AppHarvest (APPH) is an AgTech company that aims to build a resilient food system for America through the construction and operation of large-scale and high-tech greenhouses.

As many investors are not familiar with the agriculture business I will lay out the case for its importance and the urgency for its development.

Problems of the Agriculture Industry

Roughly 69% of all vine crops (e.g. tomatoes, cucumbers & peppers) consumed in the US are imported.

Figure 1: Imports of Vine Crops

Source: Investor Presentation APPH

The exporting companies use high amounts of water and pesticides in the process of growing vine crops. This has negative effects on the health of consumers and the environment. Additionally, many vegetables and fruits are transported with semi-trucks from Middle & South America to the USA. Not only is this connected to the large consumption of diesel but also to the need to transport unripe fruits. Consequently, the consumer receives low-quality food. Moreover, the demand for fresh produce is not going to decrease anytime soon. The UN forecasted the food consumption by 2050 to be 70% higher than today. And, thus, there is an even bigger urgency to grow food in the US under environmentally friendly conditions.

What is the solution?

APPH wants to solve the above-mentioned problems with high-tech greenhouses.

Figure 2: Morehead Facility in Kentucky

Figure 2 shows the sheer size (60 acres) of AppHarvests' first operational facility. The other astonishing factor, besides the size, is the use of technology in this facility. APPH required Root AI, a company that builds harvesting robots equipped with image recognition software to distinguish between ripe and unripe fruits and vegetables (see figure 3).

Figure 3: Image Recognition of Root AI

Source: Root AI Youtube

Figure 4: Harvesting Robot

APPH is monitoring all plants with sensors to ensure perfect growing conditions. By doing this they know exactly when their plants need water, light or where pests are spreading in the greenhouse. As a result, APPH can reduce the use of water by 90% in comparison to traditional farming. The water used by APPH is solely rainwater that was locally captured and stored in 10-acre big rainwater retention ponds. To have a sufficient water supply, APPH is based in Kentucky, which is the 12th wettest state in the US and has, therefore, more than enough rainwater for APPHs' current and future facilities. However, Kentucky has further advantages. It is located centrally in the USA which makes it possible to reach 70% of the population within one day. Furthermore, Kentucky has a poverty rate of 18.3%. Accordingly, it is the state with the 4th highest rate in the USA. This is because Kentucky formerly relied heavily on the coal industry which is now shrinking rapidly. Hence, APPH shoots for filling this gap by building a range of different facilities in the state and therefore creating new jobs for Kentuckians.

Many companies highlight similar aspects to market their stock to investors. Often this is mostly greenwashing and there is no real motivation behind it. I don’t believe this is the case for APPH. This is because the CEO Jonathan Webb is born and raised in Kentucky, which is the reason why he took it as his goal to transform Kentucky into an AgTech hub. To get an idea of the CEOs passion I recommend you to watch this video.

What you told me sounds great, but I want to see more numbers!

Figure 5: Impact of AppHarvest

Source: Investor Presentation APPH

Through the innovations and strategies mentioned above, APPH achieves 30 times higher yield than open-field agriculture and uses 80% less diesel for transportation. Also, the business model of APPH results in a contribution to many different sustainable development goals, from decreasing poverty to a much more responsible consumption and production. Due to this, APPH is one of the only publicly traded B Corps in America.

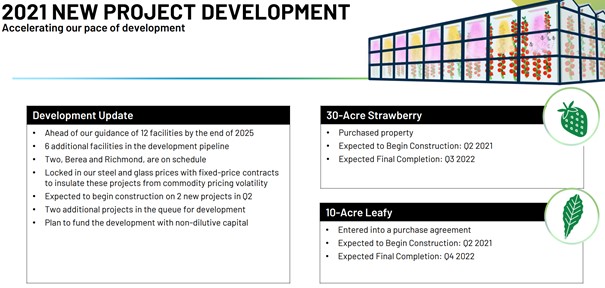

For now, the company just started operating, and accordingly, their current revenue figures are very small. They guided for revenue of $20M to $25M in 2021. Measured on the current market cap of $1.7bn this translates roughly into a 76 price-to-sales ratio. Keep in mind that their first facility just started production and it takes some time to have it running at full capacity. Besides, this is just the starting point. APPH aims to have 12 facilities running by the end of 2025. What is striking to me is that APPH may just have started but they seem to have the blueprint for rapidly building the machine that creates healthy food. So far APPH is only growing tomatoes. But the construction of two new facilities will start in Q2 of 2021. One is a 30-acre facility for strawberries and the other one a 10-acre facility for leafy crops (see figure 6).

Figure 6: AppHarvest Can More Than Tomatoes

Source: 2021 Q1 Earnings Presentation

In case you are wondering what leafy crops are; Leafy crops are e.g. spinach, iceberg, leaf lettuce, or romaine. Besides the already mentioned projects, APPH already did the groundbreaking for a 60-acre tomato facility in Richmond and a 15-acre leafy crop facility in Berea.

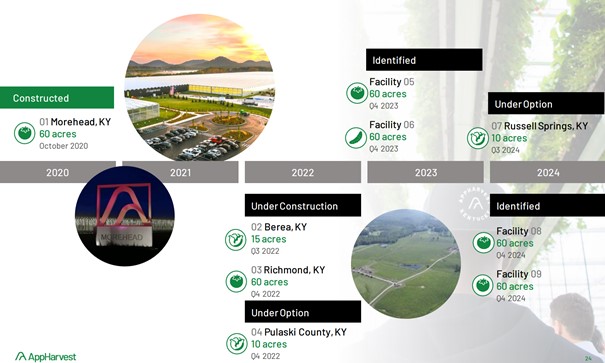

Figure 7: AppHarvests' Facility Pipeline

(Click on image to enlarge)

Source: Investor Presentation APPH

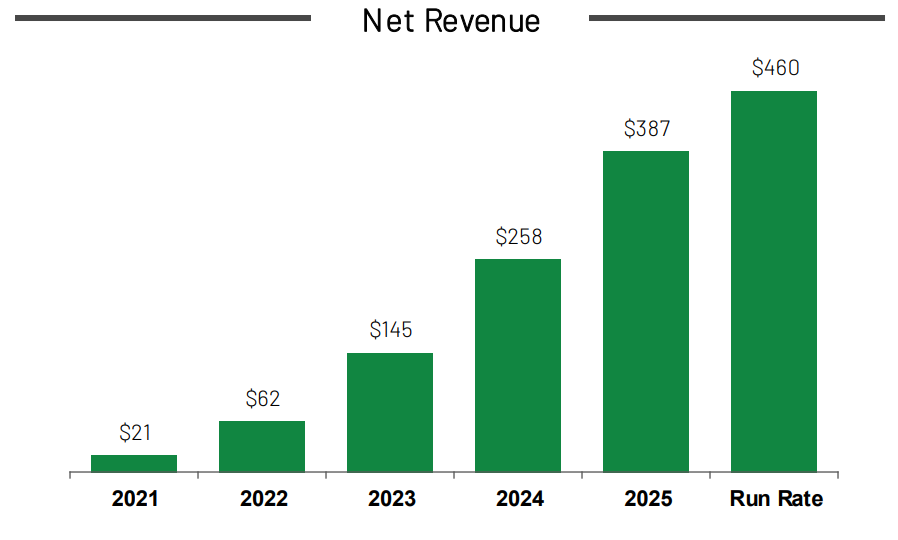

The pipeline shown in figure 7 does not include the recently announced projects in figure 6. This is because it is from the investor presentation that was held before Q1. However, the pipeline highlights how ambitiously APPH is. The announcement of the two new facilities in their Q1 earnings further stresses the pace APPH is executing with. It also indicates that APPH is ahead of its ambitious goals. The expected revenue figures by APPH are shown in figure 8.

Figure 8: Forecasted Revenues

Source: Investor Presentation APPH

So, we know that the company will grow its revenues rapidly but what about profitability?

Normally, the expected gross margin in agriculture is roughly between 10% and 15% and therefore rather low. This is not the case for APPH. Due to the strong technology focus, the company expects a gross margin of 40%. To see if this figure is realistic I looked at the expected numbers of their competitor Aerofarms. Aerofarms forecasted an even higher gross margin of 51% for the end of 2026. Hence, the 40% stated by APPH could be realistic. In the long-term, this could lead to a net margin of 20% or more because their operating expenses should be relatively low going forward. However, given their aggressive growth plans, it is unlikely that they will be profitable measured by net income anytime soon. Still, just to show what would be possible we take the $460 run rate at the end of 2025 and multiply it with 0.2 to come up with a potential net income. The result would be $92M in net income. Given the market cap would still be at $1.7bn this would result in a PE ratio of 18. Take all these calculations with a grain of salt as a lot of guesswork is involved. Furthermore, one needs to keep in mind that this company will still grow fast by 2026 and beyond which would justify a much higher PE ratio. Another essential question remains. Is the TAM big enough to support this growth?

TAM of Fresh Produce in the USA

The fresh produce market in the US currently generates $55bn yearly. This amounts to $170 per person. Compared to some developed European countries, this number is relatively small. For example, Germany and Sweden have roughly $300 in revenue per person. When assuming that Americans get more aware of the benefits of a balanced diet the American fresh produce market should increase over time. Accordingly, I expect the US to have similar revenue figures per person like Europe. The result is that the TAM of APPH could increase to $100bn per year. Therefore, there is some runway for APPHs' future revenues. However, their TAM is just centered in the US. I also do not see them expanding to other countries anytime soon as this would contradict their vision. To be a good investment APPH needs to capture a few percentages of the described TAM.

The Valuation

I used a discounted cash flow model to value APPH. I set the targeted operating margin by 2031 at 20%. Furthermore, I assumed the revenues of 2031 to be roughly $1.5bn. This reflects 1.5% of the TAM. For the cost of capital, I used 8% in the first years and gradually lowered it over time. The result is a fair value of $32 per share. As of today, the price is at $16.3 per share.

Conclusion

The company has a very honorable vision. It is one of the few investing opportunities with a great focus on environmental and social sustainability. The agriculture industry is ripe for disruption and the CEO, Jonathan Webb is a good fit to grow the business. Before founding APPH he was responsible for some of the biggest solar projects in America. This provides confidence that he knows how to optimize for energy efficiency of large-scale projects. Besides, Jonathan has a lot of skin in the game. He owns more than 18% of all outstanding shares.

Overall APPHs' future is very exciting and I will monitor them very closely going forward.

Comments

Log in or sign up to join the conversation.