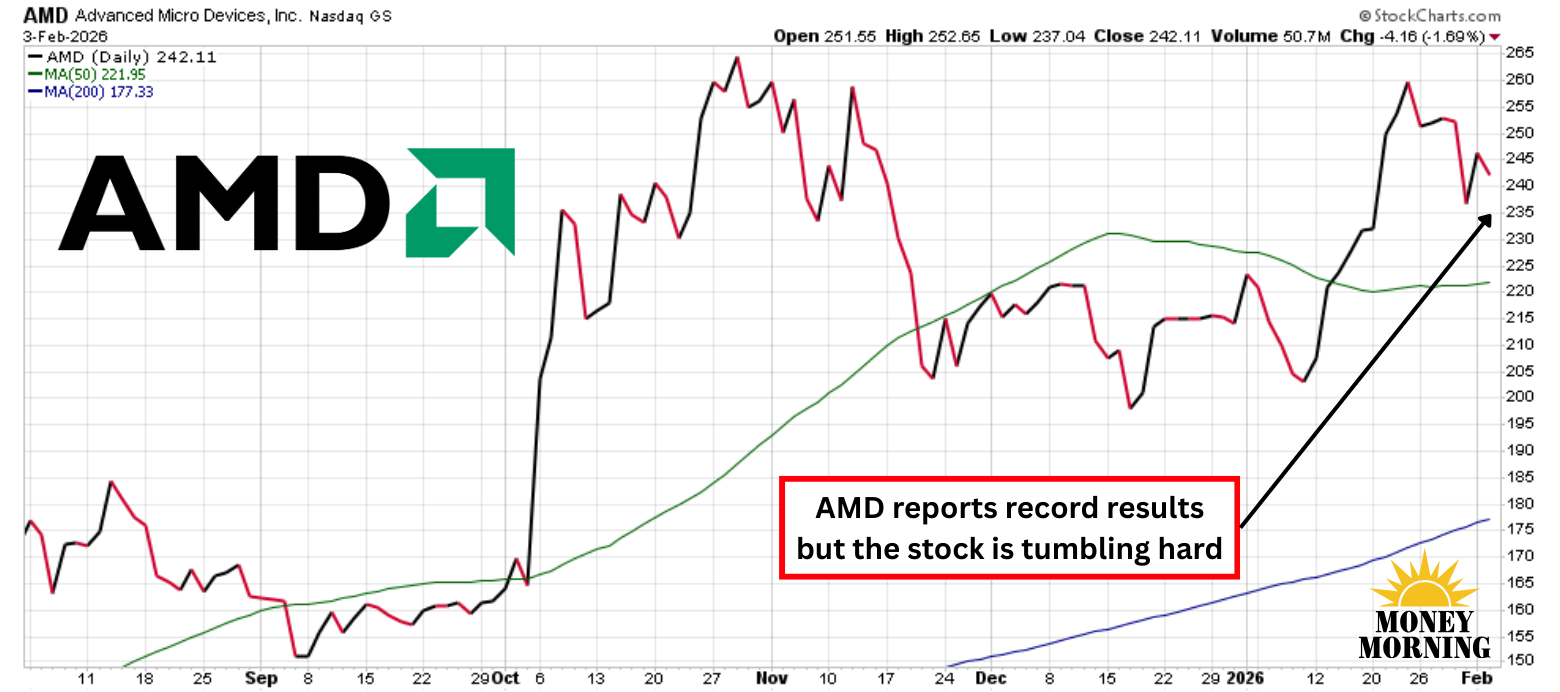

Market jitters over the sustainability of AI demand and a broader rotation out of high-flying tech stocks have eclipsed Advanced Micro Devices' (AMD) stellar fourth-quarter earnings. Despite posting record revenue of $10.3 billion – a 34% year-over-year surge that beat estimates of $9.7 billion – and earnings of $1.53 topping expectations of $1.32 per share , AMD shares plunged 10% in premarket trading today.

The sell-off reflects investor unease about potential AI hype cooling, U.S.-China trade tensions, and seasonal slowdowns. Yet, with robust growth in data centers and AI chips, this disconnect raises a compelling question: Is the dip a golden opportunity for investors to buy into AMD's long-term AI dominance?

Record-Breaking Performance in Key Segments

AMD's Q4 triumph was fueled by explosive demand in its Data Center and Client segments, amplified by AI momentum. Data Center revenue soared to a record $5.4 billion, up 39% year-over-year, powered by strong sales of EPYC processors and Instinct GPUs. This growth underscores accelerating CPU market share gains and widespread AI adoption across cloud and enterprise customers. An unexpected upside came from MI308 accelerators shipped to China, contributing $390 million despite export curbs, highlighting AMD's agility in navigating geopolitical hurdles.

Client processors also shone, generating $3.1 billion – a 34% increase – with record Ryzen revenue driven by a growing commercial mix. This reflects resilient PC demand for AI-enabled devices. Gaming added $843 million, up 50%, while Embedded edged up 3% to $950 million. Overall, full-year revenue hit $34.6 billion, up 34%, with free cash flow doubling to $5.5 billion.

(Click on image to enlarge)

Forward Guidance and Growth Prospects

Looking ahead, AMD guided Q1 2026 revenue to $9.8 billion, exceeding analyst forecasts of $9.4 billion, though down sequentially due to seasonality. Notably, the Data Center segment is expected to grow quarter-over-quarter, with China AI sales minimal at $100 million. Management remains bullish, targeting over 60% annual Data Center growth for the next three to five years, projecting tens of billions in AI revenue by 2027.

Gross margins hit 55%, boosted by a MI308 reserve release, but underlying improvements stem from a favorable mix of newer EPYC, Instinct, and Client products. In Client, PC strength continues despite a modestly declining total addressable market (TAM) in 2026. Gaming faces headwinds, with semi-custom revenue projected to drop double digits as the current console cycle matures – impacting partnerships like Microsoft's (MSFT) Xbox and Valve's Steam Machine.

Embedded is stabilizing and poised for growth, backed by record design wins for longer-term stability. A key second-half 2026 inflection point is the ramp-up of major, capital-intensive scaling and deployment phases of its next-generation AI infrastructure products, such as its Helios and MI450 AI racks, with its supply chains deemed adequate to meet AMD's plans.

The main risks it faces include escalating China export controls, the console downcycle, execution on those AI ramps, and gross margin pacing for its new GPUs. Still, the quarter was strong, driven by surging Data Center CPU/GPU demand and record PC performance.

Bottom Line

While skepticism lingers about AI's long-term viability amid economic shifts, AMD's results provide ample evidence of a durable growth path. As new chips and platforms like MI450 and Helios scale, expect continued robust quarters. This pullback offers investors a chance to snag the stock at a discounted valuation, positioning their portfolios for substantial upside in the AI era.

More By This Author:

Cathie Wood Just Dropped $33.5 Million On Robinhood. Time To Buy?PayPal Is Plunging 14% As Profits Come Up Short

Is Bitcoin About To Get Hit By A Polar Vortex?

Comments

Log in or sign up to join the conversation.