Advance Auto Parts (AAP) provides automotive replacement parts, accessories, batteries, and maintenance items for domestic and imported cars, vans, utility vehicles, and trucks. The company offers a variety of products such as brakes and brake pads, engines and related parts, antifreeze and washer fluids, wiper blades, and tire repair accessories.

Furthermore, Advance Auto Parts provides services such as battery installation, electrical system testing, and engine light scanning. The company serves do-it-yourself customers and professional installers through its website as well as retail stores in the United States, the U.S. Virgin Islands, Canada, and throughout the Caribbean.

The Zacks Rundown

Advance Auto Parts, a Zacks Rank #5 (Strong Sell), is a component of the Zacks Automotive – Retail and Wholesale – Parts industry group, which ranks in the bottom 12% out of more than 250 Zacks Ranked Industries. As such, we expect this industry group as a whole to underperform the market over the next 3 to 6 months, just as it has over the course of the year:

(Click on image to enlarge)

Image Source: Zacks Investment Research

Candidates in the bottom tiers of industries can often be solid potential short candidates. While individual stocks have the ability to outperform even when included in a poorly-performing industry group, the inclusion in a weaker group serves as a headwind for any potential rallies and the journey forward is that much more difficult.

Despite the underperformance this year, stocks in this group remain relatively overvalued:

(Click on image to enlarge)

Image Source: Zacks Investment Research

As a part of this group, AAP stock has experienced considerable volatility in 2023. Shares recently hit a 52-week low following a disappointing earnings report and represent a compelling short or hedge opportunity.

Recent Earnings Misses and Deteriorating Outlook

AAP has fallen short of earnings estimates in three of the last three quarters. The auto parts company most recently reported second-quarter earnings back in August of $1.43/share, missing the $1.72/share consensus EPS estimate by 16.86%. Earnings plunged 61.8% from the same quarter in the prior year.

Advance Auto Parts has missed earnings estimates by an average of 21.03% over the past four quarters. Consistently falling short of earnings estimates is a recipe for underperformance, and AAP is no exception.

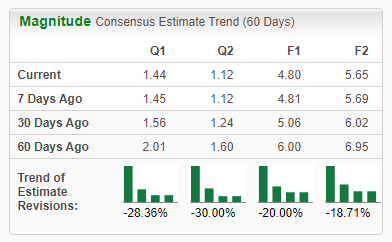

The company has been on the receiving end of negative earnings estimate revisions as of late. For the current quarter, analysts have decreased estimates by 28.36% in the past 60 days. The third-quarter Zacks Consensus EPS Estimate now stands at $1.44/share, translating to negative growth of -49.3% relative to the same quarter last year.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Falling earnings estimates are a huge red flag and need to be respected. Negative growth year-over-year is the type of trend that bears like to see.

Technical Outlook

As illustrated below, AAP stock is in a sustained downtrend. Notice how shares have plunged below both the 50-day and 200-day moving averages signaled by the blue and red lines, respectively. The stock is making a series of lower lows, with no respite from the selling in sight. Also note how both moving averages have rolled over and are sloping down – another good sign for the bears.

(Click on image to enlarge)

Image Source: StockCharts

While not the most accurate indicator, AAP stock has also experienced what is known as a ‘death cross’, wherein the stock’s 50-day moving average crosses below its 200-day moving average. Advance Auto Parts would have to make a serious move to the upside and show increasing earnings estimate revisions to warrant taking any long positions in the stock. AAP shares have fallen more than 64% in the past year alone.

Final Thoughts

A deteriorating fundamental and technical backdrop show that this stock is not set to go into overdrive anytime soon. The fact that AAP stock is included in one of the worst-performing industry groups provides yet another headwind to a long list of concerns. A history of earnings misses will likely serve as a ceiling to any potential rallies, nurturing the stock’s downtrend.

Shares continue to experience substantial volatility and have widely underperformed this year. With negative earnings estimate revisions continuing to pile up, this stock should be avoided as there are plenty of better alternatives in the current market environment.

More By This Author:

Bull Of The Day: ACM ResearchPanasonic (PCRFY) Surges 39.6% YTD: Will the Uptrend Continue?

Carnival (CCL) Q3 Earnings & Revenues Top Estimates, Rise Y/Y

Comments

Log in or sign up to join the conversation.