Image Source: Unsplash

There is no exact definition for blue chip stocks. We define it as a stock with at least ten consecutive years of dividend increases. We believe an established track record of annual dividend increases going back at least a decade shows a company’s ability to generate steady growth and raise its dividend, even in a recession.

As a result, we feel that blue chip stocks are among the safest dividend stocks investors can buy. This article will analyze Axis Capital Holdings (AXS) as part of the 2022 Blue Chip Stocks In Focus series.

Business Overview

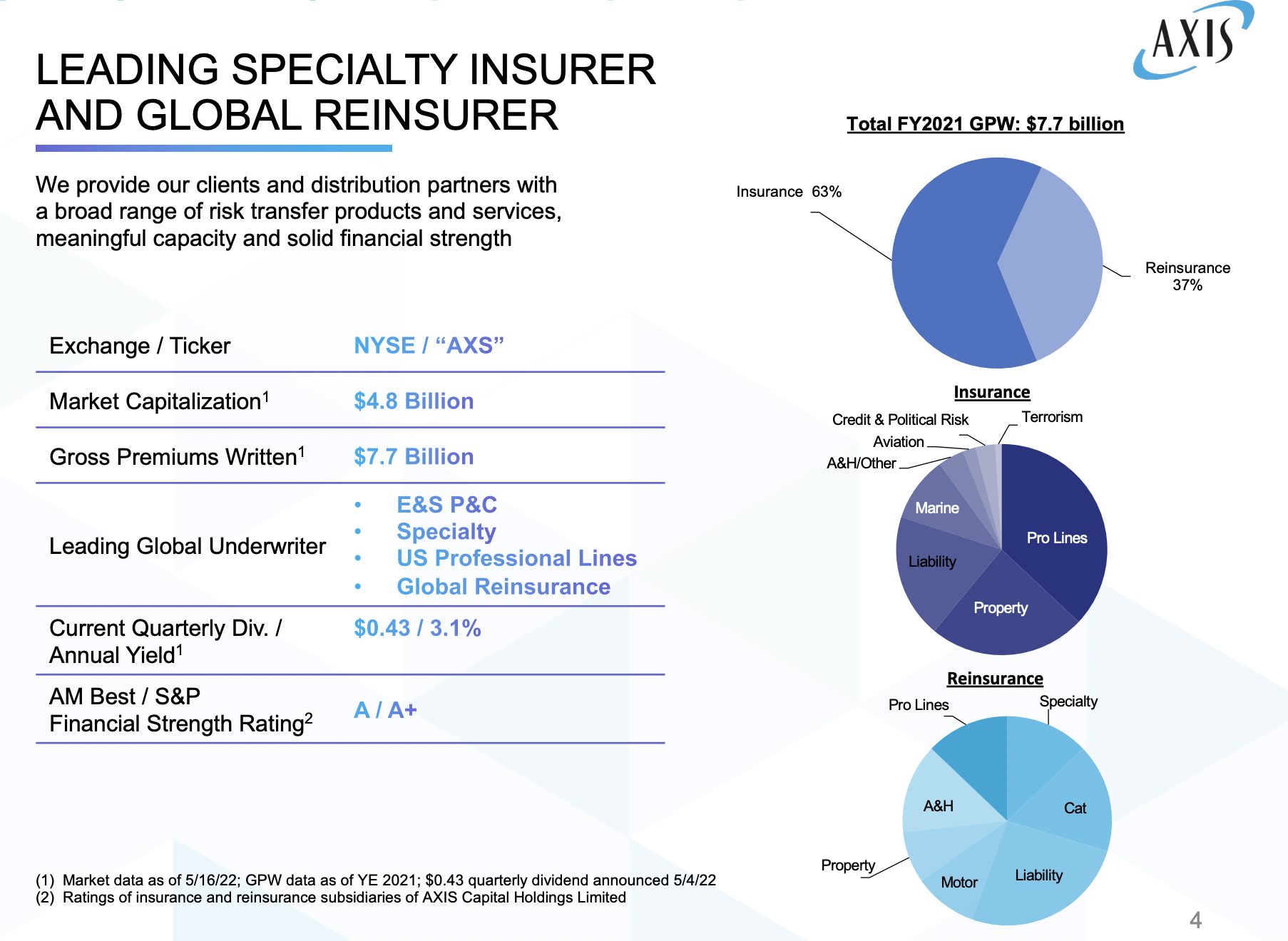

Axis Capital is a global insurer and reinsurer that was founded in 2001. It is split into Insurance and Reinsurance divisions, with the former making up just over half of total revenue. It offers a broad range of risk transfer products for a diverse base of customers, and it has a market capitalization of around $4.3 billion and about $5.3 billion in annual revenue. Axis also has an impressive 20-year streak of dividend increases.

Axis reported second-quarter and first six months’ earnings on July 26, 2022, and results were much weaker than expected on both the top and bottom lines. Earnings-per-share came to 32 cents, which missed estimates by 90 cents. Revenue was down 11% year-over-year to $1.2 billion, which missed expectations by more than $100 million.

On a dollar basis, earnings came to $27 million, down sharply from $228 million a year ago. Operating income was $149 million, or $1.74 per share. These were down from $171 million, or $2.00 per share, in the year-ago period. This does not include a $16 million charge resulting from reorganization expenses.

The company’s fixed income portfolio book yield was 2.4% at the end of Q2, and the market yield was 4.3%. Book value declined 8% from Q1, driven by net unrealized losses and common dividends declared, and partially offset by a small amount of net income.

The company repurchased 600 thousand shares during the quarter for $35 million. Gross premiums written increased by $172 million, or 9%, to $2.1 billion. The insurance segment led the way with 16% growth, partially offset by a decline of 4% in the reinsurance segment.

For the six months, Gross premiums written are up 17.9% compared to the first six months of 2021. While net premiums were written were up 20.6% versus the six months of 2021. Earnings per diluted common share were $1.97, a notable decrease compared to the six months of 2021, which was $4.04 per share.

Source: Investor Presentation

Growth Prospects

Earnings-per-share has been tremendously volatile during the past decade, which is expected for an insurer. Axis’ profits rise and fall based upon how efficiently it writes premiums along with factors that are out of its control, including claims, as we saw in 2019 and especially in 2020.

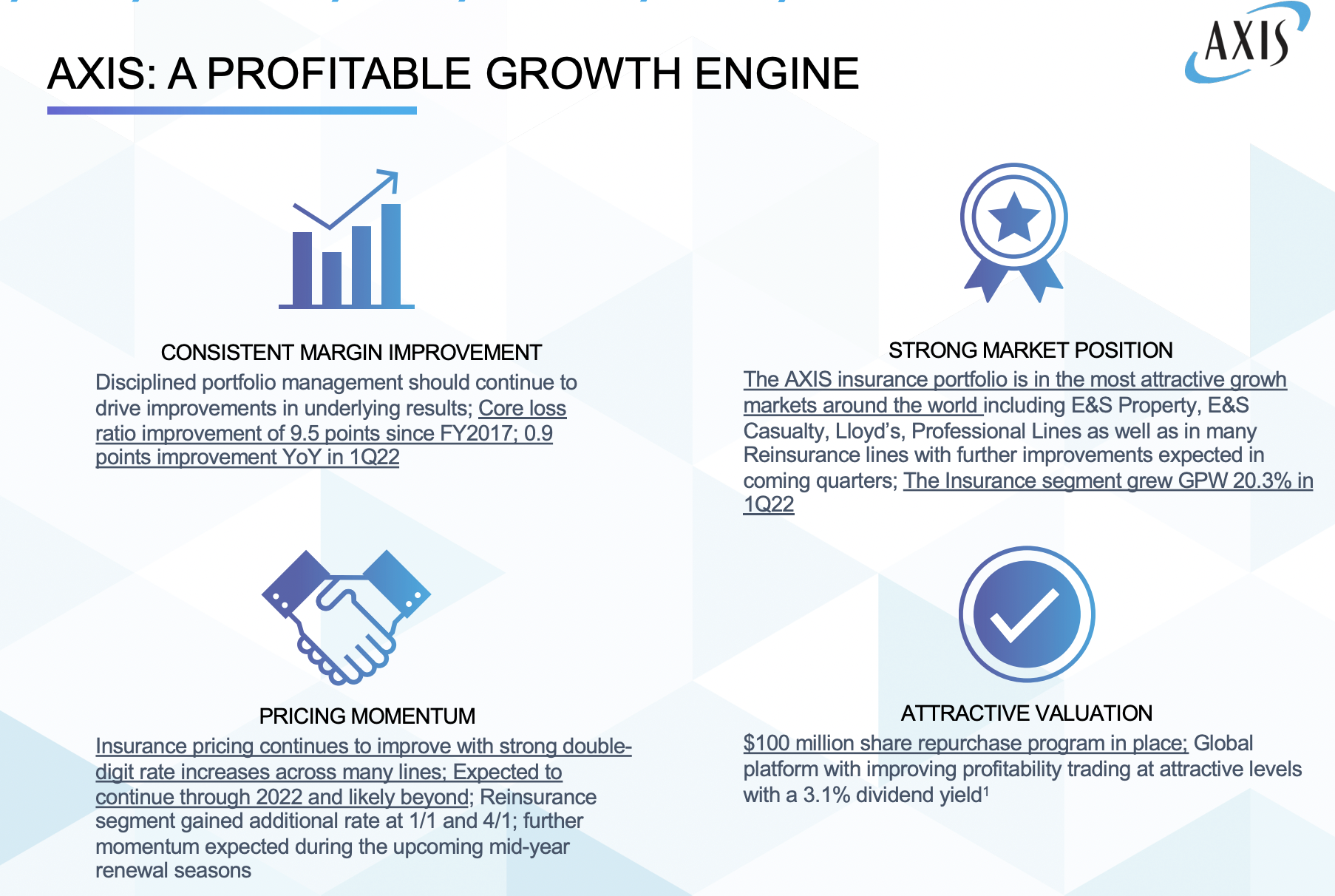

Typical weather/catastrophe losses weighed on 2020, but COVID-19 did as well, which shouldn’t be repeated going forward from 2022. Axis benefits from higher interest rates as its investment income rises commensurately. We forecast 5% growth going forward from the current base.

Axis continues to grow its business organically through prudent risk-taking, in addition to further acquisitions. There is potential room for additional upside should Axis avoid years like 2017 in the future or if it completes a sizable acquisition.

Overall, Axis looks well positioned to maintain its current book value and, in our view, continues to be well-managed. However, the fact remains its earnings are primarily outside of its control, and the long-term earnings growth outlook is murky from here.

Source: Investor Presentation

Competitive Advantages & Recession Performance

Competitive advantages are tough to come by for insurers, and Axis is no different. On the bright side, recessions tend not to sway performance one way or the other, so there is a diversifying component to adding Axis to one’s portfolio.

However, Axis Capital did not do very well doing the Great Recession. Not only did the share price see a massive fall in price at about 45%, but earnings for the company also saw a significant decrease.

You can see a rundown of Axis Capital’s earnings-per-share from 2007 to 2011 below:

- 2007 earnings-per-share of $6.29.

- 2008 earnings-per-share of $2.81 (55% decrease).

- 2009 earnings-per-share of $5.10 (81% increase).

- 2010 earnings-per-share of $4.60 (10% decrease).

- 2011 earnings-per-share of $(1.30) (127% decrease).

The company did see a significant decrease in earnings in 2008. However, it also saw a nice comeback in 2009 with an 81% increase in earnings. But, in the following two years, earnings decreased notably.

The company has a good balance sheet. The company sports a debt-to-equity ratio of 0.3 and a long-term debt-to-capital ratio of 23.2. Also, the interest coverage ratio is 7.9, which is a high ratio, meaning that the company covers the interest on its debt very well. Overall, the company sports an S&P credit rating of A-, an investment grade rating.

Valuation & Expected Returns

The company’s price-to-book ratio has moved around significantly as its fortunes have risen and fallen, similar to other insurance companies’ valuations. The stock has been down since the start of the year, and shares have recently been trading closer to our estimate of fair value and with a 3.4% dividend yield. We, therefore, forecast a slight headwind to total returns from the valuation in the coming years.

We also expect a 5% earnings growth over the next five years. Putting this all together, the dividend yield of 3.4%, earnings growth of 5%, and a slight negative valuation multiple will give an investor about a 7% annual return over the next five years.

Final Thoughts

We see Axis as somewhat overvalued and offering investors a total annual return potential of 7% in the coming years. We see very limited growth from 2021 levels given the company’s history of significant, unexpected losses on events like the pandemic, typhoons, etc. We still believe Axis is well managed, but note that its earnings and book value growth are primarily out of its control. Thus, we think that Axis deserves a hold rating.

More By This Author:

Blue Chip Stocks In Focus: The Kroger Co.Blue Chip Stocks In Focus: First Of Long Island Corp.

Blue Chip Stocks In Focus: Target Corporation

Comments

Log in or sign up to join the conversation.