Buy Equity Vol - But Not For The Reason You Think

Most equity traders are of the belief that volatility only rises in down markets. It’s easy to see why.

Looking back over the past two decades, bouts of increased volatility have predominately been associated with periods of market stress. On the other side of the coin, large stock market rallies have brought about lower volatility readings.

(Click on image to enlarge)

(Click on image to enlarge)

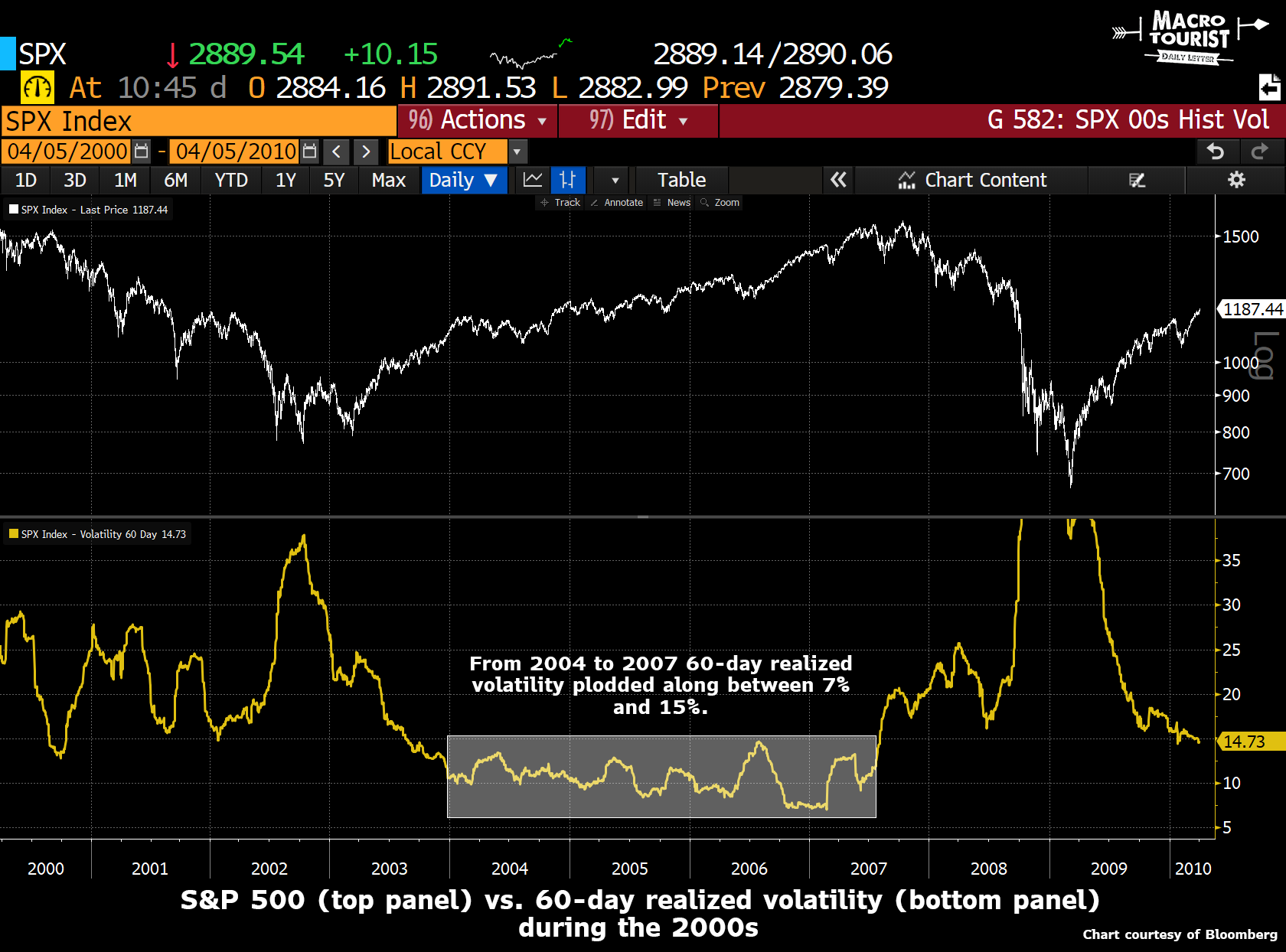

In fact, in 2017 while the stock market was running like it stole something, historical realized 60-day volatility stayed glued under 10% for the entire year! This was an astounding accomplishment that had a feel of “unnatural” calmness to it.

With this past market action, it’s little wonder that most traders believe that higher stocks equals lower volatility.

Yet is this always the case? Does one necessarily have to lead to the other?

Maybe we are not thinking back far enough.

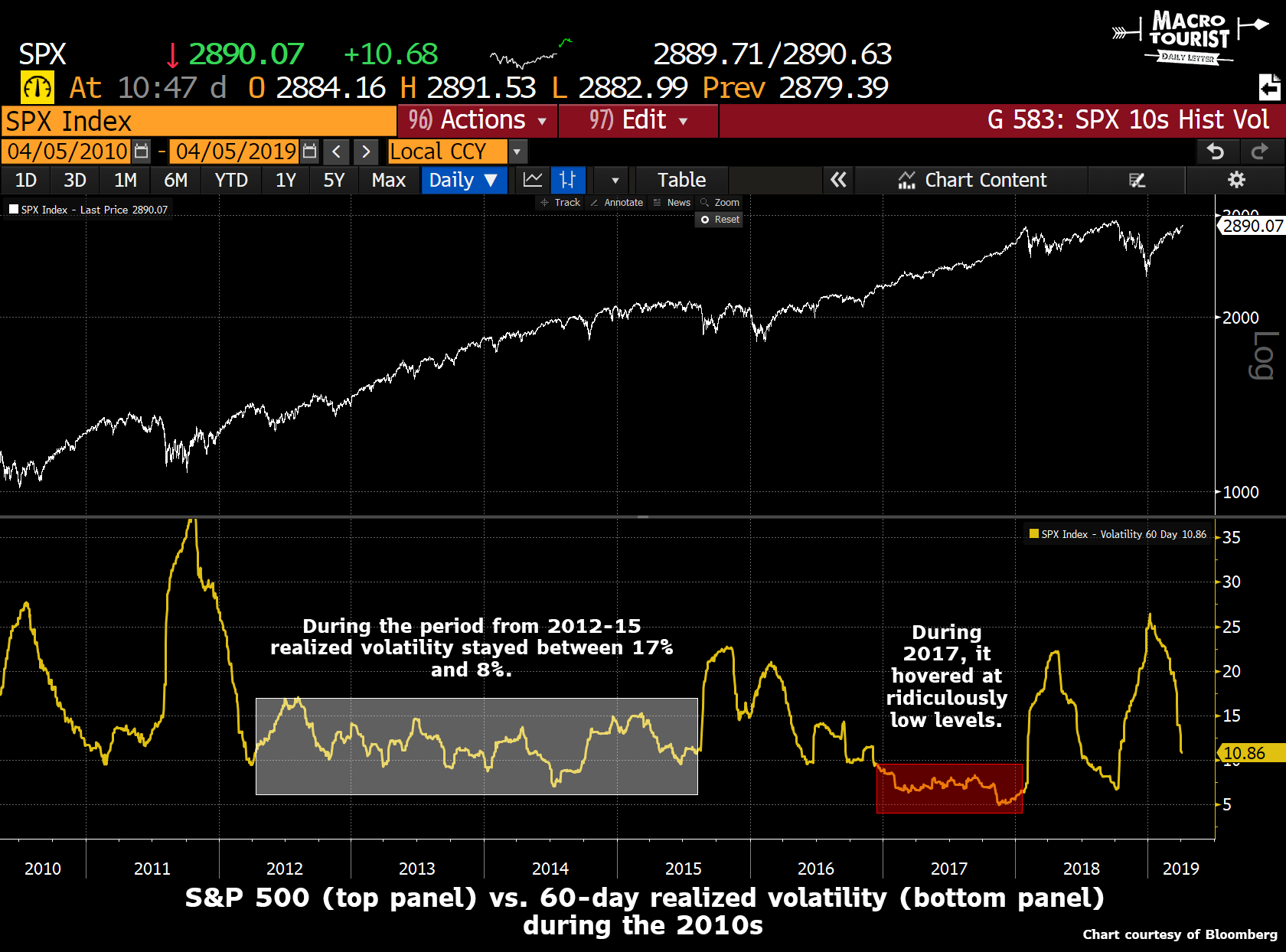

If we remember back one more decade and examine the stock market during the 1990s, we notice a most curious phenomenon.

(Click on image to enlarge)

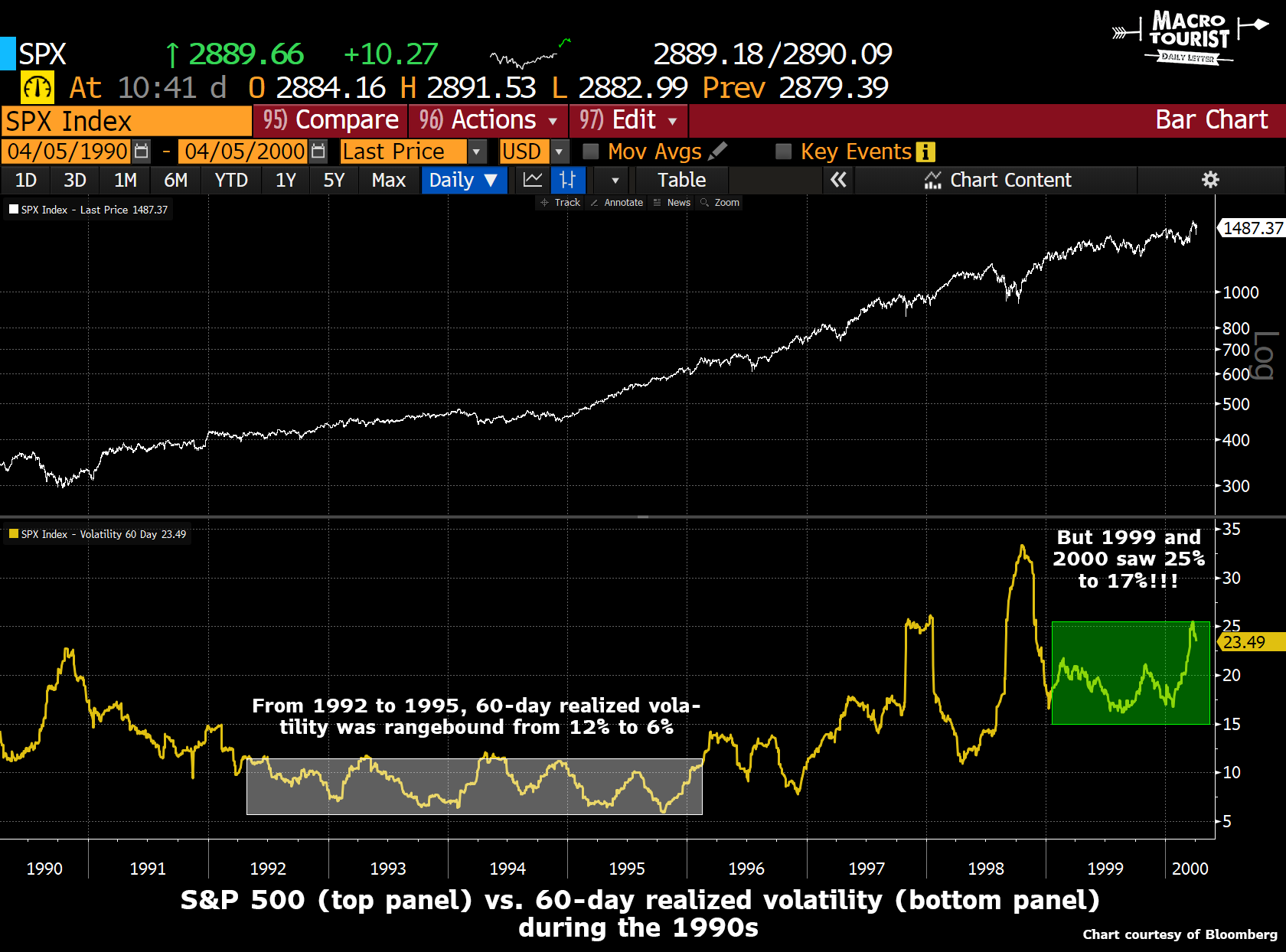

The initial stock market rise during the start of the decade was accompanied by the expected lower volatility. The 60-day realized vol bounced between 6% and 12%.

Then the Long Term Capital Management crisis hit. To no one’s surprise, volatility spiked. Nothing unexpected there.

However, after the initial panic subsided, the stock market resumed its advance, yet volatility did not return to its previous lower levels.

For the next two years, as the DotCom bubble exploded higher, volatility stayed firmly elevated.

The historical 60-day volatility gyrated in a new range between 16% and 25% - not what would have been predicted given that the bull market’s largest advance in terms of price was still ahead of it.

So this meant that purchasers of options were blessed with a more volatile underlying asset, which is one of the main determinants of an option’s value.

The most interesting part of this story? In 1998 during the LTCM crisis, the 3-month 10-year yield curve inverted - just as it did recently - and back then, many participants were also convinced that a recession was right around the corner.

(Click on image to enlarge)

Instead, the volatile crazy part of the equity rally was still ahead.

What’s Jimmy Rogers’ famous line from Market Wizards? Something about the final 50% of the move in price often occurs in the last 10% of the period in time?

(Click on image to enlarge)

Although many pundits are currently bearish - predicting that the yield curve inversion was an ominous signal that the economy is about to roll over, I believe there is a decent chance we will instead see a repeat of the 1999-2000 final push higher.

The best part of this scenario? You don’t have to pay up to express this opinion.

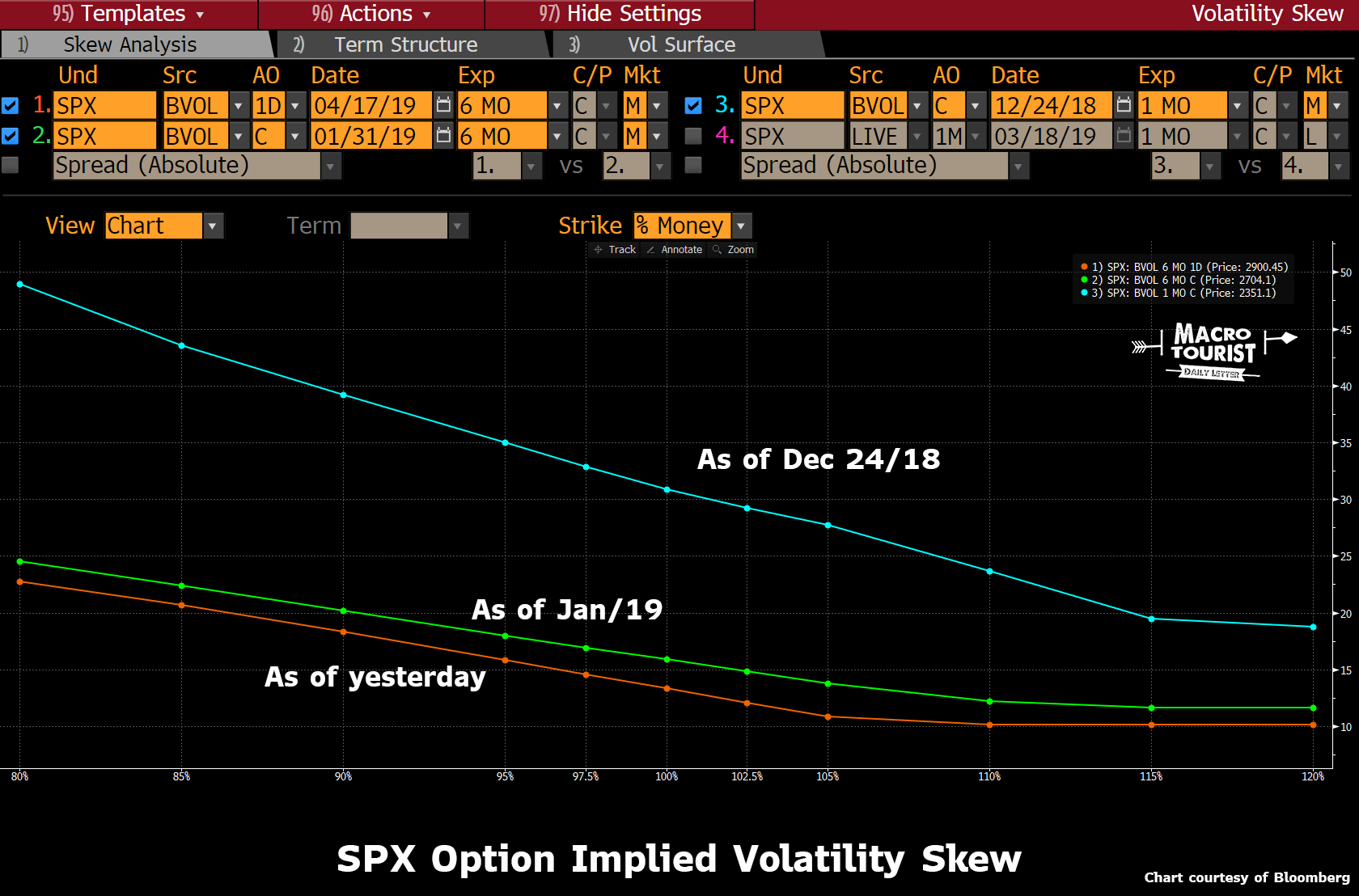

Even though larger future realized volatilities might be in the cards, implied volatilies in the S&P 500 have collapsed.

(Click on image to enlarge)

6-month out of the money call options at the time of the Christmas-eve-bottom were pushing 20%. A month later they had sunk to 12%. Today they are around 10%.

This is due to the mistaken belief that stock market rallies always equal lower volatility.

I contend this is not always the case, and on a risk-adjusted basis, they are giving these call options away.

It’s rarely being cheaper to hedge against an upside move, yet conditions have seldom been this ripe for that possibility.

Disclosure: None.

Buying VOL is always dangerous, and best if done with VIX options not VIX-ETPs imo. No contango in VIX options

What’s your vehicle of choice for this? $UVXY?

Welcome!

Good Q.