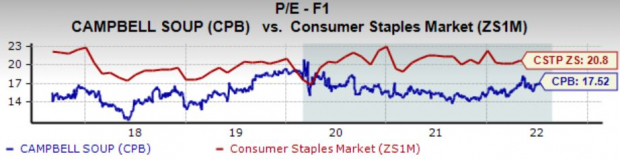

In addition, the company carries a 17.5X forward earnings multiple, representing a substantial 16% discount relative to its Zacks Consumer Discretionary Sector.

Campbell Soup carries a Style Score of a B for Value.

Image Source: Zacks Investment Research

Quarterly Estimates

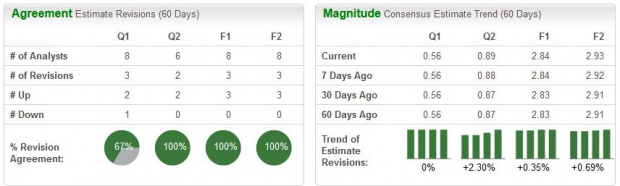

Analysts have primarily been bullish for the quarter to be reported over the last 60 days, with two positive estimate revisions hitting the tape. The Zacks Consensus EPS Estimate of $0.56 reflects a respectable 2% Y/Y uptick in quarterly earnings.

Image Source: Zacks Investment Research

CPB’s top-line appears to be in good health as well – the Zacks Consensus Sales Estimate of $2 billion reflects a notable 5.4% increase from year-ago quarterly sales of $1.8 billion.

Quarterly Performance & Market Reactions

Campbell Soup has been on an impressive earnings streak, exceeding the Zacks Consensus EPS Estimate in four consecutive quarters. Just in its latest print, the food titan penciled in a notable 15% bottom-line beat.

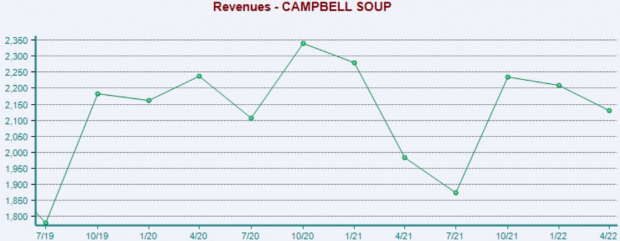

However, top-line results have primarily been mixed – over CPB’s last ten quarters, the company has registered five revenue beats. Below is a chart illustrating the company’s revenue on a quarterly basis.

Image Source: Zacks Investment Research

The market has had favorable reactions as of late to CPB’s quarterly prints, with shares moving up following three of its previous four releases.

Putting Everything Together

Campbell Soup shares have posted market-beating returns not just year-to-date but over the last month as well, signaling that buyers have been busy.

In addition, shares trade at solid valuation multiples, with its forward P/E ratio nicely beneath its Zacks Sector average.

Analysts have been primarily bullish in their earnings outlook, and estimates reflect solid growth in revenue and earnings.

Furthermore, the company has consistently exceeded bottom-line estimates, but top-line results have been mixed over its last ten prints.

Heading into the release, Campbell Soup carries a Zacks Rank #2 (Buy) with an Earnings ESP Score of 0.6%.

More By This Author:

3 Dividend Kings Income Investors Will Love

Airline Stock Roundup: Ryanair's Solid FY23 Traffic View, American Airline's Deal & More

Ulta Beauty Q2 Earnings And Revenues Top Estimates

Comments

Log in or sign up to join the conversation.