Image Source: Unsplash

Apple (AAPL - Free Report), the unequivocal king of the stock market reports earnings Thursday, May 4 after the market closes. As the world’s leading consumer products and technology company, Apple’s earnings act as an important bellwether for the broader economy.

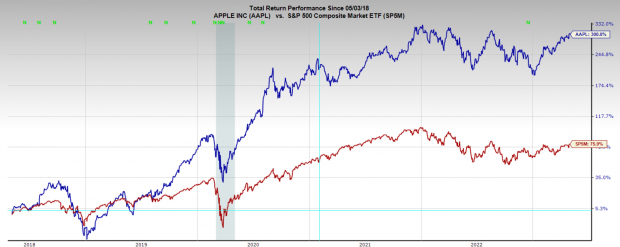

Apple stock has not disappointed this year and the sturdiness of Apple’s returns simply cannot be understated. The stock is up 30% YTD, 300% over the last five years, and 1100% over the last 10 years. It isn’t flawless though, as it was down -30% during 2022. However, it has nearly earned it all back in the first four months of 2023.

Image Source: Zacks Investment Research

Earnings Expectations

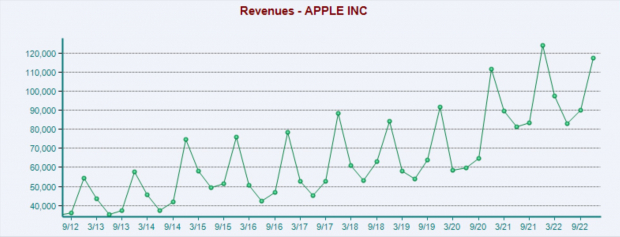

Analysts are expecting a YoY decline in Q2 sales, which isn’t great, but also not terrible. Something I don’t often see mentioned about Apple is the strong seasonal tendencies of its revenues.

In the quarterly revenues chart below we see revenues regularly explode higher following the holiday season and are then mostly stagnant through the rest of the year. But Q1 2023 sales were below Q1 2022, which shows that there was a YoY slowdown in the most recent holiday season.

Image Source: Zacks Investment Research

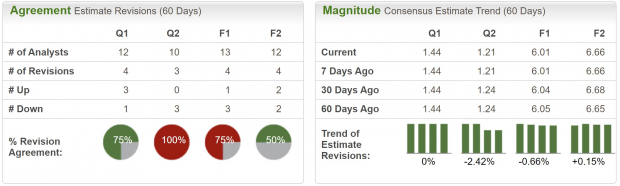

Additionally, analyst earnings revisions have been mixed, which gives Apple a Zacks Rank of #3 (Hold). Q2 expectations are looking down a bit, which lines up with market expectations of a broader economic slowdown in the second half of the year.

Also concerning, last quarter Apple posted a rare sales and earnings miss. Last quarter marked Apple’s first earnings miss since 2016, which was just -$0.01 below expectations and its second sales miss since 2016, which was also just below expectations.

Image Source: Zacks Investment Research

Analysts are expecting earnings growth to decline -5.3% YoY to $1.44 a share. The rest of the year is expected to be mostly flat as well, however next year’s earnings are projected to pick up significantly.

Image Source: Zacks Investment Research

Bear Case

Shorting Apple is almost never advised, and although I don’t consider this my base case it is important to address the primary risks. AAPL stock has acted as an incredible haven this year and its returns make up 25% of S&P 500’s total returns YTD.

At this point investors are treating Apple stock like a Treasury bond, and it has considerably outperformed Treasuries. But is that realistic? Will some doubt start creeping into investors’ minds and cause Apple to roll over.

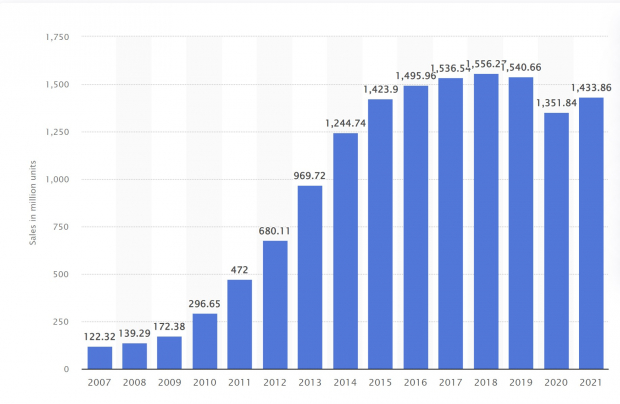

Apple’s most critical profit center is the iPhone, which makes up 52% of total revenue. In the Q1 report, we saw that iPhone sales were down YoY. Management chalked this up to a one-time event and blamed the miss on supply issues related to the lockdowns in China.

What if it was a demand issue though? What if we are moving past peak iPhone? The chart below shows total annual smartphone sales, which have clearly peaked. This means that Apple is already fighting an uphill battle.

Furthermore, iPhone quality and longevity is improving, and so are prices, and the length of payment plans. I know personally, the iPhone 11 Pro I bought in 2019 still feels as good as new.

Image Source: Statista

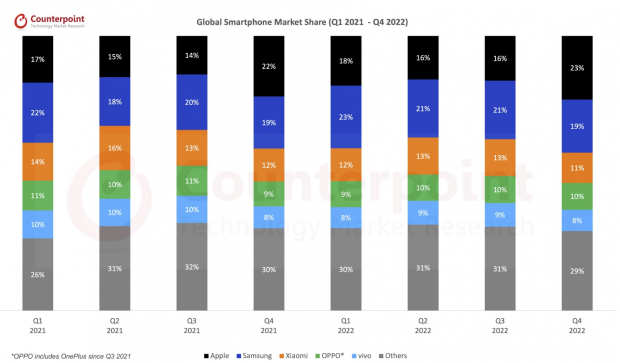

Market share is another important consideration. Apple currently has an impressive 23% market share of global smartphones. How much room does Apple have to continue to grow this figure?

The massive Chinese middle class is a very important segment for Apple to target, but what if they start to prefer the Chinese branded phones? Oppo and Xiaomi have made some extremely compelling new phones, particularly their smart flip phones. Flip phones are extremely interesting because they begin to blend phone and tablet products. Flip phones are a product Apple doesn’t have and I haven’t heard rumors of anything in the pipeline.

Image Source: Counterpoint

The black swan event would be a military conflict between the US and China. In this worst case scenario, it would be highly unlikely that the civil relations between Apple and China continue.

The concerns listed are more hypotheticals and questions. Of course, Apple has defied all investor logic for over a decade now, and its downfall is an extremely unlikely event. But doubt and fear can move a stock. Is the next 20% move in Apple stock higher or lower? I don’t know, but there are certainly catalysts the give potential to the -20% possibility.

Technicals

There isn’t a clean chart pattern to trade AAPL from, but this large range looks significant to me. The $180 level is resistance and $130 support. Right now, price is in no-mans land in the middle of this large range.

If price can clear the $180 level, resistance should turn into support, and the next multi-year leg higher in Apple should commence. However, a rejection at $180 would be very significant. If the stock can’t clear that level, it may be indicative of not just Apple, but the market more broadly.

With a recession likely coming later this year, it is possible we will see Apple retest the high of the range, and then as the recession takes hold, swing back down to the bottom of the range. Rather than trying to short the stock, investors would be better off waiting for price to come back down to the $130-$140 buy zone.

Image Source: TradingView

Valuation

Apple is currently trading at a one-year forward earnings multiple of 28x, which is above the market average and above its five-year median of 24x. This certainly isn’t a cheap valuation, but as one of the world’s leading companies it isn’t particularly expensive either. This reasonable valuation doesn’t play well for the bears.

Image Source: Zacks Investment Research

Bottom Line

Apple is a juggernaut in the stock market, and its supremacy is undeniable. While I did lay out a bear case, it is more of an exercise in risk management than anything else. While the dynamics that have propelled Apple to this level over the past decade may change, the biggest risk currently is an economic slowdown.

Apple brought luxury to the masses, so if the average person begins to feel the heat of a slowing economy, they probably won’t be buying a new iPhone. But there is a path where the recession is not too bad, and in that case, Apple continues to chug along as the world’s leading stock.

More By This Author:

Yum Brands Q1 Earnings Miss Estimates

Starbucks Q2 Earnings And Revenues Beat Estimates

Pfizer Tops Q1 Earnings And Revenue Estimates

Comments

Log in or sign up to join the conversation.