Image: Bigstock

The market liked what it saw in the quarterly releases from JPMorgan (JPM - Free Report), Citigroup (C - Free Report), and even Wells Fargo (WFC - Free Report). There was plenty to like in these results, with higher interest rates helping these big players expand their margins while demand for loans remained strong, helping loan portfolios grow.

The bank worries that took center stage in the wake of the Silicon Valley Bank fiasco didn’t pertain to these big players. JPMorgan, Citi, and Wells Fargo, which reported Friday morning, and Bank of America, which is scheduled to report Tuesday morning (April 18), regularly go through the Fed’s stress tests and are perceived as very safe.

The diminished confidence in the banking space is specifically centered on the small- and mid-sized regional banks that will start reporting results this week. The flight to safety among depositors has forced these banks to offer much higher deposit rates to stem the tide.

This will show up in net-interest margin pressures relative not only to what came through from the likes of JPMorgan, Citi, and Wells Fargo, but also relative to what these same banks had reported in the preceding period.

Returning to the group’s Q1 results, the fact that the investment banking business was weak during the period was no surprise for the market. We knew that advisory fees would, at best, be about two-thirds of what they were in the year-earlier period, as tighter monetary policy and other macroeconomic headwinds have been weighing on deal-making.

JPMorgan’s net interest income jumped +49%, as average loans increased +5% and net-interest margin expanded to 2.63% from 1.67% in the year-earlier period. Margins expanded for Citigroup and Wells Fargo as well, as funding costs (the rates offered to depositors) didn’t go up by that much.

The market liked JPMorgan’s raised guidance for net interest income this year, though management has stated that 2023 will mark the high watermark on this count over the next few years.

Lending remained strong in Q1 but started to soften towards the end of the quarter in the wake of the Silicon Valley Bank failure, a trend that has carried into the current period and will likely remain a negative factor over the coming quarters as well.

Many in the market see the resulting tightening in financial conditions as reflected in the aforementioned diminished lending outlook becoming a significant growth headwind for the U.S. economy, which was already under severe strain due to the Fed’s extraordinary monetary policy tightening.

Partly driving the market’s favorable reaction to these big bank results is a sigh of relief in a way, which follows an almost indiscriminate sell-off for the group since early March when the Silicon Valley Bank issue took center stage.

The JPMorgan, Citigroup, and Wells Fargo results were undoubtedly good, but sentiment on the group had weakened so much that market participants found the results reassuring. Bank stocks had been leading the market this year through early March but have struggled since March 6, as the chart below shows.

Image Source: Zacks Investment Research

The issue with the bank stocks isn’t so much their current earnings power, but rather how their profitability will shape up in the coming economic slowdown. Bank investors are wary of the group’s track record of making a lot of money during the good times, which the group then gives back during the bad times.

The question is how ‘bad’ will the coming ‘bad times’ be for the economy, and what will that do to bank earnings.

Regarding the Finance sector scorecard for Q1, we now have results from 18.5% of the sector’s market capitalization in the S&P 500 index. Total earnings for these companies are up +25.3% from the same period last year on +17.3% higher revenues, with 83.3% beating EPS estimates and 100% beating revenue estimates.

Looking at the Finance sector as a whole, total Q1 earnings for the sector are expected to be up +4.2% on +7.7% higher revenues.

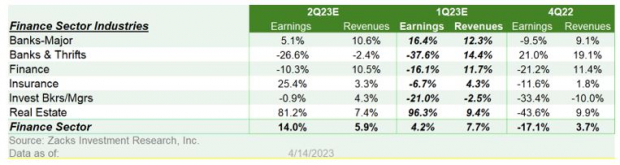

For the Zacks Major Banks industry, which includes all of the aforementioned banks and accounts for roughly 40% of total Finance sector earnings, total Q1 earnings are on track to be up +16.4% from the same period last year on +12.3% higher revenues.

The table below shows the sector’s Q1 earnings and revenue expectations at the ‘medium’ industry level in the context of what the space reported in the preceding period and what is expected in the following quarter.

Image Source: Zacks Investment Research

As noted earlier, skeptics of the banking industry argue that the group ends up giving away all the profits that it had accumulated during the good times when the macro environment turns south. The COVID-19 downturn was an anomaly in that respect, but there is some truth to the allegation.

We will see how the economic picture unfolds in the coming quarters, but the credit quality metrics in the reported Q1 results do not point toward any imminent deterioration.

The earnings growth picture for the Finance sector is expected to improve in 2023 as we turn the page on tough comparisons, even though the economic growth pace is expected to moderate under the cumulative weight of the Fed’s tightening. Finance sector earnings are expected to be up +11.3% in 2023 on -1.9% lower revenues, which would follow the -15.9% earnings decline on +7.7% higher revenues in 2022.

2023 Q1 Earnings Season Scorecard

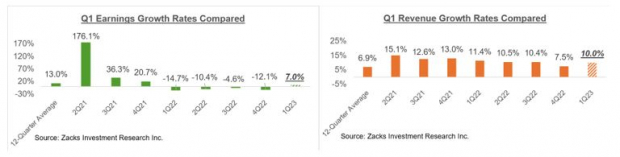

Including Friday morning’s bank results, we now have Q1 earnings from 30 S&P 500 members. Total earnings for these 30 index members are up +7% from the same period last year on +10% higher revenues, with 83.3% beating EPS estimates and 73.3% beating revenue estimates.

Banks and other financial operators dominate this week’s reporting docket, but we also have a slew of blue-chip operators from Johnson & Johnson and Proctor & Gamble to Netflix, Tesla, and many others.

The first set of charts compares the earnings and revenue growth rates for the 30 index members that have reported with what we had seen from the group in other recent quarters.

Image Source: Zacks Investment Research

The comparison charts below put the Q1 EPS and revenue beats percentages in a historical context.

Image Source: Zacks Investment Research

The Earnings Big Picture

To get a sense of what is currently expected, take a look at the chart below that shows current earnings and revenue growth expectations for the S&P 500 index for 2023 Q1 and the following three quarters.

Image Source: Zacks Investment Research

As you can see here, 2023 Q1 earnings are expected to be down -9.4% on +1.9% higher revenues. This would follow the -5.4% earnings decline in the preceding period (2022 Q4) on +5.9% higher revenues.

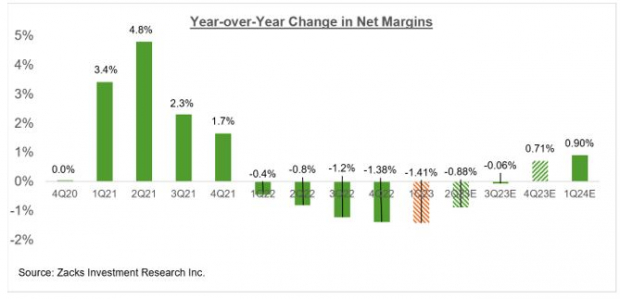

Embedded in these 2023 Q1 earnings and revenue growth projections is the expectation of continued margin pressures, which has been a recurring theme in recent quarters. The chart below shows the year-over-year change in net income margins for the S&P 500 index.

Image Source: Zacks Investment Research

Estimates for Q1 came down as the quarter got underway, in-line with the trend that had been in place since the start of 2022. That said, the magnitude of negative revisions to Q1 estimates was smaller relative to what we had seen in the preceding two periods.

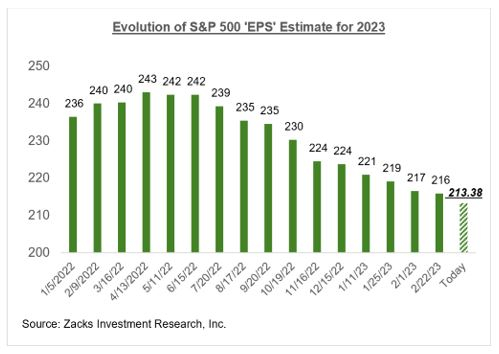

Estimates for full-year 2023 have also been coming down as well, as we have been pointing out consistently. The chart below shows how the aggregate 2023 S&P 500 earnings estimate has evolved.

Image Source: Zacks Investment Research

As we have been pointing out all along, 2023 earnings estimates peaked in April 2022 and have been coming down ever since. Since the mid-April peak, aggregate earnings have declined by -13.1% for the index as a whole and -14.8% for the index on an ex-Energy basis, with the declines far bigger in a number of major sectors.

You have likely read about the roughly -20% cuts to S&P 500 earnings estimates, on average, ahead of recessions. Many in the market interpret this to mean that estimates still have plenty to fall in the days ahead. But as the aforementioned magnitude of negative revisions in excess of -14% on an ex-Energy basis show, we have already traveled a fair distance in that direction.

Importantly, some key sectors in the path of the Fed’s tightening cycle, like Construction, Retail, Discretionary, and even Technology, have already gotten their 2023 estimates shaved off by a fifth since mid-April.

We are not saying that estimates don’t need to fall any further. If nothing else, estimates for the Finance sector will need to come down in the wake of the ongoing banking industry issues. But rather that the bulk of the cuts are likely behind us, particularly if the coming economic downturn is a lot less problematic than many seem to assume or fear.

Please note that the $1.893 trillion aggregate earnings estimate for the index in 2023 approximates to an index ‘EPS’ of $213.38, down from $221.05 in 2022. The chart below shows how this 2023 index ‘EPS’ estimate has evolved over time.

Image Source: Zacks Investment Research

The chart below shows the earnings and revenue growth picture on an annual basis.

Image Source: Zacks Investment Research

For a detailed look at the overall earnings picture, including expectations for the coming periods, please check out our weekly Earnings Trends report: 2023 Q1 Earnings Season Likely to Reflect Continued Margin Pressures.

More By This Author:

Are Earnings Estimates Too High?2023 Q1 Earnings Season Likely To Reflect Continued Margin Pressures

Bank Earnings Looming: What Can Investors Expect?

Comments

Log in or sign up to join the conversation.