5 Tailwinds For Children's Place

Specialty retailer Children’s Place (PLCE) has a lot going for it right now. Here are five major tailwinds in place for the company:

- Parents skimped on kids’ clothing last year as most students did not physically go ‘back to school’ due to COVID-19. This year those children are a year older, a lot larger, and their clothes are in need of major upgrades.

- President Biden’s aid to families with children began distributing substantial electronic payments this month. That program is scheduled to go on for quite a while, with the ultimate political goal to make the payments permanent.

- Children’s Place has vastly improved its online presence and fully integrated its purchase of industry rival Gymboree.

- Many unprofitable stores were closed during the COVID-19 shutdowns. Charges for those closures were already accounted for, but the improved margins on the remaining units are just starting to fully kick in.

- It is likely that management will reinstitute cash dividends before long, providing a larger universe of potential institutional holders.

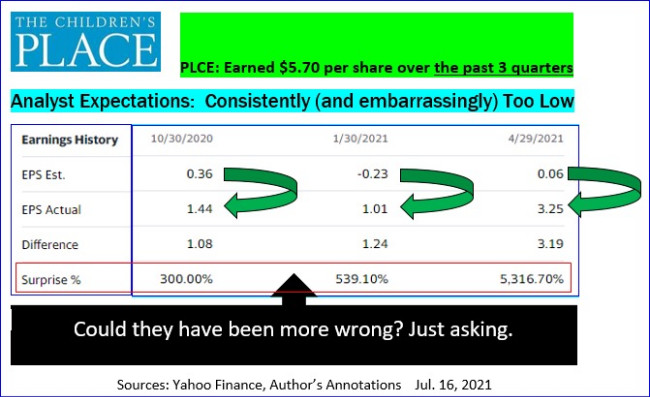

The CEO of Macy’s (M) was recently on CNBC, saying that he expects this fall to be the best ‘back to school’ season in that venerable company’s history. Analysts have been way too slow in realizing just how favorable conditions for Children's Place have become. Their estimates over the past three quarters were pathetically off by percentages that seem to be typos but weren’t.

Over those nine months of reported results, PLCE posted $5.70 in EPS. The end of July quarter last summer marked the very bottom of PLCE’s COVID-19 woes. They lost $1.48 in adjusted earnings during that interval last year (per Yahoo Finance). Even a modest profit this year will make trailing 12-months EPS at least around $7.50.

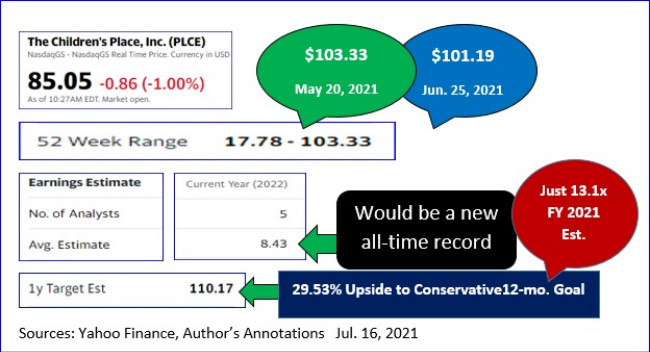

Yahoo Finance now projects $8.43 for PLCE’s full fiscal year, ending Jan. 29, 2022. Based on their past forecasting history, that number might very well turn out to be too low.

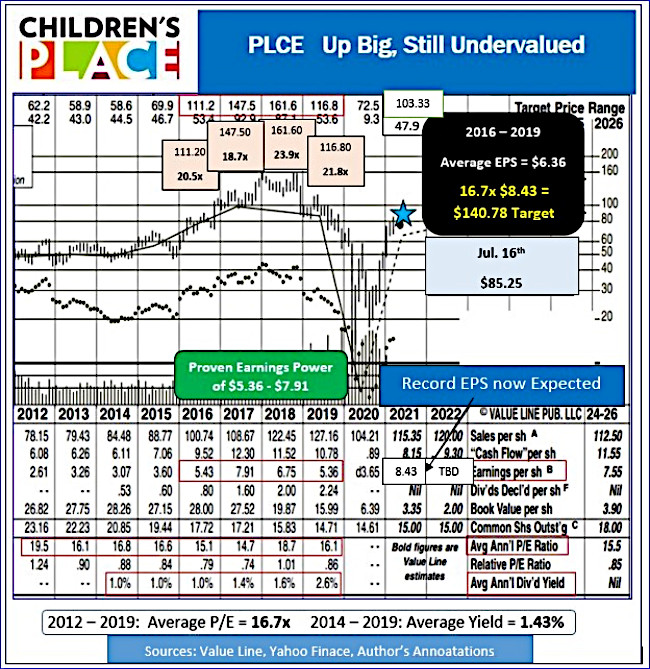

What is Children's Place really worth? In the previous eight pre-COVID-19 years, a typical multiple ran about 16.7x. Applying that P/E to this year’s estimate supports a greater than $140, seven-month price target.

That goal is not far-fetched. Children's Place peaked between $111.20 and $161.60 during each of the four years stretching from 2016 through 2019. The shares hit $103.33 in May of this year. They still commanded over $101 as recently as June 25, 2021, just a few weeks ago.

With all-time record results on tap, there’s every reason to think Children's Place can eventually exceed all those old highs. Buyers of PLCE’s Jan. 2023, LEAP calls at $130 and $140 were paying $12.50 and $10.30, respectively, on July 16, even with the stock down for the day and near $85. They won’t even start to make money on expiration day until PLCE passes $142.50 or $150.30.

Buying shares outright is a simple, plain way to bet on Children's Place's fine prospects. Selling puts, or setting up buy/write combinations could work out brilliantly, too.

Disclosure: I am long PLCE shares, short PLCE naked put and covered call options.

Disclaimer: © 2021 MoneyShow.com, LLC. All Rights Reserved.