Image Source: Pixabay

The media have been giving considerable attention to the national debt in the last year or so. They have some cause, it has been rising rapidly, and more importantly, the interest burden of the debt has increased sharply since the Fed began raising rates last year. But, if we want to be serious, rather than just write scary headlines, we have to ask why the debt is a problem.

The first concern to dispel is the idea that the country somehow has to pay off its debt. Our national debt is in dollars, which the government prints. Unless something truly bizarre happens, we will always be able to print the dollars needed to pay interest and principal on government bonds.

We could have some story that if our economy collapses people could lose confidence in our debt. That is true, but a bit nuts. If our economy collapses, we should be worried about our economy collapsing, the debt is really beside the point.

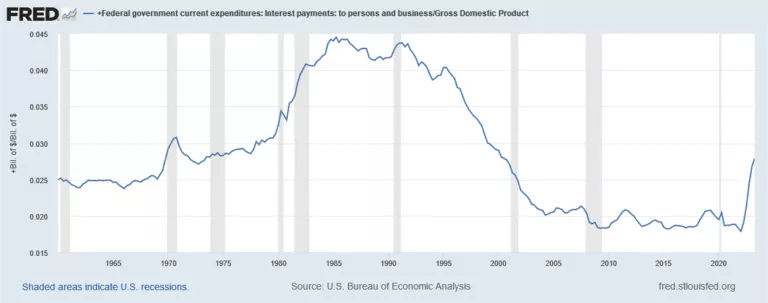

The more serious issue is that rising interest payments will be a burden. This is a real issue, but there are several important qualifications. First, in spite of the large debt, even relative to the size of the economy, interest payments relative to GDP are not especially high. Currently, interest payments relative to GDP were just hitting 2.8 percent last quarter. They are still below the 4.4 percent share reached in the early 1990s. And, for history fans, this burden did not prevent the 1990s from being a period of general prosperity.

(Click on image to enlarge)

Military Spending

The second point is that we do need to put this burden in a bit of perspective since it is often treated as a generational issue. Suppose the interest burden does rise to three or four percent of GDP, or even higher. Is that an unbearable burden?

Back in my younger days, we used to spend a much larger share of the budget on the military. In the 1950s and 1960s military spending was generally over 8.0 percent of GDP. At the peak of the Vietnam War, it exceeded 10.0 percent of GDP. It dropped in the 1970s, but the Cold War buildup under Reagan again pushed it above 6.0 percent of GDP.

Military spending is currently under 3.0 percent of GDP. Suppose a magician came down and eliminated the national debt so we no longer had to pay any interest, but forced us to increase spending on the military to 6.0 percent of GDP. Are we now better off? Can we tell our children that they should be happy?

What we should care about with military spending is that we are secure as a country. If that can be accomplished by spending less than 3.0 percent of GDP on the military, then we are much better off than in a world where we are spending 6.0 percent of GDP on the military.

The amount of spending it takes to make us secure, and what that means, are obviously debatable points, but the basic logic is not. From the standpoint of maintaining and improving our living standards, spending on the military is the same thing as throwing money down the toilet.

This is an important point that needs to be yelled loudly at the people anxious to have a New Cold War with China. They also need to recognize that the Soviet economy peaked at around 60 percent of the size of the U.S. economy. The Chinese economy is already more than 20 percent larger using a purchasing power parity measure of GDP. This means that Cold War-type competition with China is likely to be incredibly expensive, even assuming we never get into an actual hot war.

Global Warming: Will We Celebrate Containing the Debt if the Planet Burns?

The third point on this generational issue is that we need to look around at the country and the world. Global warming is having a large and devastating effect on the environment. We are seeing an unprecedented wave of extreme weather events, including droughts, dangerous heat waves, hurricanes, and flooding. This will only get worse through time.

It is great that Biden put the country on a path toward clean energy with the Inflation Reduction Act, but we will need to do much more. Thankfully, the rest of the world, and especially China, is far ahead of us. The idea that somehow the debt is an overriding generational issue, when we are facing the destruction of the planet, is something that can only be taken seriously by our policy elites. Our success in limiting global warming will have infinitely more relevance to the quality of the lives seen by our children and grandchildren than anything that happens with the national debt.

Why Spend Money When We Can Just Issue Patent Monopolies?

The fourth point is that direct spending is only one way the government pays for things. The government supports a huge amount of innovation and creative work by awarding patent and copyright monopolies. While these monopolies are one way to provide incentives, they also carry an enormous cost. In the case of prescription drugs alone, they likely cost the country more than $400 billion a year (more than $3,000 per family, each year) in higher drug prices. We will spend over $570 billion this year on drugs that would likely cost us less than $100 billion if they were sold in a free market without patent monopolies or related protections.

If we look at the impact of these government-granted monopolies in other industries, like medical equipment, computers, software, video games, and movies, they almost certainly add more than $1 trillion a year to what households pay for goods and services. For some reason, the people screaming about the debt literally never say a word about the costs the government imposes on us by issuing patent and copyright monopolies.

And, these costs are interchangeable. For example, we can spend more money on government-funded research in developing prescription drugs and require that drugs developed as a result are available as generics sold in a free market. In the standard deficit accounting, we would only pick up the extra cost from the government-funded research. We would not see the savings from cheaper drugs, except insofar as the government paid less for buying drugs.

We could also go the other way. We could give out patent or copyright monopolies as a way to fund various government services. For example, we could give the Social Security trust fund a patent monopoly on ice that lasts for 1000 years. It could finance benefits by charging licensing fees for using ice. That would save the government around $1 trillion a year in Social Security spending. That should make the deficit hawks very happy.

Yeah, that would be absurdly inefficient and be a license for all sorts of corruption. But so is our current patent system, which does things like encourage drug companies to push opioids and lie about the effectiveness of their drugs. But, we know the deficit hawks, and many in the media who push their handouts, don’t care about efficiency, they just want lower debt. So, the patent monopoly on ice should be good for them.

Debt and Stock Prices

Okay, but I promised to say how a higher debt can be bad news like higher stock prices. This requires a little bit of Econ 101. The serious story of how higher debt is bad is that it can lead to higher interest payments.

The “can” here is important. The debt-to-GDP ratio rose considerably in the Great Recession and the years immediately following, but the ratio of interest payments to GDP fell. This was because we had very low-interest rates in these years. The Fed deliberately kept rates near zero because it was combatting weak growth and high unemployment, as we faced a period of secular stagnation.

We don’t know yet whether the economy will return to something like secular stagnation as the impact of the pandemic fades into the distance. Some of the factors that led to this stagnation, most notably slower population and labor force growth, and an upward skewed distribution of income, are still present. However, we have seen some reversal of the upward redistribution of income, as wage growth has been strongest for those at the bottom of the wage ladder. But, we don’t know how far this trend will go. We also don’t know if the full increase in profit shares will be reversed.

The impact of new technologies, most notably AI, is still very much unclear. If they do have a substantial impact on productivity growth, then we may again see rising unemployment and a need for the Fed to push rates lower. Also, as we switch to clean technologies, there will be less demand for fossil fuels and many of the associated services. Of course, these technologies may also be associated with an investment boom that will increase demand for labor.

There are reasonable arguments on both sides of the secular stagnation issue, but let’s assume that the Fed does not return to its zero-interest policy, but rather we get an interest rate structure that looks something like what we saw just before the pandemic. In that context, we will see higher interest payments as a share of GDP.

It is worth thinking for a moment why this would be bad. As the Modern Monetary Theory people remind us, the problem of a government deficit is not the financing – we can always print the money – the problem is that it can be inflationary since it can lead to too much demand in the economy.

Interest payments on the debt don’t directly create demand in the economy. They create demand only when people spend the interest payments. Insofar as the payments are made to high-income people with low propensities to consume, they will have a relatively limited impact on spending and demand. But not all interest payments go to rich people, and even rich people will spend some fraction of their interest.

So, the problem of higher interest payments on the debt is increased consumption demand, which can create inflationary pressures in the economy. This gets us to the problem of a rising stock market.

While some people think of the stock market as a way to raise money for investment, most firms rarely raise money through this channel. In fact, companies typically go public as a way for the initial investors to cash out their gains. The main economic impact of a rising stock market is not on investment but rather on consumption.

There is a well-known, stock wealth effect that is usually estimated at between 3 to 4 percent. This means that an additional dollar of stock wealth leads to an increase in annual consumption of 3 to 4 cents. Households currently hold around $30 trillion in stock wealth. If the stock market rises by 20 percent, that would create another $6 trillion in stock wealth.

Assuming that people spend 3-4 percent of this new wealth, we would see an increase in annual consumption of between $180 billion and $240 billion. If we are concerned about excess demand creating inflationary pressures in the economy, then we should be worried about the impact of this rise in stock wealth.

In that sense, a rising stock market is bad news for the economy in the same way as increased interest payments on government debt. If we assume that 70 percent of interest payments are spent, then a 20 percent rise in the stock market will create roughly the same inflationary pressure as $300 billion in additional interest payments.

So, if we are worried that interest on the debt will lead to inflation, we should also be reporting the bad news on inflation every time we see a big run-up in stock prices. In short, interest on the debt can be a problem, but it gets far more attention than items that are much bigger problems in any realistic assessment of the situation.

More By This Author:

Crypto And Finance Are Waste And A Drag On The EconomyMixed Jobs Report In August: Where Does The Economy Stand Now?

2.0 Percent Is An Average, Not A Ceiling: Should We Be Scared By Jerome Powell’s Speech?

Comments

Log in or sign up to join the conversation.