7 Stocks To Buy In The Market’s 3 Hottest Sectors

Invest in the momentum of these seven stocks spanning three different sectors that all have strong economic tailwinds lifting their revenues, profits, and stock prices higher. As the market continues to flirt with and reach new all-time highs, many sectors in the market seem primed to far outpace their peers.

Sometimes being a good investor is like being a good offensive coordinator in the NFL. You just have to take what the defense is giving you that game. Sometimes that means deploying a power running game, other times dinking and dunking the ball to move the chains. Occasionally it means airing the ball out frequently downfield. Just like different phases of the market, each game calls for a different strategy.

So what is working in the current equity market? Here are a couple areas of strength I have noticed and profited from lately, and I plan to continue to do so until the defense changes up again.

The consumer market in China is evidently doing better than some thought a few months ago. I have three large cap holdings with significant exposure to the consumers in the Middle Kingdom. I had been averaging down on their declines in late 2015 and early 2016. All three companies have solid long-term business fundamentals, rock-solid balance sheets and also pay a nice dividend yield which makes it easier to wait for the inevitable turnaround. All of these stocks are in the beginning of a rally.

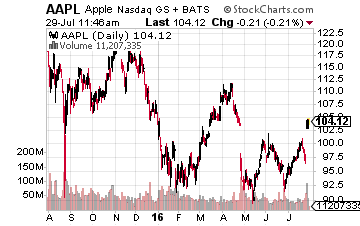

Let’s start with Apple (Nasdaq: AAPL), which saw revenue decline significantly this quarter when compared to last year, however, results came in much better than expected. The shares are up some 10% since quarterly results were released, but they are still cheap. The shares sell for approximately nine times earnings if you back out the company’s massive cash holdings and yield more than two percent as well.

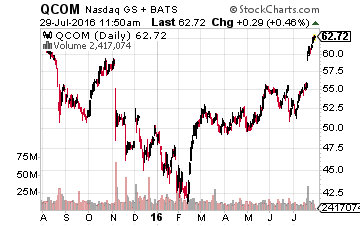

Qualcomm (Nasdaq: QCOM), which was waylaid by Chinese regulators in 2015 is having a much better 2016 and is one of the strongest performers in large cap tech this year. The company recently beat both top and bottom line expectations with their quarterly numbers and raised guidance as well. This is another tech giant with substantial net cash on balance sheet. The shares yield just under three and half percent and sell at a discount to the overall market multiple.

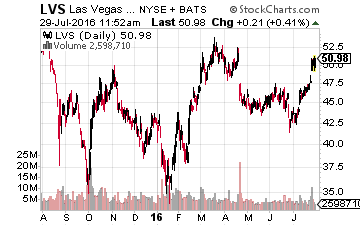

Finally, we have Las Vegas Sands (NYSE: LVS), which has been dealing with a slowdown in traffic to the gambling hub of Macau thanks to the Chinese leadership crackdown on corruption for 18 months. The stock has been moving up lately and the company just recently stated it saw the mass market gaming sector in Macau – where it is the biggest player – “stabilizing”. The shares yield nearly six percent even after its recent rally. Capital expenditure needs should also drop markedly in 2017 and 2018 as its 3,000 room Parisian Macao comes fully online as well.

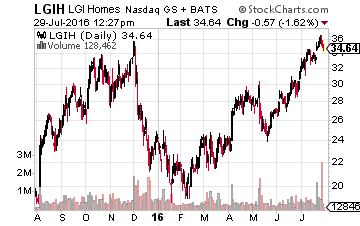

Next, homebuilders continue to be on a roll. They should be as well, given June new home sales just posted their strongest monthly levels in eight years. Mortgage rates remain at historical lows boosting affordability. Housing starts are rising but still remain significantly under their long-run averages which they have done consistently over the past decade. This means there is a lot of long-term pent up demand for years to come barring a major recession.

I have spoken often of two small builders, LGI Homes (Nasdaq: LGIH) and Taylor Morrison (Nasdaq: TMHC), on these pages. Both have had nice rallies in recent months but I am still holding them as they remain cheap compared with their growth prospects. Large builders like Toll Brothers (NYSE: TOL) continue to see revenue growth in the mid-teens and are cheap on a long-term basis based on their sales trajectory. They are a little more expensive than the smaller builders but make up for with greater financial flexibility and wider geographical diversity in their housing communities.

Finally, small biotech is on a recent roll. Relypsa (Nasdaq: RLYP), which I have profiled on these pages at least a half dozen times over the past year, was bought out with a 60% premium by Galencia on July 21st. Here are two other small biotechs that look very undervalued here.

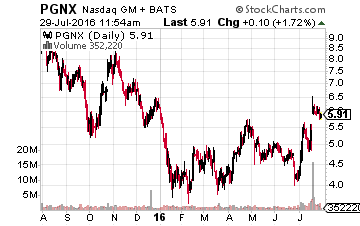

Progenics Pharmaceuticals (Nasdaq: PGNX) received FDA approval for the oral version of relistor on July 19th. The injectable version has been available for several years. This triggered a $50 million milestone payment to Progenics from its marketing and distribution partner. It also should triple or quadruple royalty revenues from the relistor franchise over time, not to mention accelerate the timeline Progenics can earn an additional $200 million in sales milestones. The stock is undervalued just based on the company’s relistor franchise. However, the company also has two other compounds in late stage development that should provide key Phase III readouts over the next couple of quarters.

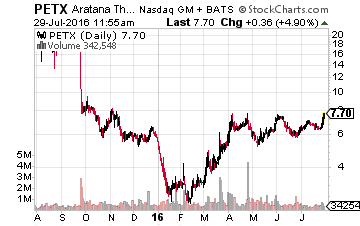

Aratana Therapeutics (Nasdaq: PETX), a unique veterinary drug play has been on the move over the past week but still trades for way under its true market value. Its first commercialized product “Galliprant” was approved earlier this year which was followed by the approval of Entyce soon thereafter. The company should have a third and possibly a fourth drug approved from its expanding pipeline by the end of 2016. This underfollowed “off the radar” biotech play is woefully undervalued with just a $250 million market capitalization.

Those are some quick thoughts on what I see working in the current market, and should continue to work until Mr. Market deploys a different defensive scheme.

Disclosure: Positions: Long ...

more