The Clorox Company (CLX) has been on a rather steady decline after it went on an unsustainable surge at the start of Covid.

Clorox’s near-term outlook appears disappointing, driven lower by a cybersecurity attack that was disclosed in August. Despite its fall from its peaks, CLX shares are still rather pricey compared to the wider Consumer Staples sector.

CLX Basics

Clorox’s portfolio includes its namesake disinfectant wipes and other household and heavy-duty cleaning items designed for the healthcare industry and beyond. On top of that, the firm’s portfolio features everything from Kingsford charcoal and Brita water filters to Hidden Valley, Burt’s Bees, and beyond.

Clorox breaks up its business into four categories: Health and Wellness (Cleaning; Professional Products), Household (Bags and Wraps; Cat Litter; Grilling), Lifestyle (Food; Natural Personal Care; Water Filtration), and International (Sales Outside the U.S.).

CLX has posted rather steady sales growth for much of the last 20 years, outside of a few small YoY pullbacks. Clorox grew its fiscal 2023 revenue (period ended in June) by 4%.

CLX on October 4 outlined preliminary Q1 FY24 financial data. Clorox said sales are expected to decrease by between 28% and 23%, with organic sales “now expected to decrease by 26% to 21%” vs. its prior expectations “of mid-single-digits growth as provided in the Q4 earnings remarks.”

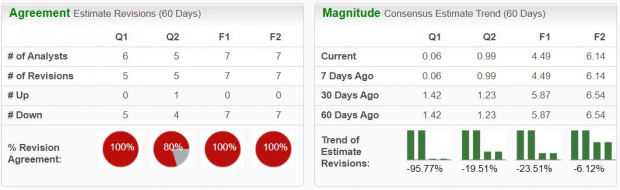

(Click on image to enlarge)

Image Source: Zacks Investment Research

The downbeat outlook “is due to the impacts of the recent cybersecurity attack that was disclosed in August, which caused wide-scale disruption of Clorox's operations, including order processing delays and significant product outages. Shipment and consumption trends prior to the cybersecurity attack were in line with the Company's prior expectations.”

Meanwhile, its adjusted EPS are expected range between a loss of -$0.40 to $0.00, with the cybersecurity attack more than offsetting the “benefits of pricing, cost savings and supply chain optimization.”

Clorox’s FY24 revenue is projected to dip by -5.5%, based on Zacks estimates. Meanwhile, its adjusted earnings are expected to decline by 12% YoY. But these estimates could get worse since they don’t yet fully account for the updated Q1 guidance.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Bottom Line

Clorox’s downward earnings revisions help it land a Zacks Rank #5 (Strong Sell) right now. CLX’s first quarter earnings estimate is already down 96%, with its FY24 figure 24% lower.

Plus, its most accurate/most recent quarterly earnings estimates came in at -$0.20 vs. the current consensus of +$0.06 per share.

CLX stock has fallen roughly 25% over the last six months and around 50% from its peaks. Despite the fall, it still trades above its 10-year median and at a 60% premium compared to the Zacks Consumer Staples sector at 25.5X forward 12-month earnings.

All in, investors might want to stay away from Clorox, at least until it reports its results and provides updated FY24 guidance.

More By This Author:

Big Tech Earnings: Time To Buy Microsoft, Amazon, And Meta Stock?How To Find Great Cheap Stocks Under $10 To Buy Right Now

Bull of the Day: AppLovin Corporation

Comments

Log in or sign up to join the conversation.