Image Source: Unsplash

With The Magnificent 7 stocks getting clubbed in recent days after disappointing earnings from TSLA and GOOGL and meh results from MSFT, hope was high that Amazon (AMZN) could save the world. So here's the good news: a top- and bottom-line beat, and despite some weakness in AWS revenues (which came in just below estimates) the stock is surging after hours.

Here is what Amazon reported for Q4:

- EPS $1.00 vs. 94c q/q, beating estimates 78c

- Net sales $169.96 billion, +14% y/y, beating estimates of $166.21 billion

- Online stores net sales $70.54 billion, +9.3% y/y, beating estimate $68.91 billion

- Physical Stores net sales $5.15 billion, +3.9% y/y, missing estimates of $5.23 billion

- Third-Party Seller Services net sales $43.56 billion, +20% y/y, beating estimates of $41.96 billion

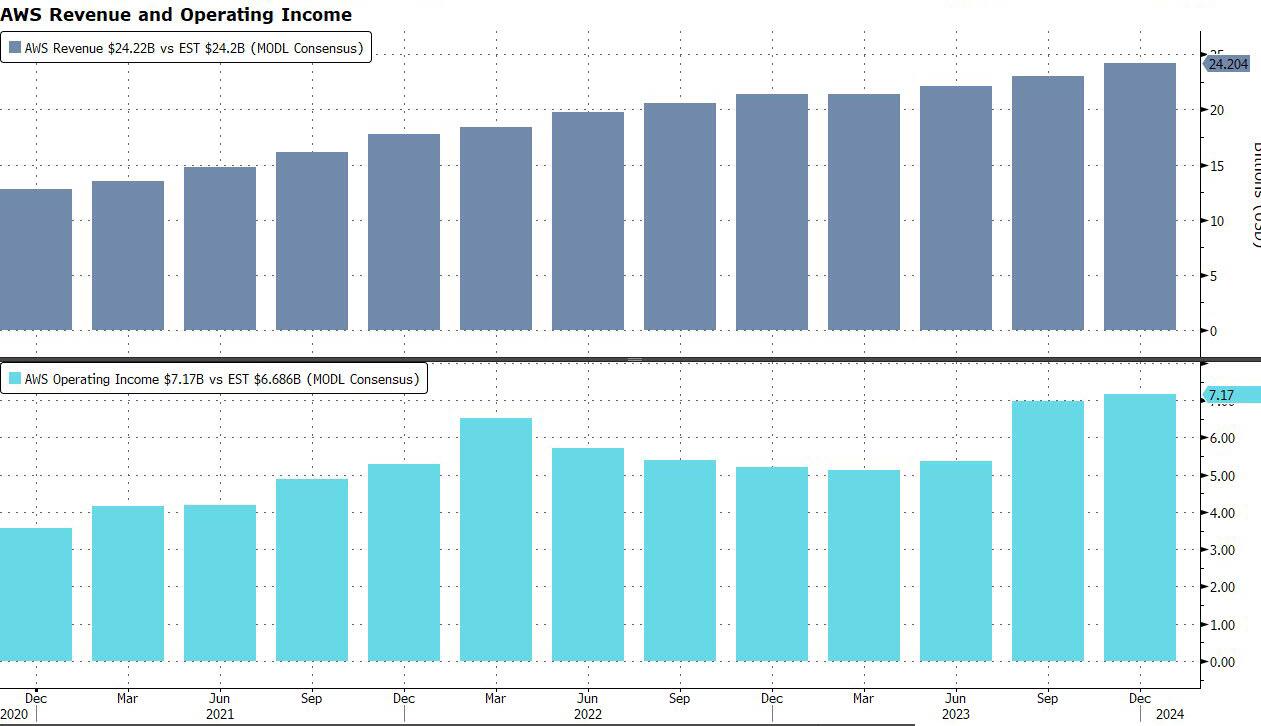

- AWS net sales $24.20 billion, +13% y/y, missing estimates of $24.22 billion

- North America net sales $105.51 billion, +13% y/y, beating estimates of $102.88 billion

- International net sales $40.24 billion, +17% y/y, beating estimates of $38.96 billion

- Third-party seller services net sales excluding F/X +19% vs. +24% y/y, beating estimates of +15.9%

- Amazon Web Services net sales excluding F/X +13% vs. +20% y/y, beating estimates of +11.8%

- Operating income $13.21 billion vs. $2.74 billion y/y, beating estimates of $10.49 billion

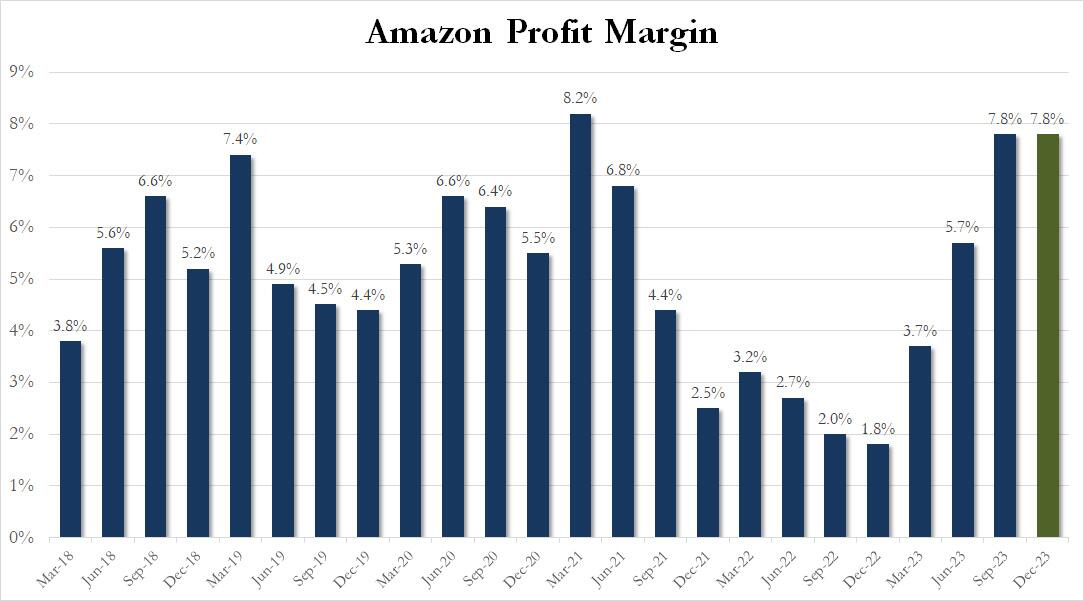

- Operating margin 7.8% vs. 1.8% y/y, beating estimates of 6.17%

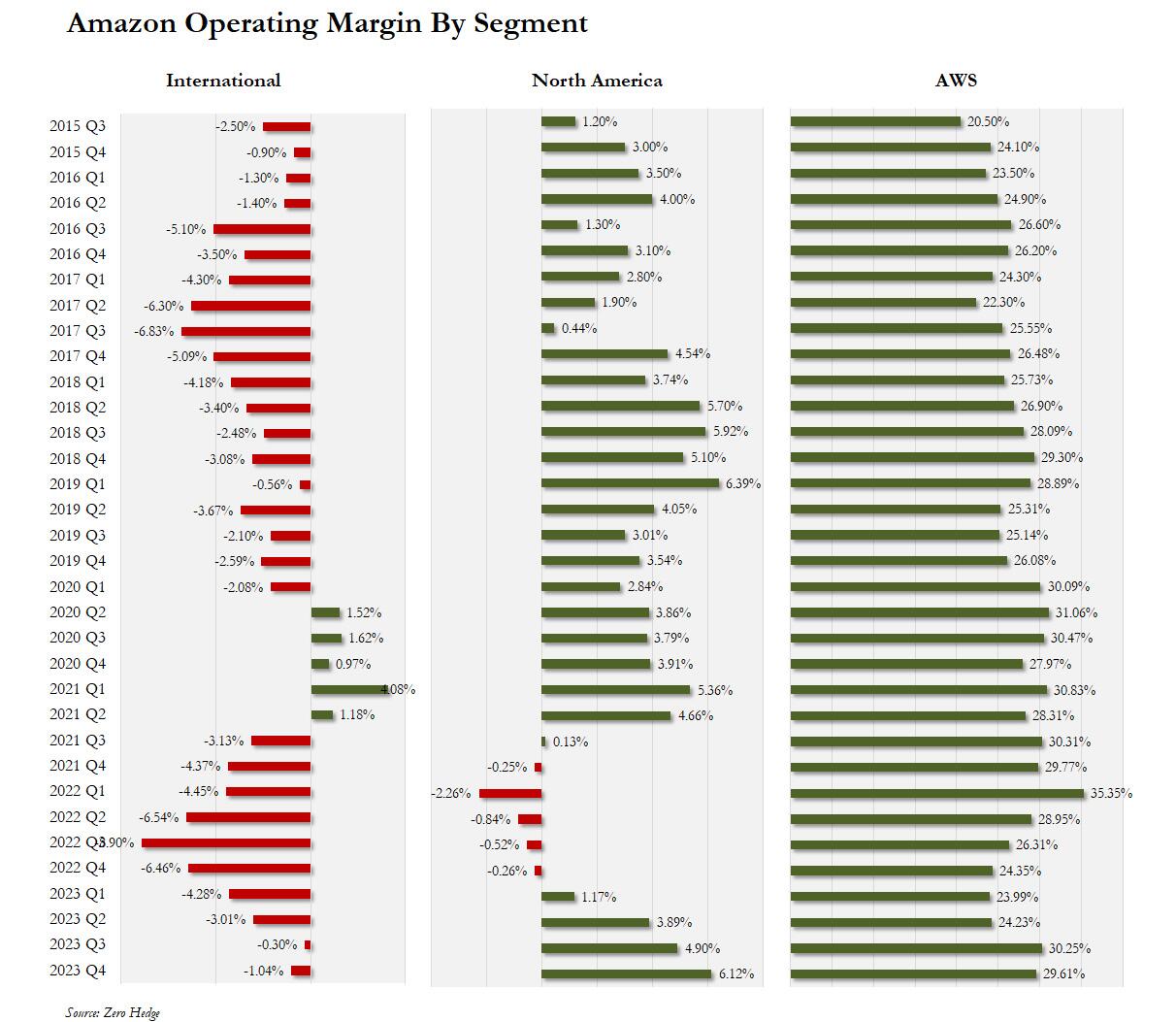

- North America operating margin +6.1% vs. -0.3% y/y, beating estimates +4.12%

- International operating margin -1% vs. -6.5% y/y, beating estimates -1.27%

- Fulfillment expense $26.10 billion, +13% y/y, beating estimates of $25.2 billion

- Seller unit mix 61% vs. 59% y/y, estimate 59.5%

Q1 Guidance:

- Revenue between $138.0 billion and $143.5 billion, or up 8% and 13%; The median consensus estimate was $142BN so the upper end is stronger if not the lower or average.

- Operating Income between $8.0 billion and $12.0 billion, also beating the Wall Street estimate of $9.1 billion.

Bottom line: the company beats expectations on both revenue ($169 billion), EPS ($1.00 vs 78c), and operating income ($13.2 billion). Amazon Web Services, the company’s profit driver, posted revenue in line with analyst estimates, but investors are likely to be heartened by much higher-than-expected operating income from the cloud division.

(Click on image to enlarge)

Commenting on the quarter, CEO Andy Jassy said that "what we’re most pleased with is the continued invention and customer experience improvements across our businesses. The regionalization of our U.S. fulfillment network led to our fastest-ever delivery speeds for Prime members while also lowering our cost to serve." As for AWS, the "continued long-term focus on customers and feature delivery, coupled with new genAI capabilities like Bedrock, Q, and Trainium have resonated with customers and are starting to be reflected in our overall results." Also Amazon's Advertising services "continue to improve and drive positive results."

Taking a closer look at profits, it was a bit of a mixed bag, with AWS reporting profit margins which dipped modestly to 29.61% from 30.23% in the previous quarter, if solidly ahead of the 24.33% reported a year ago and also beating estimates (thus offsetting the negative taste from weakness in revenue growth which disappointed modestly). As for the retail operations, North America margins posted a solid improvement, rising to 6.1% from -0.3% a year ago, and beating estimates of 4.1%, while International margins dipped modestly to -1.0% from -0.3% a quarter ago, but better than that -1.3% expected.

(Click on image to enlarge)

As Valoir Analyst Rebecca Wettemann writes in a note after earnings, with AWS’s lead in traditional cloud infrastructure fading, its ability to compete against Microsoft and Google in offering AI services is a critical consideration for investors. As such, she’ll be watching for how Amazon speaks about customer growth in Bedrock, a service that allows AWS customers to tap into large language models.

Combining the modest drop in AWS and international margins with the continued improvement in North America means that the blended profit margin remained at 7.8%, the highest since early 2021.

(Click on image to enlarge)

And speaking of profit, CEO Andy Jassy is keeping a tight hold on expenses. Spending on marketing and sales was basically flat. General and administrative expenses fell by about 10%. And technology and content spending -- which includes salaries for software developers as well as servers and other hardware -- rose just 6%, down from 38% growth entering this year.

Also of note: during the last year, Amazon laid off about 27,000 corporate employees. Cuts have continued in 2024, if more quietly, falling on entertainment subsidiaries and its studios business. CFO Olsavsky said that “I don’t see it as a year of efficiency type thing. It’s more we are going to continue to be careful on what we invest in,” holding the line on headcount in some areas while continuing to invest in others.

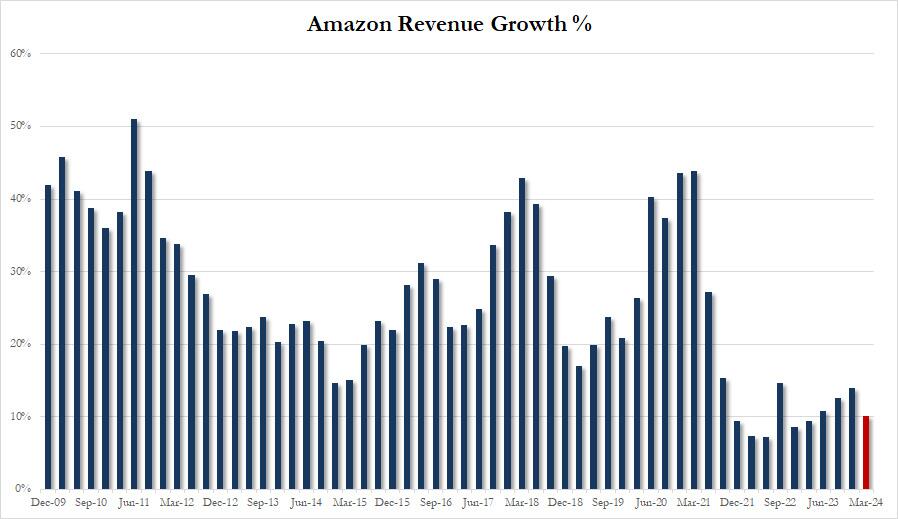

Looking at the company's guidance, Amazon expects revenues to be between $138.0 billion and $143.5 billion, or to grow between 8% and 13% compared with first quarter 2023. Taking the average of the range suggests revenue growth just around 10% YoY, which while solid, would be the lowest in the past year. Then again the company has a history of sandbagging results so investors will likely ignore this.

(Click on image to enlarge)

Amazon also said that operating income is expected to be between $8.0 billion and $12.0 billion, compared with $4.8 billion in first quarter 2023, and stronger than the Wall Street estimate of $9.12BN.

“The bottom line is that despite all the concerns plaguing the tech sector, Amazon has managed to perform surprisingly well,” said Jesse Cohen, a senior analyst at Investing.com. “The results indicate that ongoing cost-cutting measures are having a positive impact on Amazon’s business prospects.”

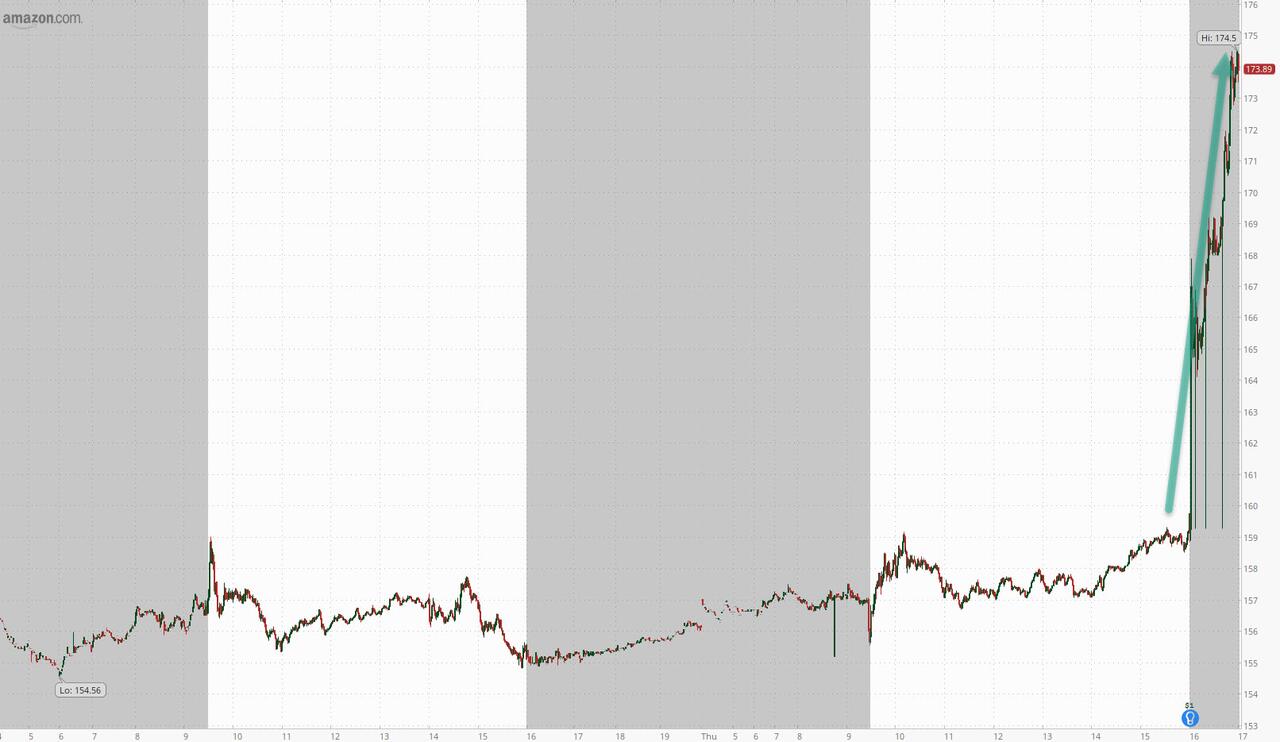

The cheerful view was clearly shared by the street, with Amazon stock soaring about 10% after hours to $174 after closing at $155 yesterday, and not far from the company's record high of $188.65 hit in the summer of 2021.

(Click on image to enlarge)

More By This Author:

Initial & Continuing Jobless Claims Surge As Layoffs AccelerateHawkish Fed Hammers Dovish Market: No Cuts Imminent, Removes 'Banking System Soundness' Comment

ADP Employment Report Job Gains Slowing

Comments

Log in or sign up to join the conversation.