Image: Bigstock

The outlook for the Internet Software & Services industry appears strong. Estimates have increased substantially over the past year, as pandemic-related aberrations have normalized and companies have executed strongly on their strategies. With a number of players adopting a subscription model, the predictability and stability of performance continues to improve.

The chances of a recession are slim at the moment, although macroeconomic concerns persist and political instability in the world remains an overhang. Also, being the backbone of the digital economy, it’s hard to see this industry doing badly over the long-term. The diversity of players in this group may lead to some dissonance.

The industry usually trades at a premium to the S&P 500 because of its innovation-driven growth, but prices have been coming down in recent months, leading to attractive valuations. Our picks are Criteo (CRTO - Free Report), Donnelley (DFIN - Free Report), and Okta (OKTA - Free Report).

About the Industry

The Internet Software & Services industry is a relatively small industry, primarily involved in enabling platforms, networks, solutions, and services for online businesses and facilitating customer interaction and use of Internet-based services.

Top Themes Driving the Industry

The level of technology adoption by businesses impacts growth. While some companies have already built their platforms, facilitating the development and use of artificial intelligence, others are scrambling to catch up in order to stay competitive. This is further accelerating the adoption of technology that can help collect and analyze data, whether on premise or in the cloud.

Additionally, today we have many more cloud-first companies than ever before. Therefore, there is steadily increasing demand for software and services delivered through the Internet.

There is increasing evidence that the Fed’s inflation fighting measures will not land us into a recession. Instead, the possibility of a cutback in the interest rate (this being an election year) is increasing.

However, the geopolitical tensions in Europe have a bearing on oil prices and supply chains, and therefore, contribute to a certain amount of volatility within the economy. Since the industry thrives on a strong economy that continues to do increasing levels of business, the macroeconomic outlook for 2024 is still a bit cloudy.

Given the colorful international politics and the resultant volatility in international markets, there is notable impact on company performance. The fact that they also serve a very broad spectrum of markets also makes it difficult to predict specific outcomes for the group, as a whole.

Therefore, industry players may increasingly prefer a subscription-based model, which brings relative stability to their businesses, especially when the companies have critical offerings. The ability to retain subscribers and raise prices as necessary is proving to be the key to success in the current environment.

The higher volume of business being operated through the cloud and the increasing demand for enabling software and services involves infrastructure buildout, which increases costs for players. This causes great fluctuations in profitability as new infrastructure is depreciated and fresh debt is serviced. So even for those players that see revenue growth accelerate, profitability can often be a challenge.

The Zacks Industry Rank Indicates Strong Prospects

The Zacks Internet – Software & Services industry is housed within the broader Zacks Computer and Technology sector. It carries a Zacks Industry Rank #22, which places it in the top 9% of more than 250 Zacks classified industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates that the industry is coping better than many others. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The industry’s positioning in the top 50% of Zacks-ranked industries is because the earnings outlook for the constituent companies in aggregate is improving. The aggregate estimate revisions indicate solid improvement, with estimates for both 2024 and 2025 trending up over the past year. The group’s aggregate earnings for 2024 are now up 44.8% from April 2023, while the 2025 estimate is up 30%.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

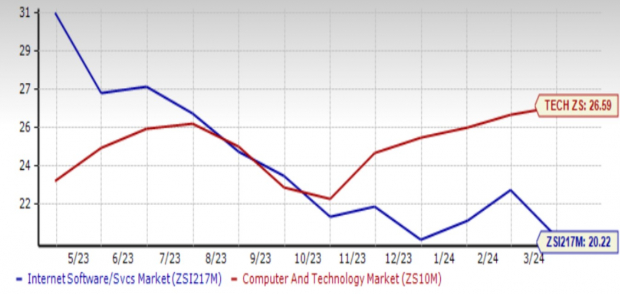

The Industry's Market Performance is Relatively Weak

The Zacks Internet Software & Services Industry has lagged both the broader Zacks Computer and Technology Sector and the S&P 500, particularly since last November.

The aggregate share price of the industry increased just 12% over the past year compared to the broader sector’s increase of 44.8% and the S&P 500’s increase of 25.4%.

One-Year Price Performance

Image Source: Zacks Investment Research

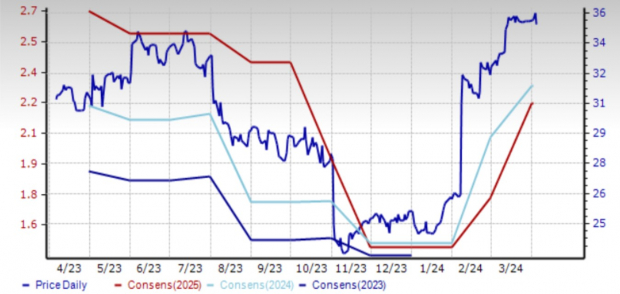

The Industry's Current Valuation: Attractive

While many of the individual players are still marking losses, the industry as a whole continues to generate profits. Therefore, on the basis of forward 12-month price-to-earnings (P/E) ratio, we see that the industry is currently trading at a 20.2X multiple, which is a 4.8% discount to the S&P 500 and a 24% discount to the technology sector.

At recent levels, it is also trading at a 12% discount to its median level of 22.9X over the past year. Therefore, whichever way you look at it, the industry is undervalued. The industry has traded in the annual range of 31X to 20.2X, as the chart below shows.

Forward 12 Month Price-to-Earnings (P/E) Ratio

Image Source: Zacks Investment Research

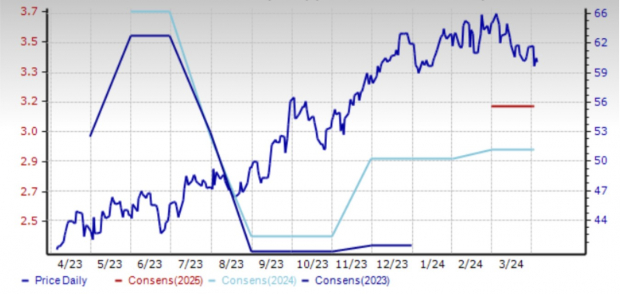

3 Stocks Worth Considering - Criteo S.A. (CRTO - Free Report)

Paris-based Criteo S.A. provides marketing and monetization services in North and South America, Europe, the Middle East, Africa, and the Asia-Pacific. Its unified, AI-driven platform directly connects advertisers with retailers and publishers to drive commerce on retailer sites and on the open Internet.

The company’s strategy is to harness AI to expand its reach across audiences, as cookies are gradually frowned upon and outlawed across the world. It therefore seeks to expand its ecosystem across advertisers, retailers and third-party platforms, using the commerce dataset to feed its AI models.

In 2023, it ratcheted up tech delivery and differentiation with the launch of the demand side platform called Commerce Max and the supply side platform called Commerce Grid. In the last quarter, the company continued to advance, with client retention at close to 90%, around 40% of live clients using more than one Criteo service (versus 35% last year), and accounting for a third of media spend activated through agencies.

In 2024, it will make use of the latest AI technologies, including generative AI to improve performance, enhance user experience, and optimize its service delivery process to further drive its strategy.

Shares of this Zacks Rank #1 (Strong Buy) company have gained 12.5% over the past year. The Zacks Consensus Estimate for 2024 has increased 15 cents (4.4%) in the last 30 days. The 2025 earnings estimate has also increased 15 cents (4.5%). Analysts are looking for revenue growth of 4.3% in 2024 and 2.5% in 2025, with earnings growth coming in stronger at 11.3% this year and roughly flat the following year.

Price and Consensus: CRTO

Image Source: Zacks Investment Research

Donnelley Financial Solutions, Inc. (DFIN - Free Report)

This company offers software and technology-enabled financial regulatory and compliance solutions, primarily in the U.S., Asia, Europe, and Canada. It operates through four segments: Capital Markets Software Solutions, Capital Markets Compliance and Communications Management; Investment Companies Software Solutions, and Investment Companies Compliance and Communications Management.

Donnelley continues to execute on its long-term strategy of growing its software and tech enabled services business while de-emphasizing its print business, leading to a doubling of revenues in the focus segment. Management expects this business to double again between 2022 and 2026, representing 55%-60% of total revenue by then.

Despite the continued weakness in the capital markets environment, the continued execution of Donnelley's long-term strategy worked in the company’s favor in 2023. It also made good progress on expanding the adoption of a recurring model of its regulatory and compliance offerings, which continues to improve the stability of its business. It also continues to deleverage the balance sheet (long-term debt is down 79.4% in the last six years, down 26% in 2023).

Shares of this Zacks Rank #2 (Buy) company have appreciated 48.5% over the past year, with estimates for 2024 and 2025 remaining stable in the last 30 days. Analysts currently expect the company to generate revenue and earnings growth of a respective 5.8% and 11% in 2024 and a respective 4.2% and 6.1% in 2025.

Price and Consensus: DFIN

Image Source: Zacks Investment Research

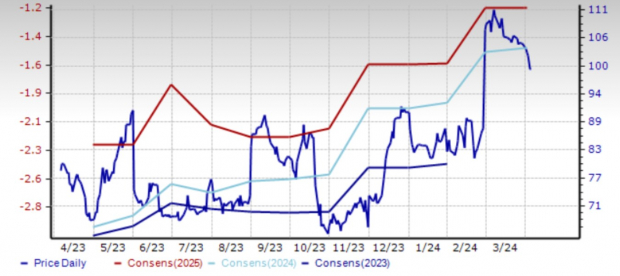

Okta, Inc. (OKTA - Free Report)

Finally, Okta provides a wide range of identity, access, and authentication solutions for small and medium-sized businesses, universities, non-profits, and government agencies within the U.S. and abroad. Its products are sold through a direct sales force and channel partners. It is headquartered in San Francisco, CA.

There was continued momentum in Okta’s business in the last quarter. The recurring revenue model is shaping up well. There were a record number of million dollar plus ARR contracts in the last year, with the number of such contracts growing 30% in the last fiscal year.

The company’s innovative product portfolio of Privileged Access, Identity Governance, and Access Management solutions (both workforce and customer) that are provided as a single platform positions it for continued expansion. The scope for growth remains substantial, with its backlog and revenue outlook continuing to grow double-digits. While macro concerns limit up-sell opportunities, management expects the dollar based retention rate to remain in the 111% range.

Shares of this Zacks Rank #3 (Hold) company are up 26.5% over the past year. Its 2025 (ending January) and 2026 estimates jumped substantially from the levels seen 60 days ago, but they have remained stable in the last 30 days. Analysts expect revenue and earnings for the current fiscal year to increase a respective 9.7% and 42.5%, followed by 12.1% revenue growth and 15% earnings growth the following year.

Price and Consensus: OKTA

Image Source: Zacks Investment Research

More By This Author:

Time To Buy Stock In These Highly Ranked Multi-Sector ConglomeratesWarner Bros. Discovery Stock Sinks As Market Gains: Here's Why

Should You Buy S&P 500 ETFs Now & Hold?

Comments

Log in or sign up to join the conversation.