Amazon.com, Inc. (AMZN) topped third-quarter earnings and revenue estimates last week and raised its guidance. Amazon’s e-commerce and advertising units are mounting comebacks after their post-Covid slowdowns, while its new AI-focused efforts are boosting its vital cloud business.

AMZN stock surged after its October 26 report to help it retake some key moving averages. Amazon’s recent jump is part of an impressive rally off its lows.

Yet, investors can still buy Amazon far below its all-time highs and its average Zacks price target. Plus, its valuation levels are enticing given its commitment to the bottom line in our new higher interest rate environment, alongside Meta and many others.

Quick Q3 Recap

Amazon’s quarterly revenue climbed by 13% to $143.08 billion, with AWS cloud sales up 12% YoY. The company’s high-margin third-party seller services and advertising units popped by 20% and 26%, respectively, with its lower-margin core online stores segment up 7%.

Amazon’s adjusted earnings soared 325% from the year-ago period to $0.85 per share, topping our estimate by 47%. Amazon has crushed our bottom-line estimates by an average of 55% in the last four quarters.

AMZN’s operating income hit a record of $11.2 billion, up from $2.5 billion in Q3 FY22. AWS operating income hit $7.0 billion vs. $5.4 billion. Amazon’s free cash flow improved to an inflow of $21.4 billion for the trailing twelve months vs. an outflow of $19.7 billion in the comparable 12-month period.

(Click on image to enlarge)

Image Source: Zacks Investment Research

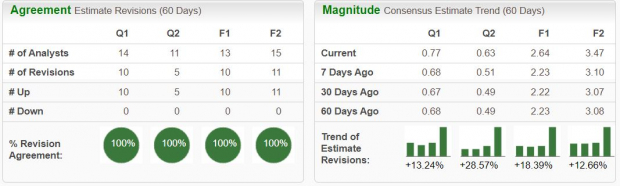

Growth Outlook

Wall Street is a forward-looking world and it was impressed by Amazon’s guidance. AMZN’s consensus Q4 EPS estimate is up by 13% since its report, with its outlook for fiscal 2023 up 18% and 13% higher for FY24. On top of that, its most accurate/most recent estimates have come in above the current Zacks consensus. Amazon’s overall improved earnings outlook helps it land a Zacks Rank #1 (Strong Buy) right now.

Amazon is firmly focused on cutting costs and streamlining its business after years of attempting to post breakneck growth and expansion into new areas no matter the cost.

Yet, the strength and importance of its cloud computing and e-commerce businesses will help it churn out stable double-digit growth in the near-term and possibly beyond. Amazon reportedly held 32% of the cloud computing market last quarter vs. Microsoft’s (MSFT) 22% and Google’s 11%. AMZN captures roughly 38% of the total U.S. e-commerce market.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Current Zacks estimates call for Amazon to post 11% revenue growth in 2023 to hit $570.42 billion and then climb 12% higher next year to pull in $637.42 billion—adding a projected $124 billion to the top line between FY22 and FY24.

CEO Andy Jassy highlighted the benefits Amazon is experiencing since it shifted from a single national fulfillment network in the U.S. to eight distinct regions. On the AWS cloud computing front, the firm is rolling out more AI-focused efforts to help attract customers to spend more as everyone races to not get left behind in the new frontier of tech. Amazon is also boosting AWS margins by rolling out more in-house chips.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Performance, Technical Levels & Valuation

Amazon stock has climbed 675% in the last decade to blow away the Zacks Tech sector’s 215%, Meta’s (META) 545%, and the S&P 500’s 145%. More recently, AMZN is roughly neck and neck with Tech over the trailing five years, with it currently down around 27% from its record highs.

AMZN has surged 61% YTD to top Microsoft’s 43% and Tech’s 30%, yet it still trades 28% below its average Zacks price target of $170.60 per share. Investors must also remember that its price per share is much lower (and more attainable to the average investor) after it completed its 20-for-1 stock split last summer.

Image Source: Zacks Investment Research

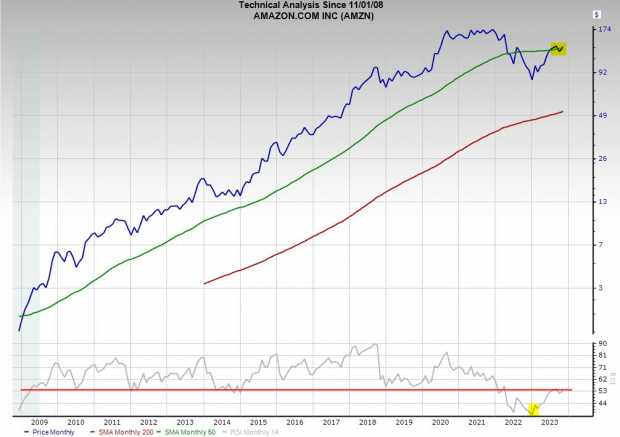

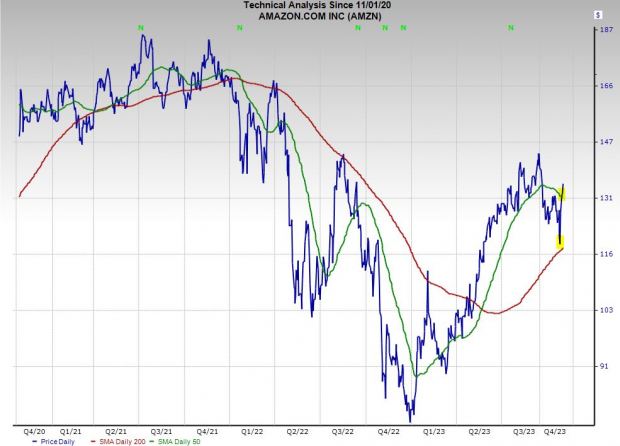

Amazon found support near its 200-day moving average after its upbeat report and its recent rebound has it out of oversold RSI territory and above its 50-day once again. The stock is also now retaking both its 200-week moving average and its 50-month, while still trading at neutral RSI levels on a 15-year timeframe.

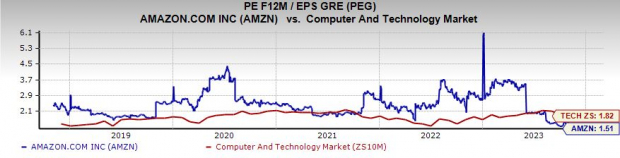

Turning to valuation, Amazon trades 65% below its highs at 44.6X forward 12-month earnings, which is still rather pricey. Yet, its peg ratio, which factors in its longer-term earnings outlook, marks an 18% discount vs. the Zacks tech sector.

Bottom Line

All in, investors with long-term outlooks might want to consider buying Amazon at these levels and making it part of their portfolios for the foreseeable future as AMZN undergoes its transformation into a mature, stable growth tech stock.

More By This Author:

Time To Finally Buy These 3 Beaten-Down Tech Stocks Before Earnings?Bull Of The Day: Lamb Weston Holdings, Inc.

Bear Of The Day: The Clorox Company

Comments

Log in or sign up to join the conversation.