6 Stocks To Profit From The Upcoming Election

The election season is now “officially” kicking off as both parties conduct their nominating conventions. These affairs promise to have more theater than usual given how divided the country is amid the weakest post-war recovery on record, increasing acts of terrorism in the Western world, rising economic inequality, and escalating racial tensions. Given the nature of the two major candidates and their highly unfavorable ratings, it is likely to go down as one of the nastiest presidential elections in memory.

I am making no predictions on this election other than the nation will remain as polarized and divided as it has been in decades, regardless of the winner. If there is one thing 2016 has shown us, it is that trying to predict some event months away is a fool’s game. One just has to look at the recent results of the U.K. referendum that blindsided pundits as well as investors and will lead to the so-called “Brexit,” which is already pushing down European economic growth forecasts.

So which areas of the market might benefit once the election is over? Two sectors of the economy and market come to mind. First, is construction, homebuilding, and infrastructure stocks. Both parties agree that the nation’s infrastructure is crumbling and needs repair. This is one of the few areas of agreement between the two groups.

Mr. Trump has also been defined by building grand projects and one of the first things I think he will target is getting a massive infrastructure package passed as part of his job creation package. Mrs. Clinton will also want this as part of her job creation efforts and also as a payback to the various unions that would benefit from increased infrastructure spending for their support during the election. Both candidates will want the improving housing market to continue, as that is a big source of jobs as well.

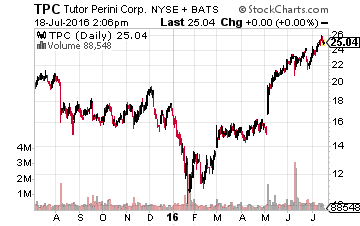

Obviously, this will help home builders as well. One beneficiary will be Tutor Perini (NYSE: TPC), which already is benefiting from increasing spending by local and state governments. The construction giant already has an impressive $8 billion order backlog as it is very involved in mass transit projects as well as big development efforts like the Brooklyn Yards. This is a huge departure from the residential condo skyscrapers that powered its growth prior to the financial crisis. The stock has bounced back very nicely from a poor performance in 2015 and should more than double earnings in FY2016 after a significant drop off in 2015 thanks to some high profile cost overruns.

Despite the recent rally in the shares the stocks trades for roughly 12 times this year’s projected earnings. Canaccord Genuity lifted its price target from $18.00 to $30.00 a share on Tutor last week.

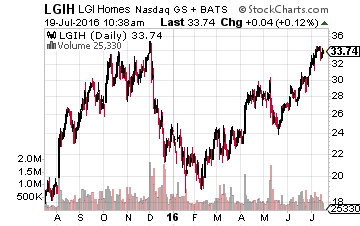

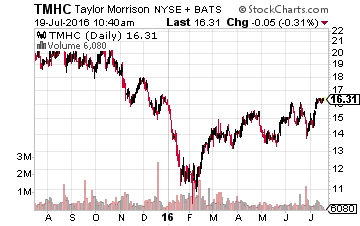

I continue to like homebuilders LGI Homes (Nasdaq: LGIH) and Taylor Morrison (Nasdaq: TMHC) and both have been profiled often on these pages. LGI Homes recently reported home closings were up 30% in the first half of 2016 compared to the same period a year ago. Taylor Morrison has been on a roll since insiders made some significant purchases near the end of the first quarter. UCP Inc. (NYSE: UCP), a California home builder, has also seen some insider buying recently and is undervalued on a book value basis. The company acquired most of its land lot inventory from 2008 to 2010 when lots were much, much cheaper than they are today.

Two more obvious winners in the upcoming election are the biotech and pharmaceutical sectors. Both have been battered by election-driven rhetoric about drug price “gouging” and the need to impose some sort of price controls on medicines. This area of the market is in its longest and deepest bear market since 2008. However, the populist rants about drug prices have already markedly decreased since the campaign of Bernie Sanders ended.

More importantly, the most likely outcome is the House will continue to be controlled by the Republicans. This makes any new major drug pricing legislation a non-starter. Now is the time to take advantage of this eventuality, especially given the downright cheap valuations in many of the large cap names in these sectors.

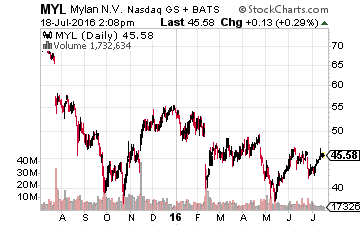

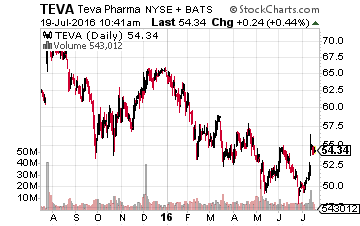

Mylan (NYSE: MYL), a generic drug powerhouse, looks enticing here. The stock has seen some insider buying recently, is still seeing solid revenue and earnings growth, and goes for just over nine times this year’s earnings. The stock is also selling for less than 60% of what drug giant Teva Pharmaceuticals (Nasdaq: TEVA) offered to buy it for early in 2015.

Speaking of Teva, that is another solid value stock.

Last week the company announced that once its $40 billion purchase of the generic drug business from Allergan (NYSE: AGN) closes later this year, it saw 14% annual EBITDA growth through FY2019. That is good growth for a business that is currently priced at just over 10 times forward earnings and offers a dividend yield north of two percent.

I do not know how the election will turn out – frankly, I would just like it to be over already – however, the above concerns should do well regardless of the outcome.

Disclosure: Positions: Long ...

more

Thanks for sharing