As we welcome a new year and its many possibilities, it’s important to reflect on where the markets and investor psychology sit on the pendulum of greed and despair. Howard Marks’ concept of the pendulum, used as a tool to gauge the psychological temperature of investors, offers a wonderful lens through which to evaluate how stocks are priced. Throughout history, markets have consistently swung toward extremes, building momentum until they reach a tipping point. This cyclical behavior stems from the nature of markets as self-organizing, complex systems that rarely settle in equilibrium.

Investors often lose sight of two fundamental characteristics of markets: they are non-linear and non-monotonic. At certain thresholds, their direction reverses. A fitting analogy can be found in nature: as water cools, it becomes denser and sinks—until it reaches 32°F, where the relationship reverses, and water begins to expand and rise. This phenomenon, though counterintuitive, is essential for life on Earth. Similarly, market behavior is driven by inherent rules and thresholds that are often misunderstood or ignored, with profound consequences when these thresholds are crossed.

As we enter 2025, it’s clear that markets have swung beyond euphoria into something even more troubling: a collective mindset that views markets as quasi-utilities, with limited downside and infinite upside. This perspective is more dangerous than despair or greed—emotions that at least keep investors actively engaged. Today’s complacency fosters dangerous overconfidence, stifling critical thinking and risk awareness.

Complacency, unlike greed or despair, erodes the discipline essential for long-term success. It encourages passive decision-making, weakens adaptability, and discourages investors from questioning their strategies. It thrives on a false sense of security, much like the way punctuated equilibrium and power laws in complex systems lull participants into confidence before swiftly exposing vulnerabilities and forcing adaptation. It’s akin to a pilot relying on autopilot through worsening weather. A crash becomes inevitable if action isn’t taken, yet the pilot’s confidence and skills have deteriorated to the point of incompetence. Complacency also stifles critical feedback loops, amplifying the severity of eventual consequences.

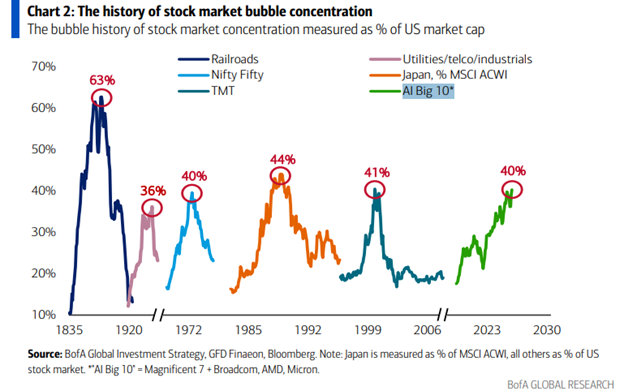

This mindset is not new. A similar complacency dominated the late 1960s and 1970s, during the era of the Nifty Fifty. While the specific circumstances differ, with less leverage employed in that era, the underlying psychological fallacy remains the same: a belief that markets can defy the inherent rules of complex systems indefinitely.

Throughout our lifetime, we have witnessed several bubbles, from the tech bubble to the global financial crisis. These painful lessons highlight the dangers of ignoring historical patterns. Unfortunately, many professionals managing money today lack the lived experience of bubbles prior, amplifying the risk of recency bias—the tendency to overemphasize recent trends while neglecting the broader historical context.

What makes today’s environment particularly alarming is the confluence of factors fueling what we call the “everything bubble.” These include unprecedented market cap concentration in a handful of stocks, record levels of leverage among equity investors, the dominance of passive investing over active strategies, unsustainable national debt, a decade-plus of monetary expansion and suppressed interest rates, and speculative excesses in fringe assets (e.g., Fartcoin, a memecoin, reached a $1.54b market cap this year making it larger than 50% of US-listed companies). Any one of these factors is concerning; together, they create a highly unstable environment that far outpaces that of the Nifty Fifty.

As an aside, for those who believe the Federal Reserve will support markets indefinitely and have a handle on the recent surge of inflation, it’s important to remember that they spent over decade and a half keeping interest rates near zero in an attempt to spur “healthy inflation” to 2% and it failed. What reason is there to believe they can now control inflation effectively using the same tools?

Underlying these trends is the same psychological fallacy that has persisted throughout history: the belief that we are somehow immune to the natural rules governing markets and complex systems. This hubris has fostered the complacency we see today, leaving markets highly vulnerable to significant disruption when these imbalances inevitably correct.

We believe that over the next decade, markets are unlikely to deliver more than low single-digit returns and most likely will be negative—a reflection of the excesses and complacency that dominate today’s investment landscape. While many managers have succumbed to the pressure of chasing the “new Nifty Fifty,” we refuse to follow that path. Instead, we focus on investing in compounders with durable moats, buying them at depressed valuations, and holding them for extended periods.

When the complacency bubble inevitably bursts, we are confident in our ability to capitalize on mispricing opportunities, while others struggle to rediscover the independence and decisiveness required to navigate a transformed market landscape. In a world where complacency has lulled many into a false sense of security, we believe our commitment to rigorous analysis and contrarian thinking will position us to thrive in the face of inevitable market corrections.

More By This Author:

Dissecting Our Discipline

Don’t Trust Antitrust

Presidential Stock Market Euphoria

Comments

Log in or sign up to join the conversation.