There is no exact definition for blue chip stocks. We define it as a stock with at least ten consecutive years of dividend increases. We believe an established track record of annual dividend increases going back at least a decade shows a company’s ability to generate steady growth and raise its dividend, even in a recession.

As a result, we feel that blue chip stocks are among the safest dividend stocks investors can buy.

In this article, we will analyze Williams-Sonoma, Inc. (WSM) as part of the 2022 Blue Chip Stocks In Focus series.

Business Overview

Williams-Sonoma is a specialty retailer that operates home furnishing and houseware brands, such as Williams-Sonoma, Pottery Barn, West Elm, Rejuvenation, Mark and Graham, and others. Williams-Sonoma operates traditional brick-and-mortar retail locations but also sells its goods through e-commerce and direct-mail catalogs. Williams-Sonoma was founded in 1956, is headquartered in San Francisco, and currently trades with a market capitalization of $9.93 billion.

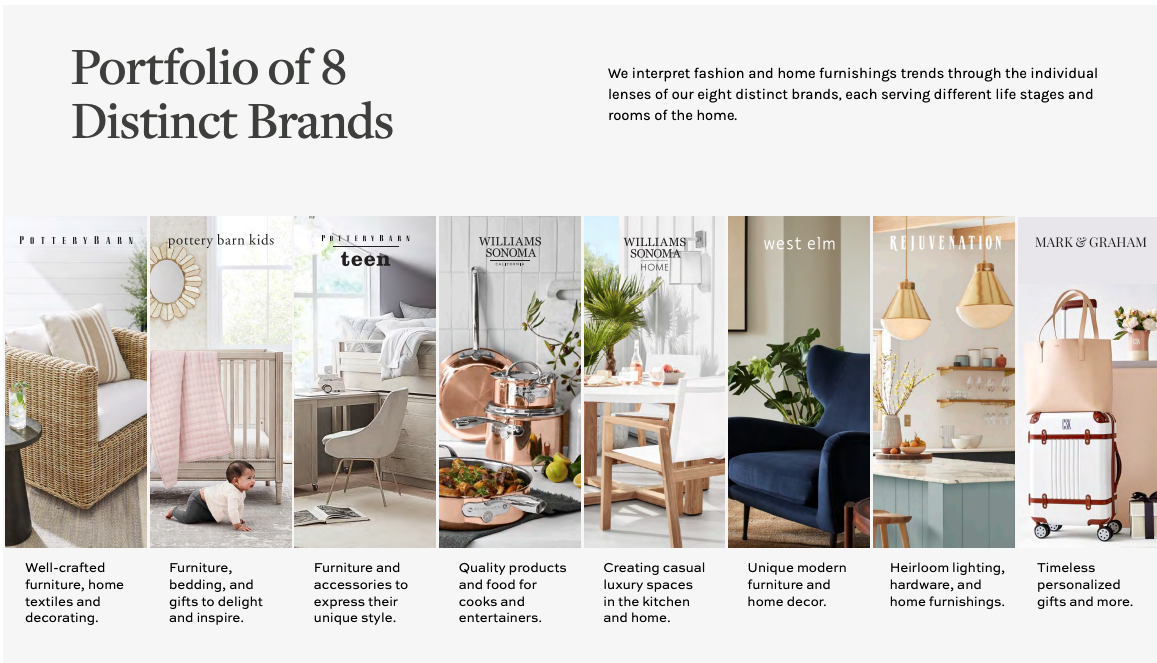

The company has a portfolio of eight brands that are sought after. Four of the eight brands generates over $1 billion in sales.

Source: Investor Presentation

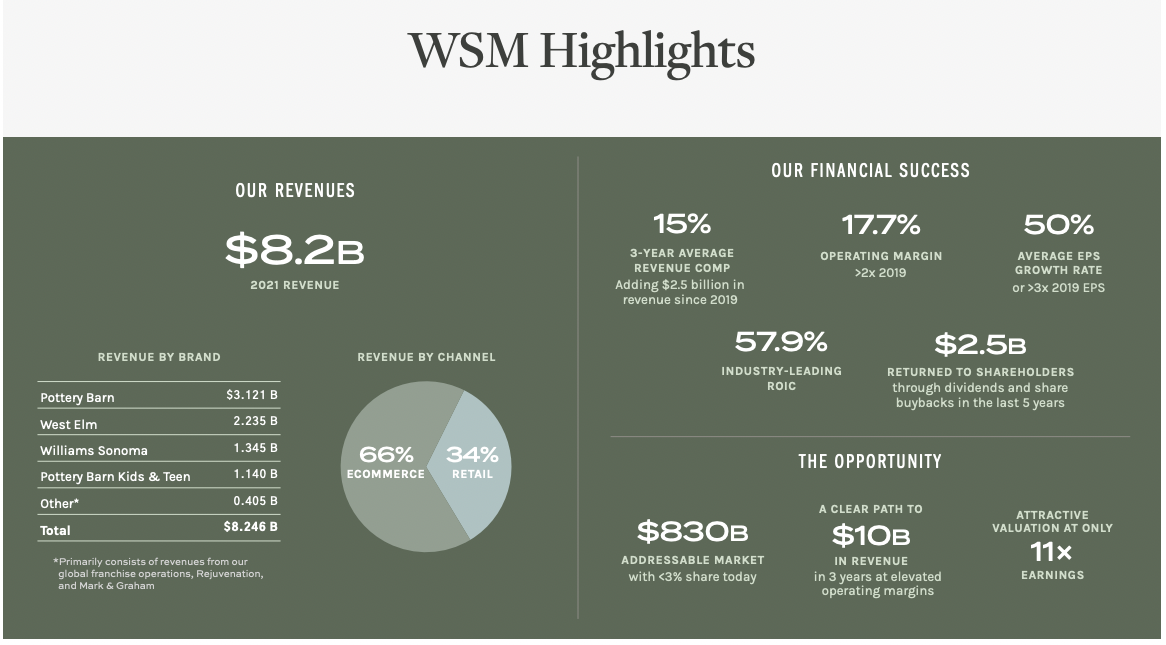

On May 5th, 2022, the company reported first-quarter results for the Fiscal Year (FY)2023. The company ends its fiscal year at the end of January of each year. For the quarter, revenue has increased 8.1% compared to the first quarter of FY2022. An increase in comparable sales growth drove this. Comparable brand revenue growth of 9.5%, including Pottery Barn at 14.6% and West Elm at 12.8%.

Net income for the quarter was also up compared to the first quarter of 2022. Net income grew 11.5% year-over-year (YoY). This was due to the increase in revenue and lower gross profits for the quarter.

Operating margin of 17.1%; GAAP operating margin expansion of 140bps; non-GAAP operating margin expansion of 120bps. Overall, earnings for the quarter were $3.50 per share, compared to $2.90 per share in the first quarter of 2021. This represents a YoY increase of 20.7%.

The company was also able to repurchase over $500 million in shares and paid $58 million in dividends in the first quarter. This was thanks to a strong liquidity position of $325 million in cash and the generation of $185 million in operating cash flow.

Source: Investor Presentation

Growth Prospects

In the past four years, the company has been growing earnings tremendously. For example, from FY2019 to FY2022, earnings grew 24%,9%, 87% and 64%, respectively. Thus, earnings have been growing over the past ten years at a Compound Annual Growth Rate (CAGR) of 17.5%.

We do not thank that this kind of growth will continue for the company. We are taking a more conservative stand and expect the company to grow earnings at a 4% annual rate for the next five years.

Based on this, we expect the company to have earnings of $17.28 per share for FY2027.

Another growth driver for earnings will come from increasing market shares. Currently, WSM has 22% of the market share, while most companies have only 7% of the home furnishing category.

Source: Investor Presentation

Competitive Advantages & Recession Performance

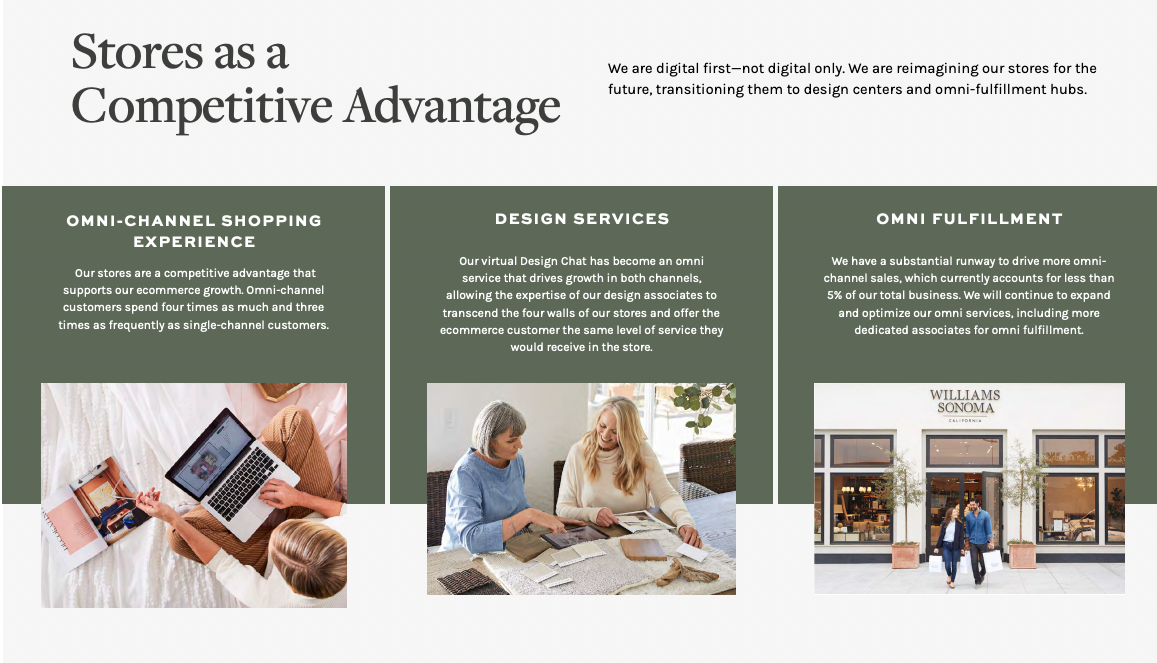

Williams-Sonoma’s competitive advantage lies in its unique product portfolio and successful move to the online space. Notably, the company competes against formidable foes, including traditional brick-and-mortar home improvement retailers like Home Depot and Lowe’s and e-commerce players like Amazon.

Another competitive advantage is the company’s intangible brand assets, which have historically been the supporting factor in the firm’s top-and bottom-line growth, as its ability to drive repeat business is widely reliant on customer loyalty and intelligent marketing and merchandising.

Source: Investor Presentation

The company did not do well during the Great recession. As you see below, earnings did fall significantly in 2009. However, it bounces vigorously in the following years. Yet, during the COVID-19 pandemic, the company’s earnings increase substantially by 87% year-over-year (YoY).

You can see a rundown of Williams Sonoma Inc.’s earnings-per-share from 2007 to 2011 below:

- 2007 earnings-per-share of $1.77

- 2008 earnings-per-share of $1.77 (Flat 0% YoY)

- 2009 earnings-per-share of $0.35 (Decrease 80% YoY)

- 2010 earnings-per-share of $0.95 (Increase 171% YoY)

- 2011 earnings-per-share of $1.95 (Increase 105% YoY)

While earnings-per-share fell significantly in 2009, the company quickly recovered. By 2011, earnings-per-share were above the 2007 level.

In addition, WSM has a solid balance sheet with ample cash, sufficient liquidity, and manageable debt levels. For example, the company has a debt-to-equity ratio of 0.95, which is an acceptable ratio.

Valuation & Expected Returns

Williams-Sonoma has a fascinating valuation history, with a typical multiple in the mid-teens coupled with occasional bouts of a 20+ earnings multiple. We assume a fair price-to-earnings ratio of 14.0, which is close to the 7-year average of the stock.

The stock is currently trading at a 9.1X earnings ratio, which is much lower than our assumed reasonable valuation level. The depressed valuation has resulted from record earnings, the effect of inflation on valuation, and fears that inflation will hurt margins in the future.

We view all these headwinds as temporary. If the stock reverts to its average valuation level over the next five years, it will enjoy a 7% annualized gain in its returns.

Overall, with the low valuation and earnings growth with a market-beating dividend yield of 2.1%, we expect that an investor of the company can expect an annual return of 11% over the next five years.

Final Thoughts

Williams-Sonoma is an excellent run company with a good potential of double-digit return over the next five years. The company has transformed itself into an omnichannel retailer with a significant e-commerce presence, which has proved resilient during the coronavirus crisis. The balance sheet is good, and the company’s future continues to look bright. Thus, we rate Williams-Sonoma as a buy at the current price.

More By This Author:

Blue Chip Stocks In Focus: Walgreens Boots Alliance

Blue Chip Stocks In Focus: Qualcomm

Blue Chip Stocks In Focus: Archer Daniels Midland Company

Comments

Log in or sign up to join the conversation.