Image Source: Unsplash

After Amazon (AMZN) and Facebook (META) reported blowout earnings, sending their stocks up double digits after hours and soothing the bitter taste left from the recent disappointing earnings from MSFT, TSLA, and GOOGL, everyone was looking at the last Mag 7 of them all, the (formerly?) biggest company in the world, Apple (AAPL) which however left a bit to be desired, because while the iPhone maker reported both revenue and EPS which beat (iPhone sales actually beat this time while Mac, iPad, and Wearables all missed), the company's Greater China revenue disappointed, coming in below estimates, with Service revenues also disappointing.

Here is what the company reported for fiscal Q1:

- EPS $2.18 vs. $1.88 y/y, beating estimates of $2.11

- Revenue $119.58 billion, +2.1% y/y, beating estimates of $117.97 billion

- Products revenue $96.46 billion vs. $96.39 billion y/y, beating estimates of $95.14 billion

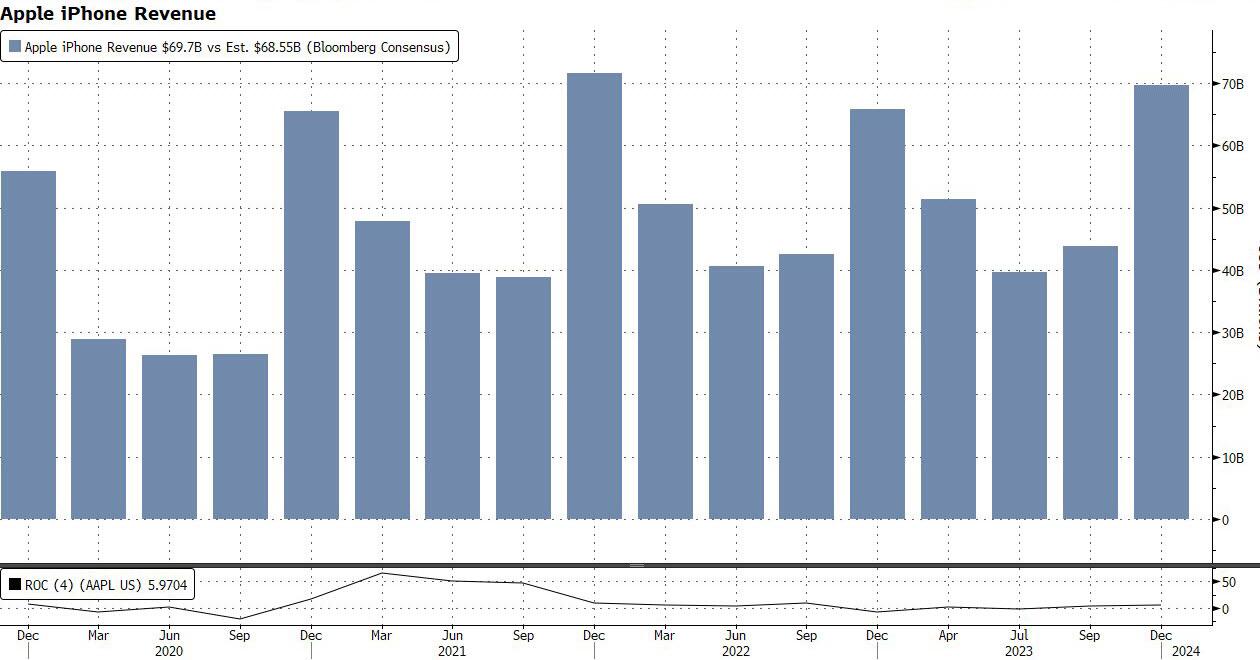

- IPhone revenue $69.70 billion, +6% y/y, beating estimates of $68.55 billion

- Mac revenue $7.78 billion, +0.6% y/y, missing estimates of $7.9 billion

- IPad revenue $7.02 billion, -25% y/y, missing estimates of $7.06 billion

- Wearables, home and accessories $11.95 billion, -11% y/y, missing estimates of $12.02 billion

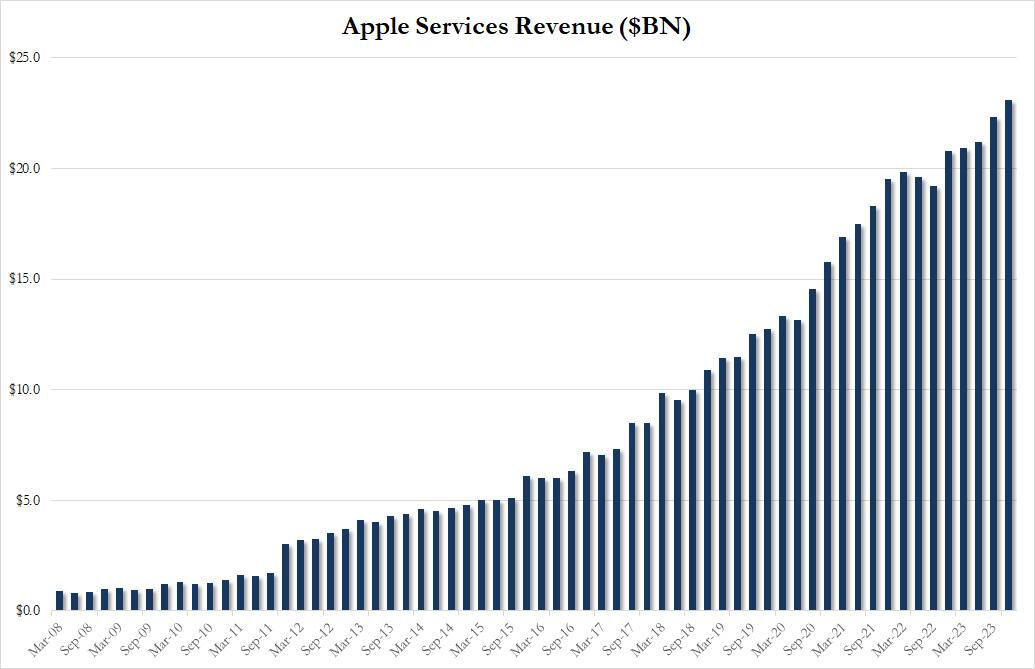

- Service revenue $23.12 billion, +11% y/y, missing estimates of $23.37 billion

- Greater China rev. $20.82 billion, -13% y/y, missing estimates of $23.5 billion

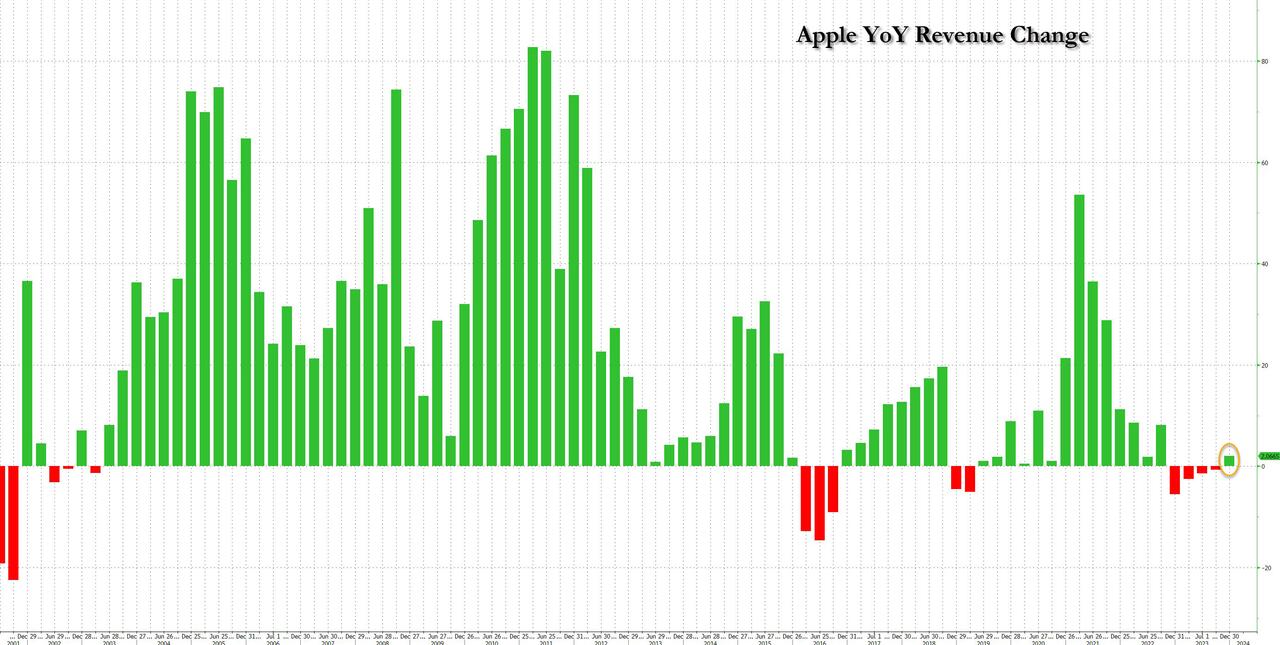

- While Revenue of nearly $120BN finally grew from a year ago, ending a period of 4 quarters of decline, it was still down from two years prior.

- Gross margin $54.86 billion, +9% y/y, beating estimates of $53.56 billion

- Cash and cash equivalents $40.76 billion, above estimates of $38.81 billion

While the numbers were mixed, the good news is that AAPL managed to avoid a 5th consecutive quarter of annual revenue declines (it would have been the first time since the company's existential crisis in the 1990s).

Commenting on the quarter, CEO Tim Cook said “Today Apple is reporting revenue growth for the December quarter fueled by iPhone sales, and an all-time revenue record in Services. We are pleased to announce that our installed base of active devices has now surpassed 2.2 billion, reaching an all-time high across all products and geographic segments. And as customers begin to experience the incredible Apple Vision Pro tomorrow, we are as committed as ever to the pursuit of groundbreaking innovation — in line with our values and on behalf of our customers.”

CFO Luca Maestri chimed in that “our December quarter top-line performance combined with margin expansion drove an all-time record EPS of $2.18, up 16 percent from last year. During the quarter, we generated nearly $40 billion of operating cash flow and returned almost $27 billion to our shareholders. We are confident in our future, and continue to make significant investments across our business to support our long-term growth plans.”

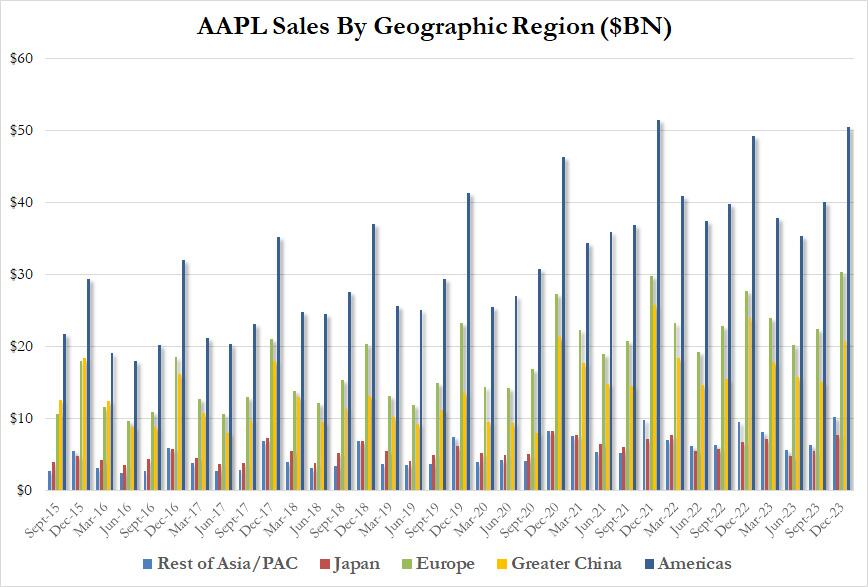

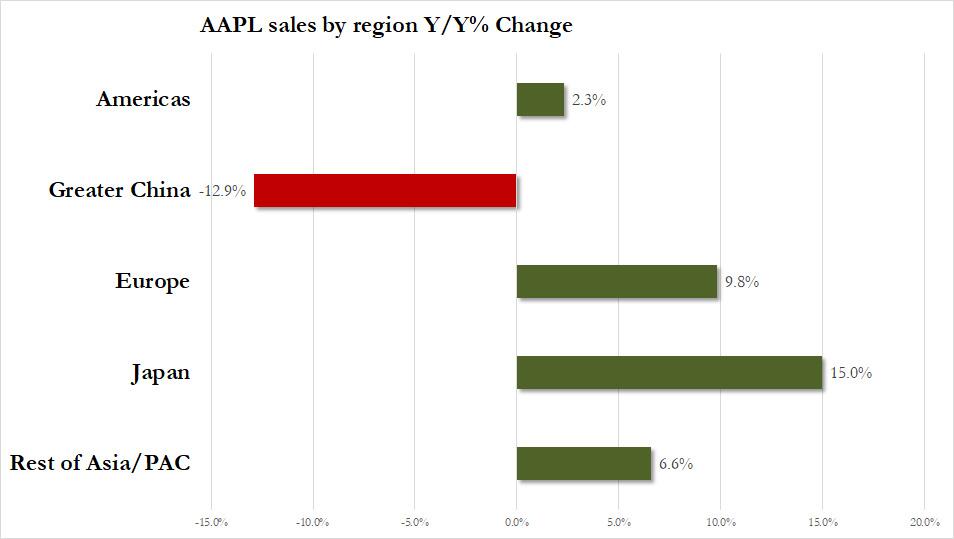

Despite the optimistic rhetoric, the rumors about the company's weakness in China turned out to be true, and revenues there missed estimates of $23.5BN badly, the company generating just $20.82BN in sales in what until recently was the biggest growth market, confirming action by Beijing to shun the western cell phone. Here is the geographic breakdown of Apple's sales...

... and here is the YoY change. China's 13% drop sticks out like a sore thumb.

This shouldn't be a surprise: for months, Apple watchers have been beating the drum that the iPhone is underperforming in China, citing strong growth by rivals like Huawei, Xiaomi, and others, combined with some government agencies banning the use of the device at work. Apple pushed back considerably on its last earnings call against that idea, but it turns out it was lying. Today, we learned that sales in China actually fell nearly $3 billion in the critical holiday quarter. That’s the lowest China 1Q revenue for Apple since 2020!

CFO Luca Maestri had this to say about the plunge in China: “There is a decline. We are not happy with the decline but we know China is the most competitive market in the world...We continue to see significant opportunity for us in China in the long term.”

Judging by the move in AAPL stock after hours, the market disagrees.

Turning to revenue by product category, iPhones beat, and... that was it: all other categories disappointed:

- IPhone revenue $69.70 billion, +6% y/y, beating estimates of $68.55 billion

- Mac revenue $7.78 billion, +0.6% y/y, missing estimates of $7.9 billion

- IPad revenue $7.02 billion, -25% y/y, missing estimates of $7.06 billion

- Wearables, home and accessories $11.95 billion, -11% y/y, missing estimates of $12.02 billion

While it is notable that the iPhone 15 grew, the context is critical - the iPhone 14 Pro before it slumped considerably because of supply-chain hiccups in China (i.e. base effect). That issue wasn’t replicated this year, plus the iPhone 15 Pro was a much bigger update. Still, the pick-up in iPhone revenues was at best modest as the chart below shows.

Mac revenue was the biggest product miss (revenue was -1.6% or so off of estimates). Computer sales have been challenged for over a year now as consumers were increasingly cost-sensitive, and many had already bought new computers during the pandemic. Industry analyst IDC expects 2024 to bring long-awaited growth in computer sales.

Commenting on the disappointing results, Tim Cook said the decrease in Wearables, Home and Accessories was due to a difficult comparison to new products released in 2022. That included the first Apple Watch Ultra and a new Apple TV. The 2023 updates in the category were minor -- and Apple dealt with a few days of halted sales in the US due to the patent fight with Masimo Corp.

And then there was service revenues, which despite rising to a new all-time high of $23.1BN (up 11.3%) missed estimates of $23.4BN.

Still, according to CFO Luca Maestri, Apple has well over one billion paid subscriptions, more than double what it had four years ago, across its ecosystem (this includes first and third-party subscriptions).

Putting it all together, despite the solid iPhone results and profit beat, investors are disappointed by the China numbers, with the stock falling as much as around 4% so far after-hours, the loss accelerating during the call when the company said that during the March quarter, it expected total and iPhone revenue to be similar to previous years when factoring in that 2Q revenue last year came in about $5 billion higher due to certain conditions (i.e., inventory replenishment). The company also expects gross margins between 46%-47% for Q2, as well as operating expenses of $14.3BN-$14.5BN, and expects service business the show double-digit growth similar to the current quarter. Finally, CFO Maestri said services in the March quarter will be negatively impacted by foreign exchange rates and that comparisons for the March quarter are more challenging than in other quarters (translation: take last Q2 and slash $5BN due to "pent up" demand for iPhone in the March 2023 quarter which obviously won't be here this time).

Not surprisingly, AAPL's stock is doing the worst of all the mega techs reporting today, with both AMZN and META surging after their respective reports, and only AAPL sliding.

More By This Author:

Amazon Soars After Beating Estimates, AWS Profit Impresses, Guides Higher

Initial & Continuing Jobless Claims Surge As Layoffs Accelerate

Hawkish Fed Hammers Dovish Market: No Cuts Imminent, Removes 'Banking System Soundness' Comment

Comments

Log in or sign up to join the conversation.