Analysts Remain Positive Following Alibaba Group Holding Ltd. Quarterly Earnings

By Sarah Roden

On May 7, Alibaba (NYSE: BABA) announced earnings from the 2015 quarter ending in March. The Chinese e-commerce website beat estimates with significant growth and announced a new CEO. This is Alibaba’s third earnings report since going public over the summer with a record-breaking IPO.

Alibaba posted $2.81 billion in quarterly revenue, beating the estimate of $2.78 billion and marking a 45% year-over-year increase. Alibaba attributed the revenue increase to the growth in commission revenue and online marketing services revenue. Analysts also note that the Lunar New Year fell within the quarter, resulting in a seasonal impact on sales. Gross merchandise volume, or GMV, increased 40% year-over-year primarily driven by a 77% year-over-year increase in the number of active buyers on the platform. Alibaba saw an increase in mobile users with a 157% year-over-year increase in mobile GMV. Alibaba posted non-GAAP diluted earnings per share of $0.48, over the analyst estimate of $0.42.

Executives were pleased with the earnings report. Former CEO Jonathan Lu commented, “Our business continues to perform well, and our results highlight both the strength of our ecosystem and the strong foundation we have for sustainable future growth in China, and beyond.” CFO Maggie Wu echoed this sentiment, commenting, “We continue to execute our growth strategy and focus on long-term value creation. The fundamental strength of our business gives us the confidence to invest in new initiatives, add new users, improve customer experience and expand our products and services.”

Alibaba also announced that its COO, Daniel Zhang, will be replacing Jonathan Lu as CEO. Lu will help with the transition and will remain on the board of directors.

According to Smarter Analyst, analyst Victor Anthony of Axiom reiterated a Buy rating on Alibaba with a $110 price target on May 8. Anthony noted, “The quarter was solid with stable monetization rates, and overall improvements from here looking sustainable as mobile GMV becomes a majority of the mix.” Despite challenges from recent headlines surrounding tighter regulation and counterfeit goods, Anthony believes “Alibaba is likely to overcome these recent woes.” The analyst concluded, “The risk-reward to owning the shares at these levels is in investors’ favor with expected upside of 45% in our bull-case model versus downside of 14% in our bear-case model.”

Victor Anthony has a 65% overall success rate recommending stocks with a +16.9% average return per rating.

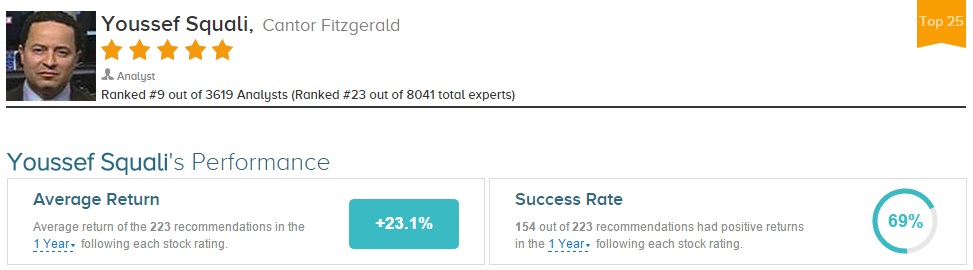

Separately on Smarter Analyst, Youssef Squali maintained a Buy rating on Alibaba and raised his price target from $100 to $110 following earnings on May 8. Squali noted the “solid” quarterly earnings report with revenue and EPS coming in ahead of expectations. The analyst remains bullish on the stock commenting, “We continue to like the stock given BABA’s dominant position in Chinese e-commerce, success so far in transitioning to mobile, opportunity both in and outside of China, and strong balance sheet.”

Youssef Squali has a 69% overall success rate recommending stocks with a +23.1% average return per rating.

Overall, the top analyst consensus for Alibaba on TipRanks is Strong Buy.

Disclosure:To see more visit more

Comments

No Thumbs up yet!

No Thumbs up yet!