The Mosaic Company (MOS) is expected to see earnings decline this year after the Ukraine War spiked fertilizer prices last year. But this Zacks Rank #5 (Strong Sell) is still bullish on fertilizer demand in 2023.

The Mosaic Company, headquartered in Tampa, FL, is one of the world's leading producers and marketers of concentrated phosphate and potash crop nutrients. It supplies phosphates and potash fertilizers and feeding ingredients for the global agriculture industry.

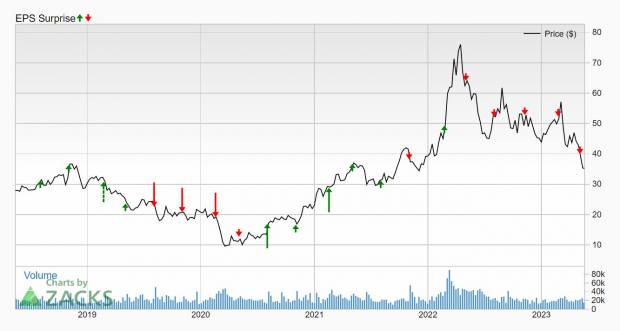

Another Earnings Miss in Q1

On May 3, Mosaic reported its first quarter 2023 earnings and it reported earnings of $1.14 which was a miss of 10.9%, or $0.14. The Zacks Consensus was looking for $1.28.

It was the fifth earnings miss in a row.

Image Source: Zacks Investment Research

Revenue fell 8% to $3.6 billion reflecting the impact of lower prices which were somewhat offset by higher volumes.

In its three big categories, volumes were higher in 2023 than in 2022. In Potash, sales volume million tonnes was 1.9 compared to 1.8 last year. In Phosphate, sales volume million tonnes was 1.8 compared to 1.7 last year and in Mosaic Fertilizantes sales volume million tonnes was 2.1 compared to 1.8.

But it was the opposite in sales price.

Potash MOP Selling Price fell to $421 from $582 last year. Phosphate DAP Selling Price fell to $660 from $785. Mosaic Fertilizantes finished product selling price was $646, down from $817.

Gross margins fell to 18.6% from 36.7% last year.

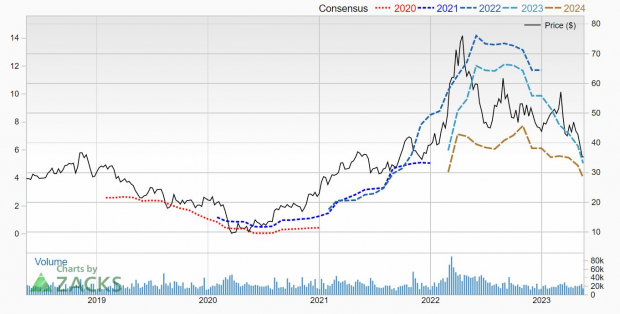

Earnings Estimates Slashed

The analysts have been aggressively cutting their earnings estimates for 2023 and 2024 the last 3 months as fertilizer prices have softened.

For 2023, 4 have cut the last 30 days and 1 in just the last week. The 2023 Zacks Consensus Estimate has plunged to $5.05 from $8.45 in just the last 3 months.

That's an earnings decline of 54% from 2022, when it made $11.01.

The cuts extend into 2024 as well. 5 estimates were cut in the last month for 2024 pushing the Zacks Consensus down to $4.02 from $5.48 just 3 months before.

That's another 20.4% drop.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Mosaic Optimistic About Demand

To counter all that analyst bearishness, which is the reason the stock is a Zacks Rank #5 (Strong Sell), is the company's industry outlook.

It expects the grain and oilseed markets to remain tight through 2023 and beyond. Mosaic said in North America, sentiment has improved "significantly" compared to the second half of 2022.

Mosaic also said spring nutrient application rates were trending toward normal levels. And for both potash and phosphates, supply constraints remain.

Shares Down Big

But until earnings turn around and get raised, instead of cut, investors have decided to flee the stock. Year-to-date, shares are down 18.4%, but over the last year shares have fallen 45.5%.

It's dirt cheap, even with the earnings cuts. It's trading with a forward P/E of just 7.

Mosaic is also generating plenty of free cash flow. Mosaic is standing by its 2023 Capital Allocation Strategy, which is to return largely all of the 2023 free cash flow back to shareholders.

In the first quarter, that meant $608 million was returned through share repurchases and dividends. It's dividend is currently yielding 2.3%.

Fertilizers are a commodity. It's a challenging industry in which to invest. For investors interested in the fertilizers, and Mosaic, you may want to wait until the Zacks Rank moves higher. Keep Mosaic on your watch list.

More By This Author:

Bull of the Day: Skechers

How To Create Your Own Mini Berkshire Hathaway

Screening For Top Ranked Value Stocks

Comments

Log in or sign up to join the conversation.