Leslies (LESL) , a leading specialty retailer of swimming pool and spa products, has unfortunately been on the wrong side of some significant downward earnings revisions, giving it a Zacks Rank #5 (Strong Sell).

Leslie’s seems to be suffering from the pool related spending that was pulled forward following the Covid-19 pandemic. In 2020, during the first summer of lockdowns, pool builds, and pool related spending exploded well above trend because everybody was stuck at home, and this continued through 2021.

However, that spending reversed considerably when people were again able to leave their homes. Additionally, with the pressures from inflation shifting budget priorities, and renewed interest in travel, pool-focused spending has fallen considerably as is evident from LESL’s most recent quarterly earnings report.

Company and Performance

Catering to both residential and commercial customers, Leslie's offers a wide range of high-quality products, including pool chemicals, equipment, maintenance tools, and accessories. The company operates through a combination of retail stores, e-commerce, and a mobile app, providing convenient access to essential pool and spa supplies.

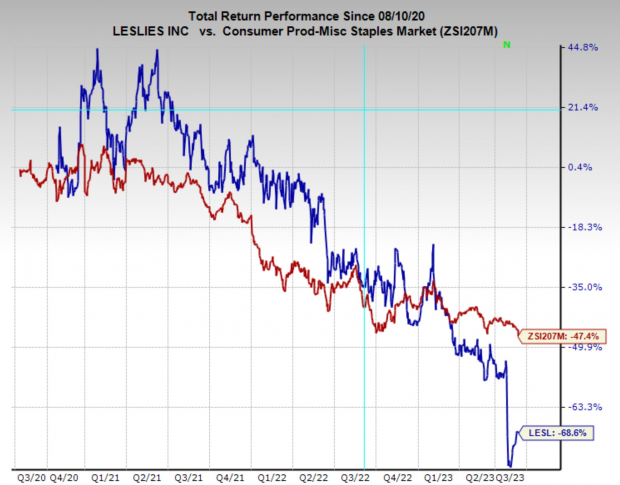

Although the company was founded all the way back in 1963, it has changed hands several times since then. More recently, in 2017 the company was purchased by a private equity firm who then brought the company public through an IPO in 2020. The stock has not performed well since then, down -69% since its IPO.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Earnings Downgrades

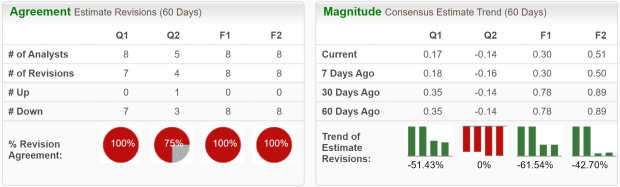

Earnings estimates have experienced some severe revisions lower over the last two months reflecting the shifting economics in the pool industry. Current quarter earnings estimates have been downgraded by -51.4% and are expected to fall -51% YoY to $0.17 per share. FY23 earnings have been revised lower by -61.5% and are projected to decline -70% YoY to $0.51 per share.

Sales forecasts aren’t promising either. Current quarter sales are expected to fall -11.6% YoY to $420.4 million, while FY23 sales are expected to fall -7.9% YoY to $1.44 billion.

(Click on image to enlarge)

Image Source: Zacks Investment Research

During the most recent quarterly earnings call executives highlighted the numerous challenging developments at Leslie’s. CEO Michael Egeck noted “it was a difficult quarter,” and that “low double-digit traffic declines resulted in a 12% comparable sales decline and a 9% total sales decline.”

Additionally, on the call, he pointed to three primary factors challenging LESL’s business performance – weather, consumer price sensitivity, and leftover pool chemicals from the prior year. That price sensitivity is the inflation effect we noted, and a surplus of pool chemicals is the spending that was pulled forward immediately following Covid.

Hopefully, the business can eventually recover from these effects, however for now it makes the stock rather unappealing.

Valuation

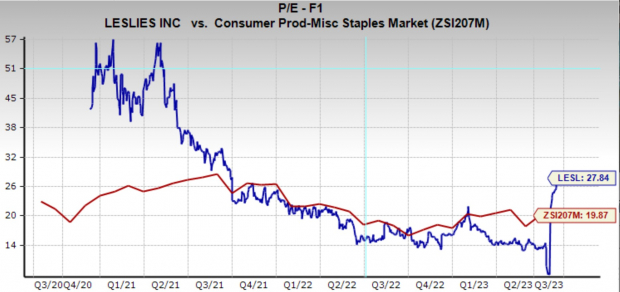

For a stock with falling business expectations, Leslie’s trades at a rather high valuation. Today it is trading at a one year forward earnings multiple of 27.8x, which is above the industry average of 19.9x, and above its three-year median of 20.8x.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Bottom Line

While Leslie’s has a long history of contributing to the pool industry, the near-term headwinds make the stock hard to invest in. Investors will want to wait for pool-related spending to normalize, and earnings revisions to begin trending higher before considering getting involved in the stock.

More By This Author:

Bull Of The Day: StoneX GroupWalt Disney Beats Q3 Earnings Estimates

3 High-Yield Bond Funds to Buy for Great Returns

Comments

Log in or sign up to join the conversation.